Axsome (AXSM): $250 Is the Problem

Auvelity is a real franchise. The ADA launch is real optionality. Neither justifies $250.

The Multiple Is Doing the Work the Business Hasn’t Done Yet

AXSM trades at ~$250/share — roughly $13B market cap, ~$11.9B enterprise value. Against ~$700-750M in NTM revenue, that implies ~15-17x forward sales. The natural comp is Neurocrine Biosciences (NBIX), which built one of the most durable branded CNS franchises of the past decade with Ingrezza — and spent most of its commercial expansion phase trading at 9-12x forward revenue, with a profitable, moat-protected franchise already generating $1B+.

But hold on — ADA isn’t HD chorea. HD chorea was incremental, a contained bolt-on into a specialist channel Neurocrine already owned. ADA could be bigger than MDD. Genuinely. A large underserved population, a prescriber universe MDD never touched, a non-antipsychotic profile that removes the primary safety objection in elderly patients, and a category where the current market leader carries a black box warning. In the bull case, ADA doesn’t add to the Auvelity story — it doubles the TAM.

What it doesn’t resolve is the timing. The 15-17x is being paid today, against a revenue base that hasn’t seen a single ADA prescription. The inflection is priced. The evidence isn’t in yet.

The DCF range that anchors this note is $150-170/share. The gap to $250 is not a rounding error — it’s ~$4-5B of enterprise value that requires a specific, optimistic, and simultaneously true set of assumptions: Auvelity MDD continues compounding past its current penetration ceiling, ADA agitation ramps materially faster than the only available analog (Rexulti) suggests, and the pipeline generates a late-stage catalyst within 24 months. All three. That’s not impossible. That is the question.

~$700-750M

EV / NTM Revenue

~15-17x

NBIX - historical growth-phase multiple 1

9-12x

DCF fundamental range

$150-170 / share

Current price

~$250 / share

Implied premium to DCF

~47-67%

1 NBIX multiple reflects Ingrezza commercial expansion phase at ~$500M-$1B+ NTM revenue, pre-

profitability inflection. One of the strongest CNS commercial launches of the past decade - still traded

at 9-12x through most of its build.

Clinaptis analysis. Market data as of June 2026. DCF range based on bear/base scenario

peak sales assumptions; 10% discount rate applied.

CLINAPTIS")

Auvelity: Still Growing, But the Easy Specialist Phase Is Over

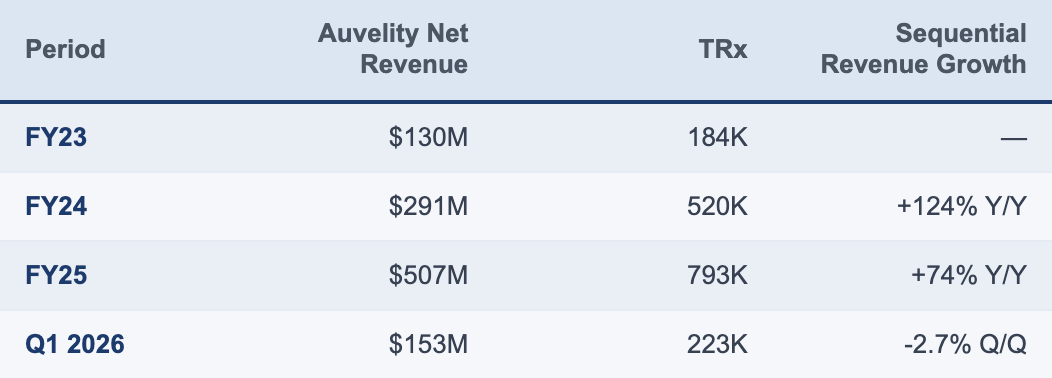

The launch trajectory is unambiguous: $15.7M in Q1 2023 to $507M in FY25, 92-94% gross margins throughout, ~78% commercial (86% total) coverage with near-universal Medicare/Medicaid. No GTN deterioration, no payer mix problem hiding in the financials. By any historical CNS benchmark, this is a strong commercial execution.

Q1 2026 operating loss increase reflects a ~$15.7M sequential SG&A step-up from completing the 630-rep ADA sales force build. Gross margin stable — operating leverage is a spend choice, not a pricing problem.

The ceiling question isn’t about what Auvelity has done. It’s about where the next increment of growth comes from — and the answer is structurally harder than the launch phase suggests. Early adoption was concentrated: 84% prior antidepressant exposure, 46% prior antipsychotic use, ~10% treatment-naïve at initiation. A high-conviction specialist population writing augmentation scripts. That cohort is largely captured. Cumulative writers now exceed 60,000, suggesting Auvelity has already penetrated a substantial portion of the highest-value psychiatry prescriber base. Q1 2026 added 5,500 new prescribers, but at ~13 scripts per writer annually, the average is being held down by newer PCP writers who write lower volumes per patient than the specialists who built the base.

The bull case for MDD from here rests on two things proving out simultaneously: PCPs maturing into higher-volume writers as familiarity with the drug builds, and the 56% first-line/first-switch shift translating into more scripts per patient over time rather than just earlier initiation. Both are plausible. Neither is proven. What’s certain is that the franchise is entering a new chapter where marginal returns per incremental prescriber are structurally lower — specialist writers were high-conviction, high-volume, treatment-refractory focused; PCP writers are earlier-line, lower-volume, and slower to deepen. Management’s own commentary confirms the transition. That’s not a criticism. It’s a description of where the lifecycle is.

What consensus hasn't adjusted for is that the same TRx count in a PCP-heavy mix carries less commercial value per writer than in a specialist-heavy one. Models extrapolating specialist-era trajectory assumptions into a PCP-era expansion are solving for the wrong base rate. The category isn’t broken. The marginal economics are just different — and at 15-17x forward revenue, different matters.

The ADA Question: Second-Mover in a Hybrid Market

ADA launch June 2026. Agitation hits ~45% of AD patients, carries 2-3x institutionalization risk. The current market leader is an antipsychotic with a black box warning. Auvelity’s profile — no black box, no mortality signal — removes the primary objection in elderly patients. The unmet need is real and the differentiation is clinical, not marketing.

The commercial build is the largest in AXSM’s history: 630 reps, ~68K HCP targets spanning neurology, geriatric psychiatry, memory clinics, and LTC. The underappreciated detail: ~34K of those 68K targets already sit inside the existing MDD call plan. Half the ADA target universe is a warm call, not a cold one. This isn’t a greenfield launch — it’s a second indication dropped into infrastructure already at scale. Execution risk is real; a build-from-scratch framing overstates it.

One underappreciated economic tailwind: management confirmed on the Q4 2025 call that 70%+ of ADA scripts are expected to flow through Medicare Part D — a channel that carries structurally lower GTN drag than the commercial insurance mix dominating MDD today, where copay cards and rebates are heavier. If ADA net revenue per prescription runs 10-20% (as a sensitivity, not mgmt. guidance) above MDD at the same WAC, the patient volume required to reach $4B ADA peak will be lower than models assuming parity currently imply.

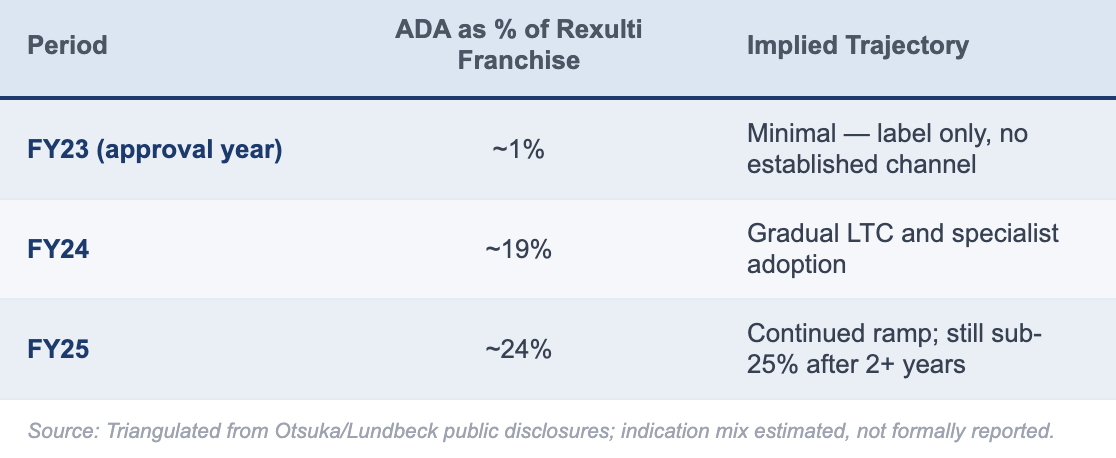

The bear case is structural, not clinical. Rexulti (brexpiprazole) was approved for ADA in May 2023 — Auvelity enters 3 years later against an entrenched incumbent with established LTC relationships, payer contracts, and embedded treatment protocols. Rexulti’s trajectory after ADA approval is instructive: the indication drove the majority of Rexulti’s incremental franchise growth over FY22-FY25, but via a gradual S-curve, not a post-approval step-function. Auvelity enters a market Rexulti created, with existing treatment inertia now working against displacement rather than in favor of adoption.

It’s Not a Pure LTC Story — Which Makes It Harder, Not Easier

A persistent framing mistake around ADA commercialization is treating it as a nursing-home-only problem. Management confirmed it directly on the 1Q26 call: the ADA treatment mix targets approximately 60% community settings and 40% LTC. That’s not a surprise — roughly 60-75% of Alzheimer’s patients reside in community settings — but it matters that management is pushing back on the LTC-dominant framing explicitly, because investor models built around nursing-home formulary penetration are solving for the wrong bottleneck.

For Auvelity, this is a double-edged finding. LTC is not the only battleground — that’s the good news. Coordinating across a fragmented dementia care ecosystem is the bad news. The ADA channel requires neurologists, geriatricians, LTC medical directors, and memory specialists — a structurally different call point from the psychiatrists who built the MDD franchise, with different workflows, different institutional dynamics, and different PA processes. It’s not that any single channel is impenetrable; it’s that five channels simultaneously is harder to execute than one.

Management (late-May 2026) cites ~80% prescriber overlap between MDD and ADA call points — but the sales force has not previously engaged long-term care, the same channel carrying the highest depression-prescriber overlap (75%). Overlap in prescriber identity isn’t overlap in commercial motion.

A Nov 2025 Alliance for Aging Research survey (n=1,000 caregivers) adds a prior layer: 73% of caregivers do not recognise agitation as requiring separate management from memory loss, and 32% hesitate to raise it with their physician. One definitional note: management anchors to 76% agitation prevalence vs. our 45% — the gap reflects clinical threshold, not data disagreement; we use clinically meaningful agitation, not any behavioral symptom. The ADA market is gated by awareness and diagnosis before it reaches prescribing infrastructure — a more improvable problem than a reimbursement barrier, but a slower one. Category education built through Rexulti’s three years in market is a tailwind Auvelity didn’t have to create from scratch.

; Rexulti penetration triangulated from Otsuka/Lundbeck public disclosures. Funnel percentages are

CLINAPTIS

estimates.")

The Speed of CNS Adoption

Cobenfy (KarXT) is an imperfect analog — different disease, different channel — but its trajectory (100% Medicare/Medicaid coverage, ~70% commercial coverage by Q4 2025, $51M in quarter five) confirms a consistent pattern: specialist CNS markets absorb new entrants slowly regardless of clinical differentiation. Rexulti is the more relevant precedent; the Cobenfy data is corroborating, not primary.

implies total Auvelity peak of ~$5.75B - requires bull ADA on a base MDD

Clinaptis analysis. MDD assumed $2.2B / $2.6B / $3.0B bear/base/bull respectively. Management

ADA figure reflects approximately equal split of \"at least $8B\" total peak guidance (Q1 2026 call);

CLINAPTIS

Street triangulated from public estimates.")

The Math the Market Is Pricing

Working backward from the current ~$11.9B EV, AXSM needs roughly $5-6B of peak Auvelity revenue to make today’s price work, assuming a mature branded-CNS margin structure of ~35% EBIT, a 12x terminal EBIT multiple, and a 10% discount rate. That is the argument. Management has now put a higher marker on the table: on the Q1 2026 call, Ari Maizel guided to “at least $8B” of annual peak Auvelity revenue, with approximately equal contribution from MDD and Alzheimer’s disease agitation. That implies roughly $4B per indication. Smoking cessation and future indications were discussed separately, so they are upside to that framework, not required to underwrite it.

The Street is not there. Current consensus implies roughly $4.5-5.0B of total Auvelity peak revenue, with the largest discount versus management on ADA. The stock at ~$250 is pricing a compromise: not management’s $8B case, not the Street’s more conservative framework, but something closer to ~$5.75B of Auvelity peak revenue. That requires ADA to become a $3B+ franchise while MDD continues to compound beyond the current base. In other words, the current price is not simply “giving credit” for ADA. It is underwriting a fairly successful ADA launch before the launch data exist.

The asymmetry is the problem.

Bull case: ADA ~$3.8B, MDD ~$3.0B, total Auvelity ~$6.8B. This requires faster-than-Rexulti ADA adoption, meaningful category expansion into undertreated patients, and continued MDD broadening through PCPs and earlier-line use. Even this bull case remains below management’s implied ~$8B framework, reflecting execution risk rather than skepticism on the addressable market.

Base case: ADA ~$2.3B, MDD ~$2.6B, total Auvelity ~$4.9B. This is broadly consistent with Street consensus and assumes a Rexulti-like ADA S-curve over 5-7 years, with MDD growth continuing but decelerating as the launch matures.

Bear case: ADA ~$1.5B, MDD ~$2.2B, total Auvelity ~$3.7B. This assumes ADA adoption is slower than expected, LTC and community-channel execution take longer to convert, and MDD’s first-line/first-switch shift does not translate into enough persistence or depth to offset natural deceleration.

Our framework is more conservative than management’s on both indications: $3.0B vs. ~$4.0B for MDD in the bull case, and $3.8B vs. ~$4.0B for ADA in the bull case. The gap is not about market size; the market is clearly large. The gap is about execution timing, channel friction, and how quickly a newly approved non-antipsychotic option can change entrenched prescribing behavior in ADA.

At ~$250, AXSM is not priced for failure. It is not even priced for a merely decent launch. It is priced for a strong ADA ramp and continued MDD durability, with limited compensation if either disappoints. That is the argument.

The Comp Set Is Not NBIX at Maturity — It’s NBIX During the Build

The most common bull framing is to anchor AXSM against NBIX as a precedent for what a durable CNS franchise deserves. That framing is directionally right but chronologically wrong. NBIX during its Ingrezza commercial build — roughly $500-700M in revenue, growing but pre-profitability, no confirmed second major indication — traded at 9-12x forward revenue, not 15-17x. AXSM at 15-17x is already pricing in NBIX-at-maturity outcomes before delivering NBIX-at-build evidence. The comp set tightens the bull case, it doesn’t expand it.

Management guided to ~$4B MDD peak — above our bull case of $3.0B. We hold the more conservative figure. Worth noting: management cited smoking cessation and future indications as upside to the $8B framework, not components of it. If that optionality is ever priced, the gap between our numbers and management’s widens further.

The multiple question and the peak sales question are the same question asked differently — both resolve on ADA.

One longer-dated consideration: ADA’s Medicare-heavy channel mix (~70%+ of scripts expected in Part D) accelerates Auvelity’s path toward IRA selection eligibility relative to an MDD-only franchise. The mechanics don’t bite until 2029-2031 at earliest — but ADA scaling toward $2B+ pulls that clock forward. Worth a line in any long-duration DCF; not a near-term catalyst either way.

MDD

MDD

$0

Bear

Base

Bull

Below current valuation

~Street consensus

~Management framework

MDD contribution

ADA contribution

---- Current price implied (~$5.75B)

ADA swing = $2.3B. MDD swing = $0.8B. MDD trajectory is unresolved - the $0.8B swing is real but bounded by

improving commercial fundamentals. ADA is where the valuation debate lives: a $2.3B swing between bear and bull,

with management explicitly guiding to ~$4B ADA peak (MDD + ADA only). At $250, the current price demands a bull

ADA outcome even if MDD delivers its base case.

Sources: Clinaptis analysis; sell-side consensus triangulated from public estimates; management guided explicitly to

≥$8B peak from MDD + ADA only (Q1 2026 call); smoking cessation and future indications cited separately as additional

CLINAPTIS

upside. All scenario figures are estimates.")

Bull Case / Bear Case

Bull — $250+ sustained

Auvelity’s non-antipsychotic profile drives faster-than-Rexulti ADA adoption. ADA exits year 2 at $300-400M annualized, validating a $3B+ peak trajectory. The 56% first-line shift embeds Auvelity earlier in prescribing behavior, extending MDD growth beyond the writer-count ceiling. Pipeline delivers a Ph3 catalyst by 2027-28. M&A optionality re-emerges as large-cap CNS buyers look for commercial-stage assets — precedented by Bristol/Karuna (~$14B) and AbbVie/Cerevel (~$8.7B).

Bear — $150-170 re-rate

ADA H2 2026 scripts track at or below Rexulti’s first-year trajectory. MDD flatness persists past Q1 seasonality. Q4 2026 guidance disappoints, triggering the multiple compression the 2026 XBI tape has applied to every name where forward revision stalls. Multiple compresses toward 10-11x NTM revenue — implying ~$150-165/share on $750M forward revenue.

What breaks the thesis: ADA weekly TRx tracking below Rexulti’s early trajectory through H2 2026. MDD failing to reaccelerate in Q2/Q3 after Q1’s sequential dip. GTN deterioration as the ADA payer mix scales, or SG&A failing to leverage off the completed 630-rep build.

Bottom Line

Axsome Therapeutics is a well-run company executing a real commercial franchise. Auvelity at $507M in FY25 revenue is not a valuation story — it’s evidence. The ADA approval is genuine optionality, not promotional noise. None of that is the argument.

The argument is $250. At 15-17x forward revenue, pre-profitability, ADA launching into an entrenched incumbent’s territory, and the pipeline unvalidated at Ph3 — the stock is pricing a specific and optimistic midpoint between Street and management. It is offering essentially no compensation for the bear scenario in which ADA tracks Rexulti-like adoption, MDD decelerates, and the multiple compresses toward where NBIX actually traded during its best commercial years. The single variable that resolves this is ADA script velocity in H2 2026. First-quarter ADA TRx data — expected through IQVIA weekly prints and Q3 earnings commentary — will either validate the $250 embedded assumption or force the reckoning the multiple has not yet priced.

NBIX is remembered as a monster winner. The market forgets it spent years trading between “too expensive” and “not expensive enough” while revenue compounded underneath. AXSM may follow the same path. The question is whether $250 is the entry point for that compounding — or the exit point before a multiple reversion the business ultimately deserves at current scale.

Disclaimer: This note is published by Clinaptis for informational and educational purposes only. Nothing herein constitutes investment advice or a recommendation to buy or sell any security. Clinaptis is not a registered investment advisor or licensed financial professional. All data and market figures referenced are sourced from publicly available information including company filings, earnings transcripts, clinical trial publications, and regulatory disclosures. Where figures are triangulated or estimated, this is noted explicitly in the text. Readers should conduct their own independent research and consult a licensed financial advisor before making any investment decision.

Clinaptis publishes independent market structure commentary on pharmaceutical and biotech categories. All views are the author’s own.