GLP-1s Solved Efficacy. They Haven't Solved Obesity

The two-leak problem in the obesity treatment funnel — and what oral drugs can and cannot fix.

The Penetration Paradox

GLP-1 prescriptions for obesity grew 309-fold between 2018 and 2025. LLY crossed a trillion-dollar market cap. NVO briefly became Europe’s most valuable company. And yet — as of a May 2026 real-world analysis tracking ~20 million patients with severe obesity — between 90% and 95% of eligible patients remain completely untreated. Not undertreated. Untreated.

That is not a rounding error. This note is not about which pill produces more weight loss. It is about why one of the fastest-growing drug franchises ever built has barely moved the needle on penetration — and whether oral GLP-1s can finally fix that.

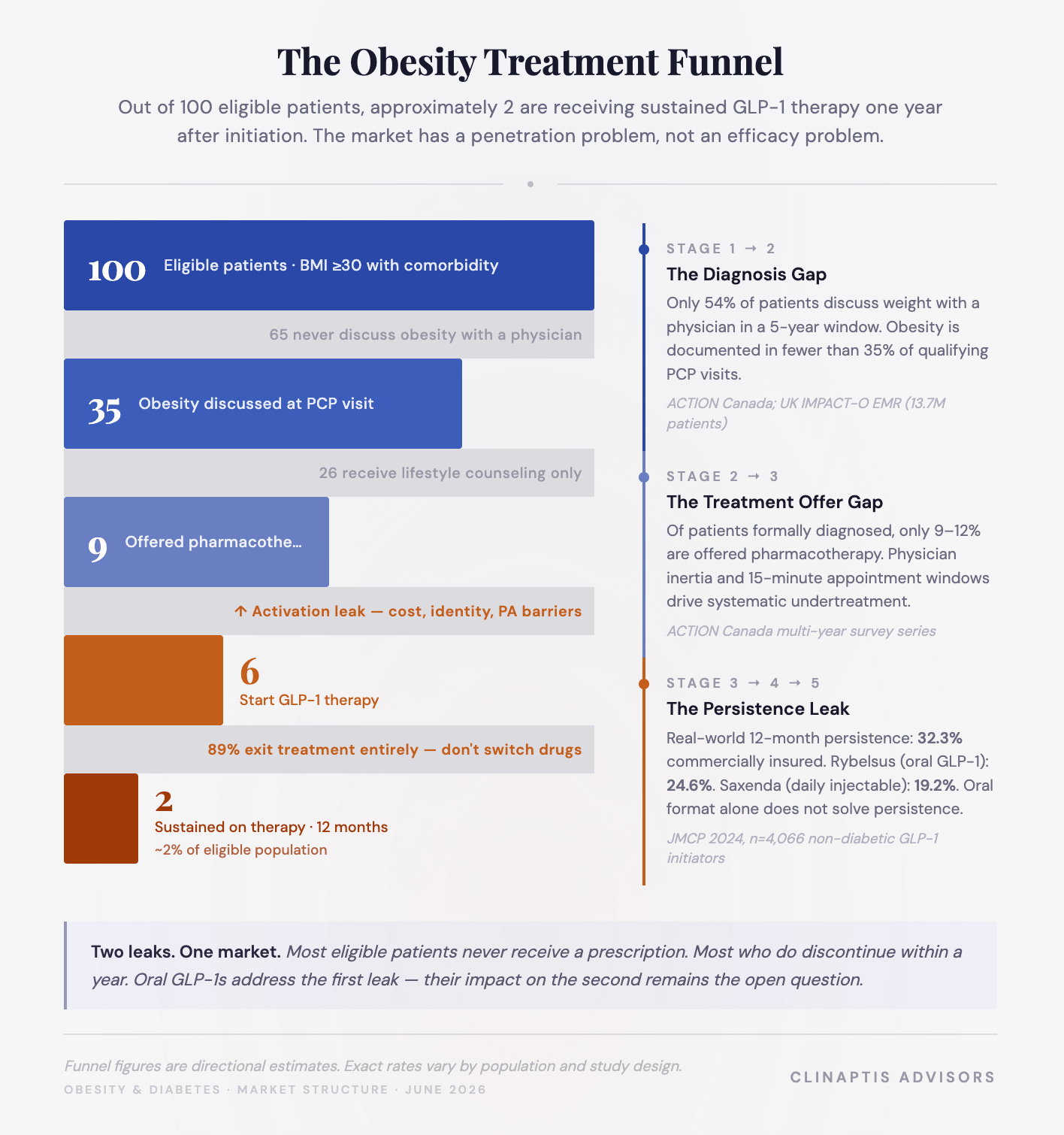

The Funnel Breaks Before the Pharmacy

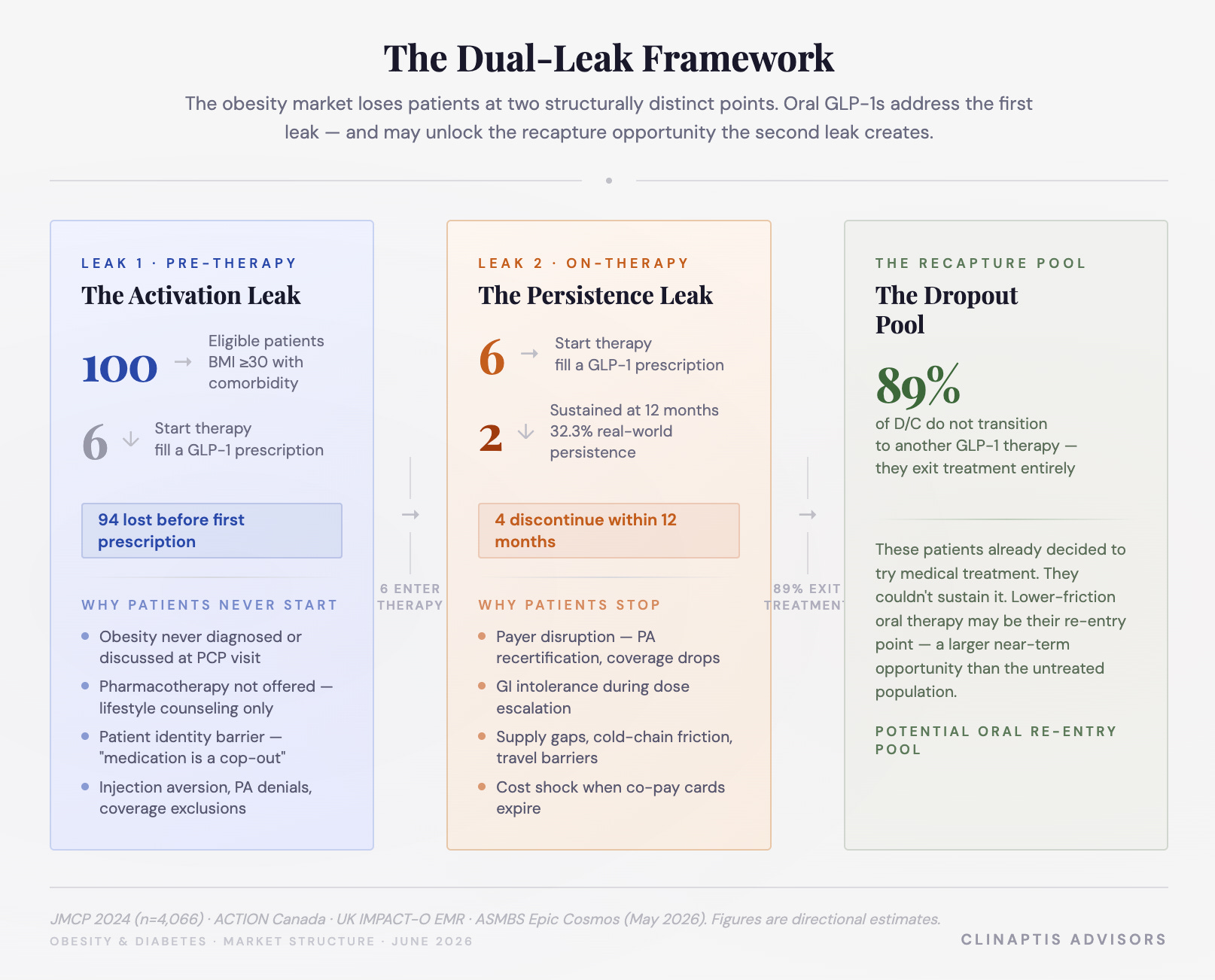

The reflex assumption is that 95% untreated means 95% unaware. The data suggests something more uncomfortable: a large fraction of eligible patients are actively inside the healthcare system and still never receive treatment. The funnel doesn’t fail at the pharmacy. It fails far earlier.

Survey data from ACTION Canada suggests ~54% of patients discussed weight with a healthcare provider in the prior five years. Of those discussions, only 9-12% resulted in a medication recommendation. The UK IMPACT-O study — EMR data from 13.7M patients — confirms the gap is wider still: among newly diagnosed obesity patients where 58% already carried at least one complication, GLP-1 utilization was 0.1%. Even among patients actively receiving obesity intervention, GLP-1 prescribing reached only 3.6% against 97% on lifestyle counseling alone (see funnel visual).

Three structural failures drive this:

Physician workflow: PCPs drive 75-80% of GLP-1 volume but operate on 15-minute windows. Obesity counseling, PA navigation, and injection training do not fit alongside hypertension, diabetes, and knee pain in a single visit.

Patient self-filtering: The ACTION 2024 Canadian mixed-methods study found patients actively removing themselves from the treatment funnel before a physician gets the chance. Among patients with mean BMI ~40, the majority had attempted diet and exercise repeatedly; fewer than one in five had ever used an AOM despite significant comorbid burden.

Identity: The barrier wasn’t awareness. Patients who entered medical treatment were statistically more likely to identify obesity as a real disease requiring lifelong management. Those who didn’t believed it should be solved through willpower first.

The funnel leak is structural, not pharmacological. And it is only the first one.

The Second Leak: Who Starts Therapy and Doesn’t Stay

Assume a patient clears the funnel. They fill the prescription. What happens next is not what the clinical trials suggested.

The most granular real-world window comes from a 2024 JMCP analysis: 4,066 commercially insured, non-diabetic adults who newly initiated a GLP-1 in 2021 with an obesity diagnosis. The core oral GLP-1 target market, tracked prospectively. The gap between trial and real world is not subtle.

At 180 days: 46.3% remained persistent. At 12 months: 32.3%. Mean proportion of days covered (PDC): 51%. Patients adherent at PDC ≥80%: just 27.2%.

Read those two numbers together. 1/3 of patients who started GLP-1 therapy for obesity are still on it a year later. Only 1/4 are taking it as prescribed. Persistence and adherence are measuring different things — one tracks whether a patient is still nominally on therapy, the other tracks whether they’re actually taking it. That gap matters more for a daily oral pill than a weekly injectable, where a missed dose is harder to ignore and easier for a physician to catch.

The product-level breakdown contains the most commercially important data in the study:

Two patterns dominate. First: weekly beats daily consistently — Saxenda’s daily injection produced less than half the persistence of Ozempic’s weekly. Dosing frequency is a major persistence driver independent of efficacy. Second, and critical: Rybelsus, the oral GLP-1 approved for T2DM, performed nearly as poorly as the worst daily injectable — 24.6% at twelve months. Oral format alone does not solve persistence. Rybelsus required a strict 30-minute morning fast with minimal water — a restriction ~40% of patients struggle to maintain long-term. The format existed. The friction was redesigned, not removed.

Two comparisons matter for Foundayo and they measure different things. Rybelsus is the persistence benchmark — a fasting-dependent oral peptide that set a low bar. Oral Wegovy, Novo’s obesity-indicated semaglutide approved Dec 2025, is the adoption comparison — same molecule as Rybelsus, reformulated for obesity, already capturing 31-33% of the Wegovy franchise within months of launch. Foundayo is running two separate races simultaneously — and the scorecards look nothing alike.

Foundayo must beat Rybelsus on persistence and close the gap with oral Wegovy on adoption. Those are separate races.

One additional finding from the discontinuation (D/C) data that most market models miss entirely: of patients who stopped in the JMCP cohort, only 11.1% switched to another GLP-1. The other 89% disappeared from treatment entirely — not to tirzepatide, not to oral semaglutide, not to Foundayo. Back to the lifestyle-only bucket, now carrying additional skepticism about whether the drugs work for them personally.

That 89% is not lost demand. It is deferred demand — patients who already decided to try medical treatment and couldn’t sustain it. In the near term, this recapture pool may represent a larger commercial opportunity for Foundayo than the purely untreated population.

Foundayo: What It Can Fix and What It Cannot

The market conversation since Foundayo’s April 2026 approval has been almost entirely about script ramp velocity, GTN dynamics, and free drug drag — benchmarking every weekly IQVIA print against oral Wegovy’s launch curve while adjusting for LillyDirect channel mix and delayed PBM coverage. The real debate is where Y2/Y3 inflection takes peak sales — a range that plausibly spans $10-25bn depending on how penetration, persistence, and net pricing assumptions resolve. That is a launch tracker with NPV attached. It is not a thesis.

Oral GLP-1s do not primarily compete with injectables on weight loss. They attack the funnel.

1. Activation leak: A PCP can prescribe Foundayo the way they prescribe a statin — no device counseling, no injection training, no needle anxiety management. For the 75-80% of GLP-1 volume flowing through primary care, that is a fundamentally different prescribing experience.

Identity Barrier: Patients repeatedly described injectables as evidence of serious chronic illness — a framing many resisted accepting. Weekly self-injection announces metabolic disease in a way a daily pill does not. For a meaningful fraction of eligible patients, the jump from “I am managing my weight” to “I am an injectable obesity patient” is one they will not make regardless of efficacy data. Foundayo reduces that jump substantially.

2. Persistence leak: More nuanced. No fasting restriction eliminates Rybelsus’s leading compliance failure. Unconstrained small-molecule manufacturing eliminates supply-driven D/C (~15-20% of injectable dropouts). No cold-chain removes travel and storage friction. Not trivial — but not yet proven at scale.

Lilly’s Ph3 ATTAIN-MAINTAIN study offers an intriguing clue. Patients switching from injectable semaglutide to oral orforglipron preserved ~79% of prior weight loss at one year; placebo patients regained substantially more. It introduces a potential new treatment architecture — injectable induction followed by oral step-down maintenance — that reframes Foundayo’s commercial logic entirely. The real opportunity may not be treatment-naïve patients. It may be the 89% of injectable D/C who currently disappear back into lifestyle management rather than switching drugs. A pill that preserves ~79% of their prior weight loss is not competing with Wegovy. It is competing with doing nothing.

The patient-selection question remains open. The oral cohort will skew toward lower baseline motivation than the injectable survivor cohort — whether that produces better or worse real-world persistence is unknown. 6-month persistence data from oral cohorts — likely emerging early 2027 — is the single most important datapoint to watch.

On early launch trajectory: The most meaningful signal is not Foundayo’s script ramp. It is oral Wegovy’s franchise penetration — 31-33% of all Wegovy prescriptions shifted to oral within months of launch. Patients will choose pills when efficacy is comparable and access is equal. That question of access is now resolving.

The Payer Ceiling

Oral GLP-1s reduce needle friction. They do not reduce cost, employer hostility, or formulary complexity. The 2026 Business Group on Health’s Spring survey is instructive: 67% of large US employers cover GLP-1s for weight management today, but only 72% expect to maintain that coverage into 2027. 10% have explicitly stated plans to drop it entirely. Seventy-one % require PA, 55% mandate step therapy, 36% require documented lifestyle program enrollment before a single script is approved. CVS Caremark’s May 28 coverage decision for Foundayo is a genuine positive — PBM channel opening, slower launch ramp partially explained. One win does not change the structural direction.

The bull and bear cases are sequential, not opposing. Oralization expands the funnel for commercially insured, PCP-managed patients — that’s real. But payer tightening may capture much of the upside that format improvements unlock, leaving net penetration gains smaller than launch enthusiasm implies. The uninsured, the employer-excluded, the patients whose physicians still don’t open the obesity conversation — a pill does nothing for them.

The payer ceiling is the constraint oral GLP-1s cannot escape alone.

The industry’s response is unlikely to stop at oral GLP-1s. Amylin-based combinations — CagriSema, petrilintide, oral amycretin — are being developed around durability and maintenance rather than peak weight loss. If the competition shifts from initiating therapy to keeping patients on it, persistence-oriented modalities may prove as commercially important as efficacy ones. That race hasn’t started in earnest. That inflection point is worth tracking closely.

How This Resolves: Three Architectures

Architecture I: The Hypertension Normalization. Oral GLP-1s become standard first-line metabolic care — easy to prescribe, broadly covered, preventive for BMI 27-35. Injectables escalate for severe and refractory cases. Penetration reaches 30-40% over a decade. This is not the statin architecture — statins normalized a known chronic disease. This is the antihypertensive architecture: drugs existed in the early 1960s, but hypertension wasn’t accepted as requiring lifelong asymptomatic treatment until Framingham propagated through clinical practice over the following fifteen to twenty years. Foundayo is closer to hydrochlorothiazide in 1965 than atorvastatin in 1997. The statin era is the destination, not the current position. At ~5% penetration today, the runway is measured in years, not quarters.

Architecture II: The SGLT2 Escape. Oral drugs absorb primary care volume, but the category fragments by indication rather than weight loss magnitude. Foundayo becomes a metabolic platform drug — OSA, OA pain, hypertension, PAD — escaping the obesity formulary fight by accumulating a clinical identity payers find harder to exclude. Lilly’s ADA 2026 presentation is already telegraphing this. The menopause subgroup poster, the hypertension work, the PAD data — no investor cares about menopause subgroup efficacy; commercial teams absolutely do. “Without food or water restrictions,” repeated in every Lilly ADA communication, is not a clinical message. It is a message to PCPs: this prescribes like your other chronic disease medications. Penetration reaches 20-25%, but the route is platform expansion, not obesity market normalization.

Architecture III: The Leaky Bucket Persists. Oralization proves easier to prescribe but not materially easier to stay on. Foundayo’s real-world persistence tracks closer to Rybelsus than Ozempic — patients entering via a convenient pill are less selected for adherence than the injectable survivor cohort. Payers tighten as utilization scales. Employer exclusions expand through 2027-28. The 95% untreated figure moves to ~88% by 2030, not 70%. Revenue grows, but the structural transformation thesis gets pushed to the 2030s. A materially different valuation picture than Architecture I implies — one that requires significant discounting of the oral TAM story.

The Chronic Disease Gap: The Problem No Pill Solves

ACTION Canada found 60% of patients agreed obesity was a chronic medical condition. In ACTION Switzerland, surveyed after semaglutide was already available, that figure was 57%. In both studies, 74-76% simultaneously believed weight management was entirely their personal responsibility. The coexistence of those two beliefs is not a statistical anomaly — it is the defining characteristic of how obesity is culturally processed. There is no obesity equivalent of the HbA1c. No blood pressure cuff in every pharmacy silently enforcing the chronic disease frame. Payers exploit this, requiring documented weight loss benchmarks for coverage recertification in ways they would never apply to a cardiovascular drug with equivalent outcomes data.

Obesity is a chronic disease. It is not yet behaving like a chronic disease market.

Foundayo participates in the cultural normalization of obesity as a treatable condition — a daily pill carries less identity cost than a weekly injection. It does not resolve the underlying gap. That shift will be driven by patient advocacy, outcomes data, and a gradual change in how the medical establishment categorizes the disease — the same forces that normalized antihypertensive prescribing across the 1970s and 1980s. The drugs arrived before the acceptance did. That is exactly where obesity is today.

Bottom Line

Out of 100 eligible obesity patients, ~2 are receiving sustained GLP-1 treatment one year after initiation. That number — derived from combining the activation funnel with real-world persistence data — should recalibrate every market model built on script growth alone.

The investors who get this right will stop arguing about efficacy and start building frameworks around penetration and persistence. The efficacy race is largely run. What remains open is whether oral GLP-1s can move the obesity market from the antihypertensive 1960s — drugs exist, acceptance hasn’t caught up — toward the statin 1990s, where chronic disease framing, payer coverage, and prescribing behavior all normalized together. That transition took cardiovascular medicine ~thirty years. The obesity market has been running for five.

The leaky bucket is real. Two holes may now be partially sealed. The payer ceiling and the chronic disease mindset gap are still open. Whether Foundayo widens the funnel fast enough to outrun payer tightening is the central commercial question of the next eighteen months. It is also, finally, the right question.

Disclaimer: Clinaptis Advisors publishes independent investment analysis on pharmaceutical and healthcare markets. Nothing in this note constitutes investment advice or a recommendation to buy or sell any security. All data and market figures referenced are sourced from publicly available information including company filings, earnings transcripts, clinical trial publications, and regulatory disclosures. Where figures are triangulated or estimated, this is noted explicitly in the text. All figures should be verified against primary sources before reliance. Clinaptis may hold positions in securities discussed.