Milvexian: AF and Stroke Indications Should Be Valued Separately

A quantitative reconstruction of BMS/J&J's Phase 3 dose-selection framework, using PK/PD modeling to independently estimate each indication's probability of success.

November 2025 changed the investment case for milvexian — just not by much, at first. BMY traded near $49/share before LIBREXIA-ACS, one of three Ph3 trials testing BMS/J&J’s Factor XIa inhibitor, stopped for futility at a preplanned interim analysis. The stock dropped to $47, bottomed at $45.79 within days, and never looked back — trading most of FY2026 in the high $50s, closing recently at $56.70. The muted reaction likely reflects that the Street had already discounted ACS as the smaller of the three commercial opportunities, not genuine confidence in milvexian’s remaining trials.

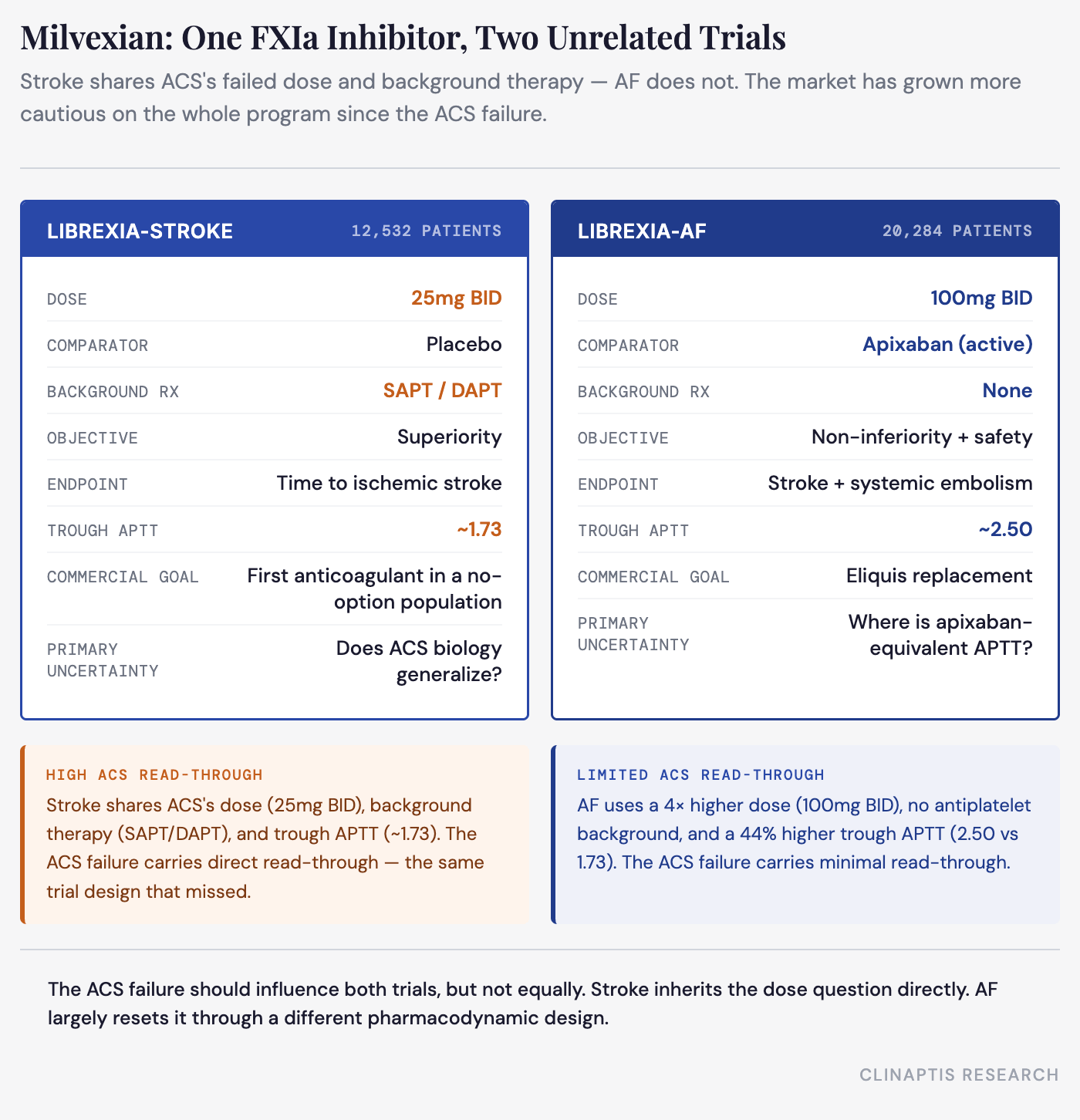

LIBREXIA-STROKE and LIBREXIA-AF remain active, sharing milvexian’s mechanism and sponsor with the failed ACS trial — and almost nothing else. Different dose, different comparator, different background therapy, different pharmacodynamic intensity. The molecule is shared. The biology isn’t — and the market has yet to price them as two separate questions rather than one.

Rather than treat ACS’s failure as a single verdict on the program, this note reconstructs each surviving trial’s dose selection independently, using a proprietary PK/PD framework (Emax model, EC50 ~630 ng/mL, R² 0.98, calibrated against a class-validating Ph3 readout) to produce externally derived, quantified HR predictions for both arms. Stroke converges tightly (HR 0.69–0.74 via four independent methods); AF’s prediction pivots entirely on a single unconfirmed APTT threshold. The dose question is largely resolved for Stroke. For AF, it’s the entire thesis.

1. The Market Priced One Failure Across Three Trials That Don’t Deserve Equal Treatment

LIBREXIA-ACS (n=14,194; milvexian 25mg BID/QD + SAPT/DAPT vs. placebo, ACS population) stopped for futility at a preplanned interim analysis in November 2025. BMS/J&J disclosed no new safety signal, and the independent DMC recommended AF and Stroke continue unchanged. Available commentary suggests a likely close miss on the efficacy endpoint rather than a decisive failure, consistent with both sponsor and investors treating ACS as the least consequential of the three trials going in.

The two surviving trials differ from ACS — and from each other — on every dimension that matters to an investor:

Stroke shares ACS’s dose, background-therapy context, and steady-state APTT exactly. AF does not. Read-through risk from the ACS failure should be treated asymmetrically — materially higher for Stroke than for AF, since Stroke shares ACS’s dose and background therapy. The market’s actual reactions don’t reflect that asymmetry: the November drawdown hit the stock broadly rather than disproportionately pricing in Stroke-specific risk, and the subsequent relief on OCEANIC-STROKE — Stroke’s own class validation — arguably should have been the larger of the two moves and wasn’t clearly treated as such.

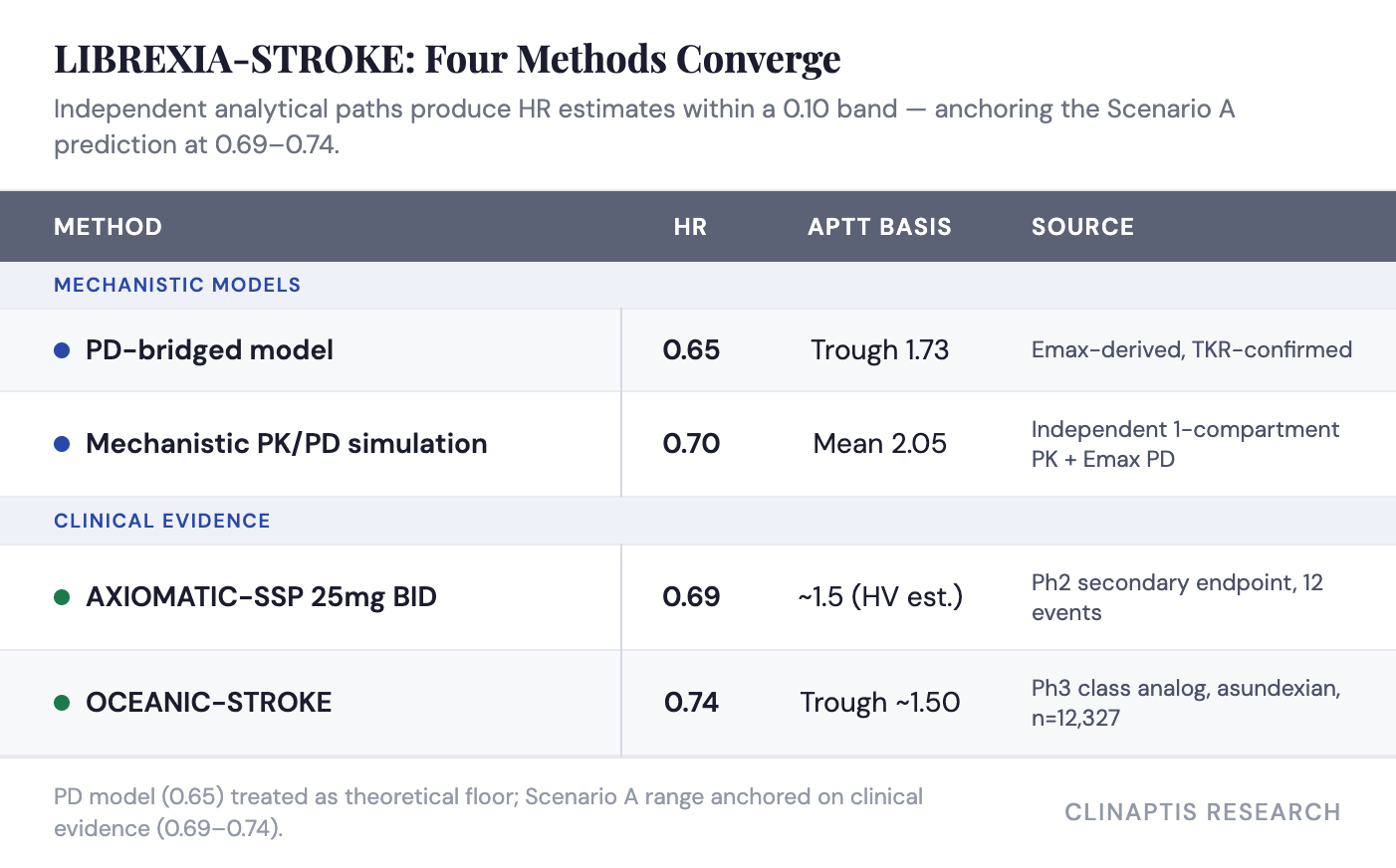

2. Stroke: The Add-On Bet Wearing ACS’s Dose — Four Methods Converge on HR 0.69–0.74

The evidence base: what Phase 2 and OCEANIC-STROKE actually showed. AXIOMATIC-SSP (Ph2, n=2,366, five milvexian regimens from 25mg QD to 200mg BID + 21-day DAPT taper) missed its composite primary endpoint — symptomatic stroke plus MRI-detected covert infarction — with relative risk ranging 0.91–0.99 across doses and no significant dose-response. The secondary endpoint of symptomatic ischemic stroke alone told a more consistent story: 25mg BID, 50mg BID, and 100mg BID converged on a 28–35% relative risk reduction (RR 0.65–0.72) against a 5.5% Pbo event rate. Major bleeding (BARC 3c/5) was not statistically distinguishable across arms — 4 events (0.6%) in the placebo arm vs. 2–5 events per active arm, with no fatal or symptomatic intracranial bleeds. The bleeding data is built on single-digit event counts and cannot reliably support a dose-response conclusion in either direction. The 200mg BID arm reversed on efficacy (RR 1.40) — the sponsor attributes this to chance, a credible reading given the event counts.

LIBREXIA-STROKE selected 25mg BID and simplified the primary endpoint to clinical ischemic stroke only, removing the MRI covert-infarct component. Both changes are favorable: the endpoint targets the specific flaw the Ph2 composite introduced, and the dose — described by the sponsor as “likely the lowest effective dose” — reflects an intentional dual-pathway strategy (background DAPT/SAPT provides baseline antithrombotic effect, milvexian adds the lowest anticoagulant intensity believed necessary on top of it). That logic is coherent and evidence-referenced. It is also the exact same strategy LIBREXIA-ACS was built on, at the identical dose, and it missed.

Bayer’s Ph3 OCEANIC-STROKE (n=12,327, asundexian 50mg QD vs. Pbo, same indication) hit its primary endpoint in April 2026 — ischemic stroke 6.2% vs. 8.4% (HR 0.74, 26% RRR, 2.2% ARR, NNT ~45), major bleeding statistically flat (1.9% vs. 1.7%, HR 1.10, NS). This is class-level validation in the identical indication and background-therapy context — a different molecule and dose, but one whose APTT has been independently characterized and can be compared to milvexian on a validated, same-assay-methodology basis.

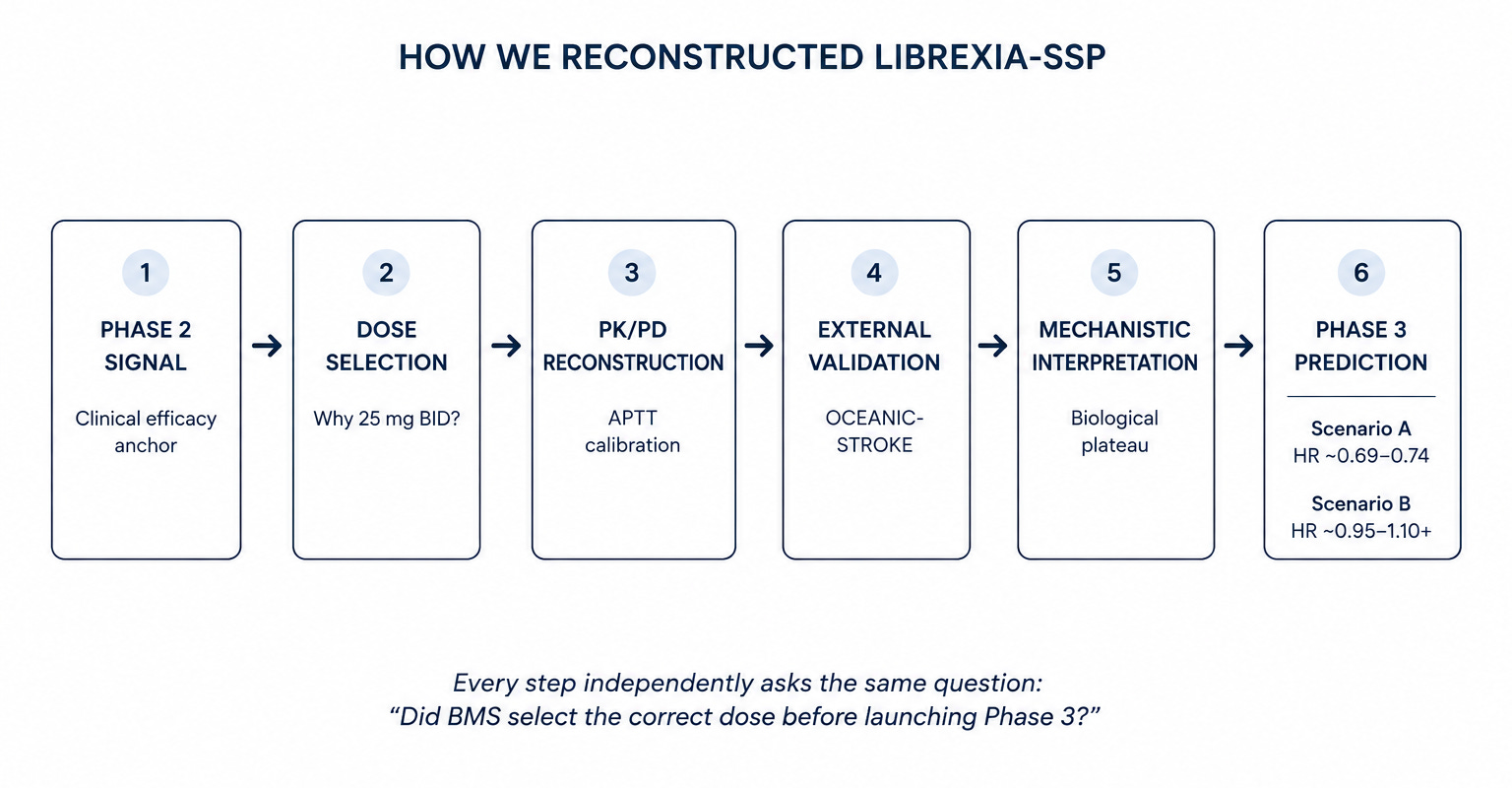

Why 25mg BID? Reconstructing the sponsor’s dose selection. We reconstructed milvexian’s concentration-APTT relationship from digitized Phase 1 healthy-volunteer data (Emax model, EC50 ~630 ng/mL, R² 0.98) and validated it against patient-derived steady-state APTT from AXIOMATIC-TKR’s Supplementary Figure S2, demonstrating consistent dose rank order, accumulation, and exposure-response. Independent PK/PD reconstruction places 25mg BID within the same pharmacodynamic window that generated the favorable Ph2 signal, supporting BMS’s dose selection before estimating the likely Phase 3 HR. Validation against patient-derived TKR data showed systematic underestimation of steady-state APTT (predicted trough ~1.50 vs. observed ~1.73–1.80), shifting 25mg BID above asundexian’s failed AF exposure (~1.50) rather than approximately matching it.

Four methods, one answer. Four independent methods now converge on a Stroke efficacy prediction within a 0.10-HR band: a PD-bridged model anchored to trough APTT, an independent mechanistic simulation (mean APTT 2.05, r=0.97 vs. Cavg), the Ph2 observed RR, and OCEANIC-STROKE’s class analog. We retain trough APTT as the primary anchor because the calibration point (OCEANIC-STROKE HR 0.74) was reported as a population-level outcome rather than indexed to a specific APTT metric. The model’s 0.65 is best treated as a theoretical floor: it moved toward the Ph2 observed value (0.69) once corrected for patient-derived APTT, internally consistent with the Ph2 dose-response.

Calibration error: MAE 0.16, RMSE 0.18, mean bias -0.16 across the three Ph2 doses.

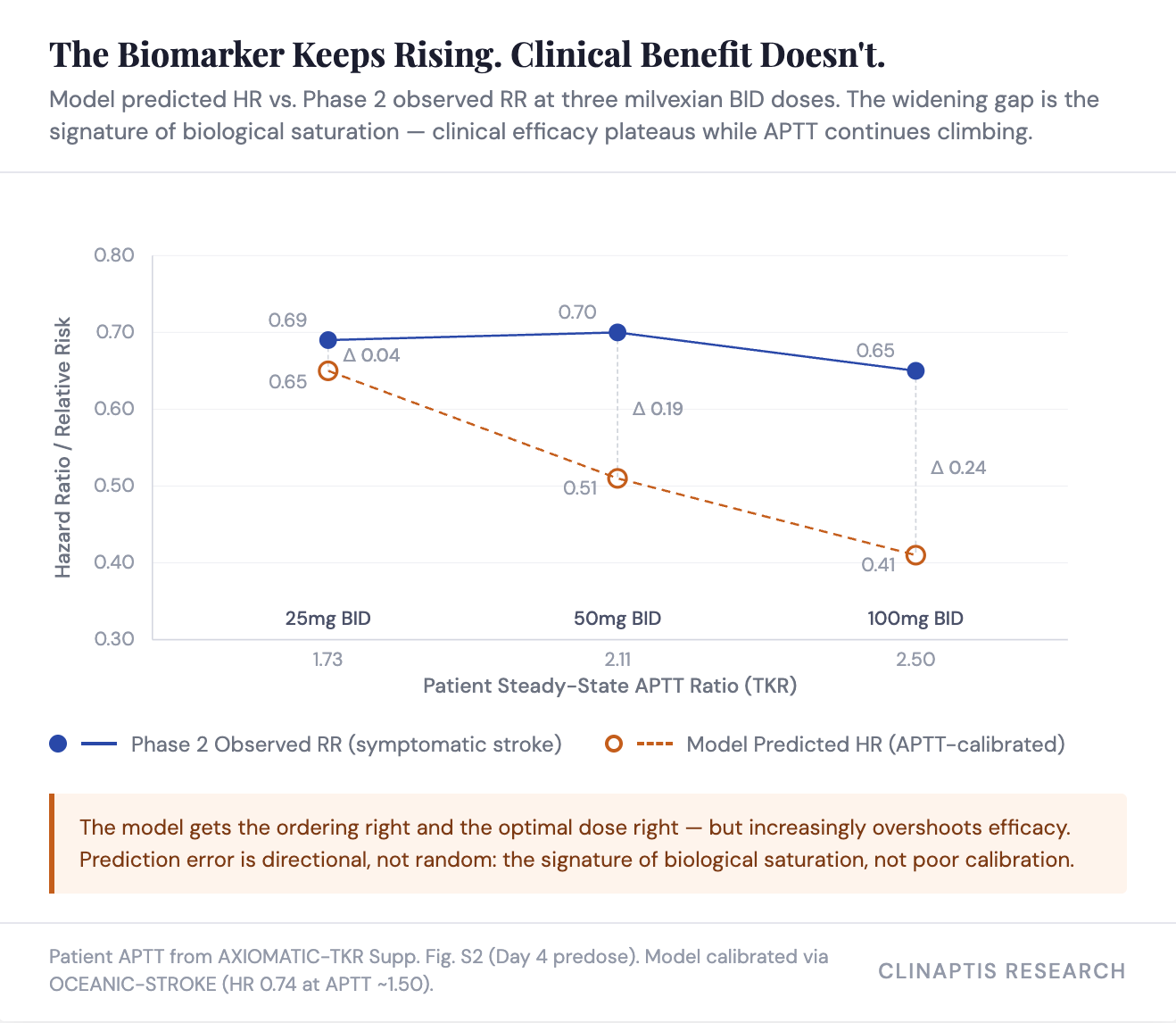

The plateau finding — and why the model overstates efficacy above the calibration point. This framework is not intended to forecast the exact trial HR; it is intended to determine whether the sponsor’s chosen dose sits on the correct side of the efficacy curve. Reconstructing what the model would have predicted for Ph2’s symptomatic stroke endpoint — the same endpoint LIBREXIA-STROKE uses — provides an internal calibration before the model reaches Ph3.

Taken together, the reconstruction suggests the model is well calibrated near the clinically selected dose but systematically overestimates efficacy once pharmacodynamic intensity exceeds the plateau. Calibration error increases monotonically with APTT — the signature of biological saturation, not poor calibration near the selected dose.

Why efficacy plateaus while APTT doesn’t — the preclinical answer. Three preclinical observations explain the plateau. First, arterial antithrombotic efficacy followed a shallow Hill slope (~0.7), so increasing exposure produced diminishing incremental benefit — a pharmacologic property of FXIa inhibition, not a trial artifact. Second, half-maximal efficacy occurred around 1.6× APTT, placing both 25mg BID milvexian (1.73) and asundexian (~1.50) near this inflection point rather than at maximal pathway inhibition. Third, FXIa inhibition suppresses thrombin amplification without directly inhibiting platelet activation (no effect on ADP, arachidonic acid, or collagen-induced aggregation), making it complementary to DAPT rather than a replacement for it — explaining why 25mg BID produces meaningful stroke prevention despite modest APTT, by targeting a different node in the cascade.

For the model, the plateau is a quantified limitation: accordingly, we anchor the Scenario A range on the Ph2 observed RR (0.69) and the class analog (0.74) rather than the model’s theoretical floor (0.65).

Note also that LIBREXIA-STROKE’s comparator bar is genuinely lower than AF’s — Pbo-controlled, not active-comparator, in a population with no approved anticoagulant option today. Any statistically clean win is commercially actionable because there is nothing to displace.

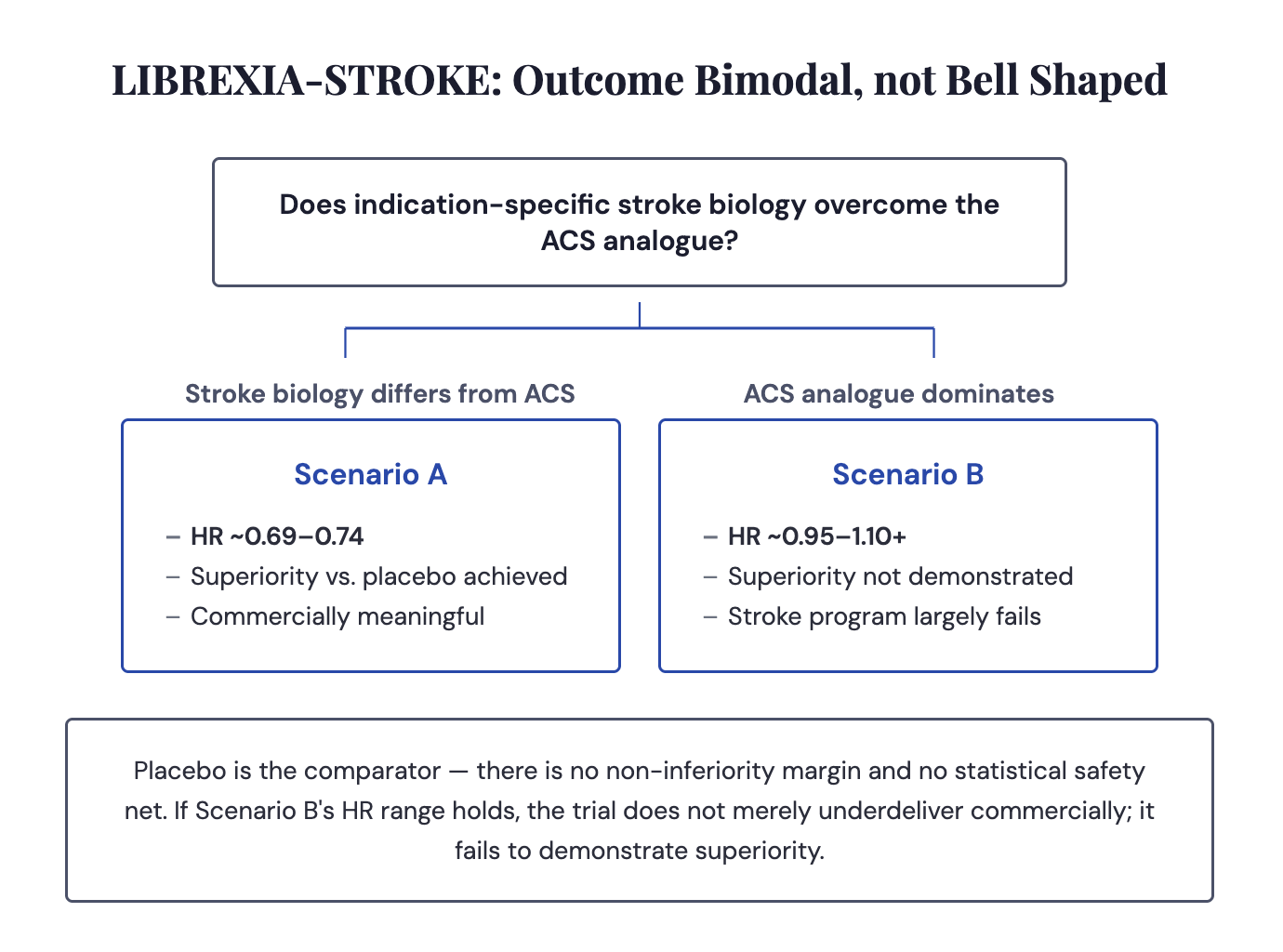

Two scenarios, not one number. The outcome is bimodal rather than bell-shaped.

Scenario A — indication-specific biology translates: HR ~0.70 (plausible range 0.69–0.74). Anchored to the four converging methods above.

Scenario B — LIBREXIA-ACS generalizes: HR 0.95–1.10+. Scenario B assumes LIBREXIA-ACS generalizes despite the mechanistic differences discussed above. The identical dose and background therapy remain the strongest bearish analogue, although no ACS exposure-response analysis has been disclosed to determine whether inadequate pharmacodynamic intensity contributed to failure. The preclinical pharmacology above suggests a specific mechanism: if acute coronary thrombosis is more dependent on primary platelet activation and less dependent on the thrombin-mediated amplification loop that milvexian targets, FXIa inhibition’s incremental contribution would be inherently smaller in ACS — consistent with a dose that clears the efficacy threshold in stroke but falls below it in ACS, even at identical exposure. This hypothesis is mechanistically plausible but remains unproven in humans.

We’re underwriting Scenario A. Four converging methods, an external class validation, and a specific mechanistic reason ACS doesn’t generalize is a stronger evidentiary position than one unconfirmed AF threshold will ever offer — which is exactly the asymmetry the AF section runs into next.

Stroke is the higher-confidence call — four methods converge inside a 0.05-HR band, backed by external Ph3 class validation. AF carries the larger prize, resting on a single unconfirmed APTT threshold public data cannot yet resolve.

3. AF: The Eliquis-Replacement Bet — Where a >$5B Thesis Pivots on One Unconfirmed Data Point (APTT)

Bayer’s asundexian (a different FXIa inhibitor) failed to prevent AF stroke versus apixaban in OCEANIC-AF (Nov 2023; Stroke/SE HR 3.79 in a high-risk subgroup — age ≥80, weight ≤60kg, or renal impairment), despite a marked reduction in major bleeding (HR 0.32). This trial changed the burden of proof: mechanism and a bleeding advantage were no longer enough — every subsequent FXIa program, including milvexian, must now show that its selected dose preserves efficacy before bleeding advantages become commercially relevant. This section addresses that question using pharmacology.

LIBREXIA-AF (Ph3, n=20,284, milvexian 100mg BID vs. apixaban, non-valvular AF, no antiplatelet background) is a non-inferiority design on stroke/systemic embolism, with ISTH major bleeding, a major-plus-CRNM bleeding composite, and a net-clinical-benefit composite as key secondaries. Per pre-ACS brokerage allocation (~50% of ~$5B risk non-adj. peak sales), this is the commercially decisive arm.

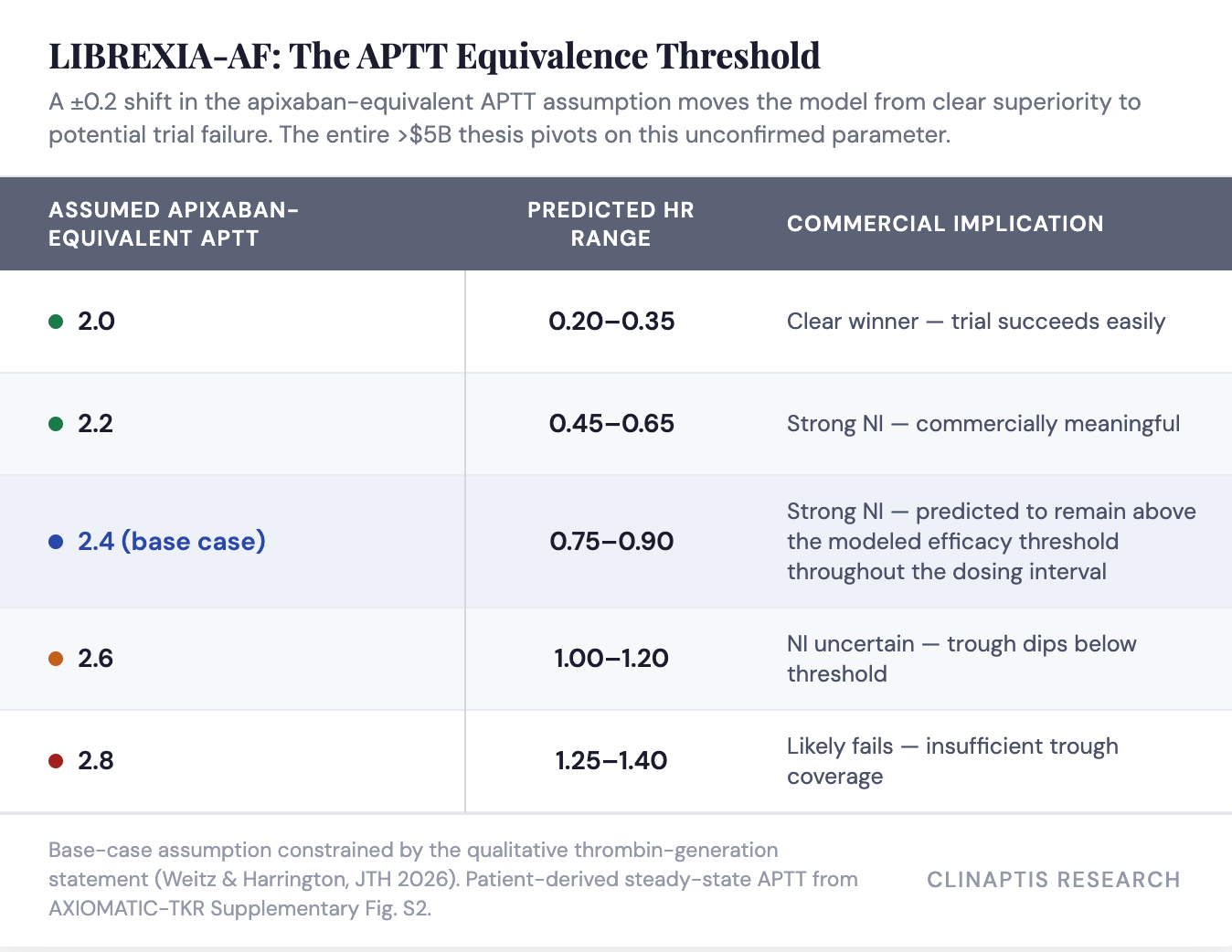

Our reconstruction suggests LIBREXIA-AF is more likely than not to achieve non-inferiority (HR ~0.75–0.90), but the prediction remains medium confidence — it depends on one unpublished pharmacodynamic equivalence assumption rather than clinical calibration. The remainder of this section explains why.

How the dose was chosen — and what it wasn’t chosen for. The dose was not derived from AF data. It was derived from AXIOMATIC-TKR — a 10-14 day orthopedic VTE-prophylaxis study — via population PK modeling and a model-based meta-analysis against apixaban’s VTE odds ratios, which identified a crossover favoring milvexian at ≥75mg BID and improving further at 100mg BID. Critically, the company’s own published account (Weitz & Harrington, JTH 2026) states that an equivalent dose-response analysis for bleeding “could not be performed,” because TKR bleeding rates were low and flat. The single most commercially important variable for this trial — bleeding differentiation versus apixaban — was not a quantified input into the dose-selection process at all.

The trial’s efficacy bar, by contrast, is rigorously derived. The non-inferiority margin (1.37) comes from an indirect comparison: warfarin-vs-Pbo (OR 0.32) combined with apixaban-vs-warfarin from ARISTOTLE (OR 0.79) implies an apixaban-vs-Pbo effect of OR 0.25. A 50%-preserved-effect fixed margin would allow 1.62; BMS chose a more conservative 1.37, preserving ~67% of apixaban’s benefit over Pbo. The asymmetry is notable — the efficacy bar was built with real statistical rigor while the bleeding differentiation the trial actually needs to matter commercially had no equivalent dose-response foundation.

OCEANIC-AF materially raises the evidentiary bar for the FXIa class. It does not, by itself, falsify the milvexian hypothesis — but the remaining uncertainty is whether it reflects molecule-specific underdosing or a target-class limitation in AF.

Why asundexian’s AF failure doesn’t read across. Asundexian at APTT ~1.50 (50mg QD trough) produced HR 3.79 versus apixaban — statistically indistinguishable from untreated risk (implied HR ~3.94, from untreated AF stroke risk ~5%/yr versus apixaban’s ~1.27%/yr, ARISTOTLE). Bayer’s chosen dose provided essentially zero incremental protection. Earlier biomarker comparisons appeared contradictory (~50% FXI clotting activity vs. >90% FXIa inhibition), but this reflects different assay methodologies rather than different pharmacology. Bayer itself acknowledged the fluorogenic assay was not clinically validated. APTT therefore provides the most defensible cross-molecule bridge.

Key finding: patient-derived TKR data imply a trough APTT of ~2.50, not the previously assumed ~2.40 — a measurable pharmacodynamic buffer versus OCEANIC-AF’s failed exposure. At patient-derived steady-state (TKR Supplementary Figure S2), milvexian 100mg BID produces trough/average/peak APTT of 2.50/~2.58/~2.66. That trough is ~67% higher than asundexian’s failed 1.50, backed by ~10x greater molar potency and 4x higher daily dose.

But the AF thesis still pivots on where apixaban-equivalent anticoagulation sits on the APTT curve. The only direct evidence is a qualitative Weitz/Harrington statement — milvexian at “therapeutic concentrations” inhibited thrombin generation “similar to apixaban” — from unpublished, steering-committee-authored data. That statement is therefore the single largest unresolved assumption in our AF framework. The TKR efficacy crossover (75mg BID, improving further at 100mg BID) narrows the range indirectly, suggesting real margin above the efficacy threshold — consistent with, not proof of, the ~2.4 base-case equivalence assumption. VTE prevention isn’t AF stroke prevention, so this constrains rather than resolves the question.

Sensitivity: the model is highly sensitive to the equivalence threshold, and relatively insensitive to every other assumption we tested.

The uncertainty therefore lies almost entirely in identifying the correct equivalence threshold, not in reconstructing milvexian exposure.

The 0.10-unit patient-derived buffer moves milvexian from dead-center on the original 2.40 assumption to sitting meaningfully above it — but the knife-edge structure is unchanged: the prediction still depends on a qualitative, unpublished data point from a non-independent source.

Why we lean toward this conclusion:

Patient-derived trough APTT adds a real 0.10-unit buffer.

TKR dose selection crossed the efficacy threshold before 100mg BID.

Independent PK reconstruction converges with the sponsor’s dose-selection methodology.

This is a medium-confidence lean, not a high-conviction call.

Bleeding: the key commercial variable. Unlike efficacy, bleeding cannot currently be modeled quantitatively because no chronic exposure-response dataset exists. The commercial framework therefore necessarily rests on scenario analysis rather than mechanistic prediction.

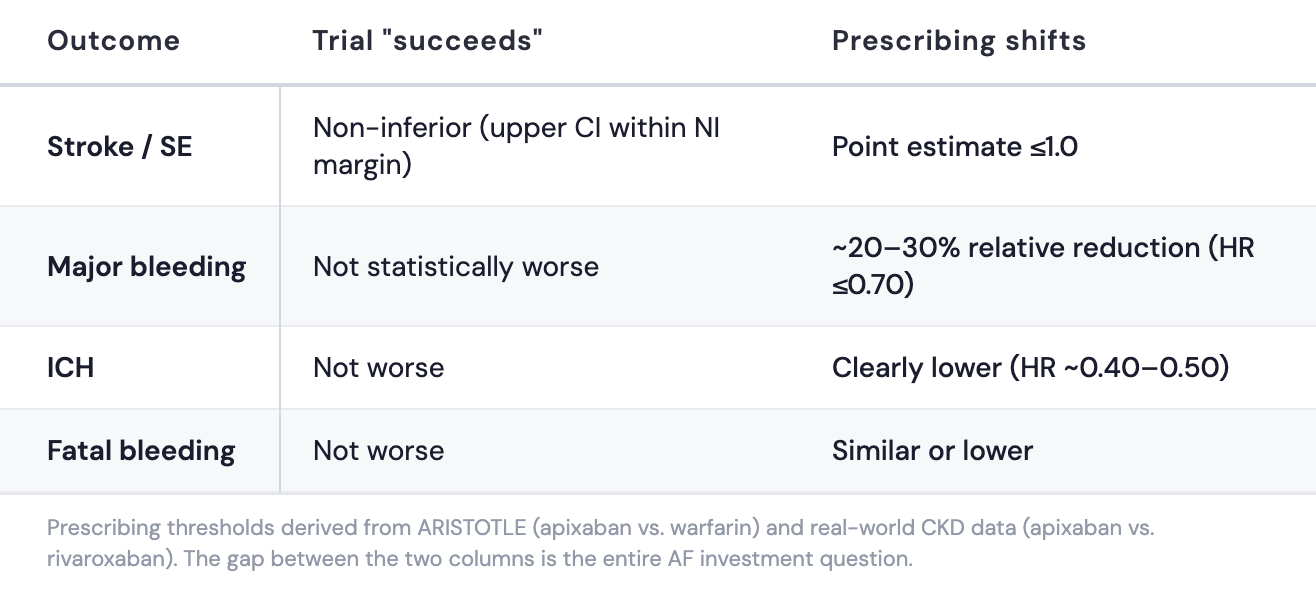

Commercial bar. Statistical non-inferiority alone does not change prescribing against apixaban, which has defended its bleeding advantage against both warfarin (ARISTOTLE) and rivaroxaban (real-world CKD data) across multiple bleeding endpoints — the table below quantifies the specific thresholds milvexian must clear. No milvexian dataset — and no FXIa inhibitor dataset at any dose — provides a reliable bleeding dose-response signal at chronic, AF-relevant exposure. LIBREXIA-AF is prespecified to test ISTH major bleeding via a graphical testing procedure — a prespecified statistical sequence that lets BMS test multiple endpoints (bleeding and stroke prevention) while controlling the false-positive rate across them. BMS built this multiplicity-controlled framework to detect a bleeding difference even without a dose-response model to predict one. The hemostasis-sparing hypothesis is the strongest mechanistic argument in the program; it remains untested at APTT ~2.50 over chronic AF-duration exposure.

Bottom line. OCEANIC-AF demonstrated that inadequate FXIa inhibition fails. Our reconstruction suggests milvexian’s selected dose sits materially above the failed OCEANIC-AF exposure while remaining within the sponsor’s own efficacy window. The remaining uncertainty is not whether the dose was chosen defensibly — it’s whether chronic FXIa inhibition can preserve apixaban-level efficacy while delivering clinically meaningful bleeding reduction.

4. What the Street Is Modeling, and Where the Model Likely Lags

Mgmt. continues to guide to >$5B global peak sales (shared equally with JNJ) without disclosing indication-level assumptions. Consensus estimates cluster around ~$3.9B risk-adjusted for the combined program, reflecting differing assumptions about clinical success rather than materially different commercial economics.

Our framework reverses the usual order. We first estimate the probability that each indication achieves clinically differentiated efficacy, then translate those outcomes into commercial value. For AF, we anchor the model to Eliquis’s existing franchise economics, asking what share of today’s ~$5.2B US AF business a differentiated successor could capture rather than what fraction of AF patients receive therapy. Stroke remains patient-based because it expands an underpenetrated market rather than replacing an incumbent.

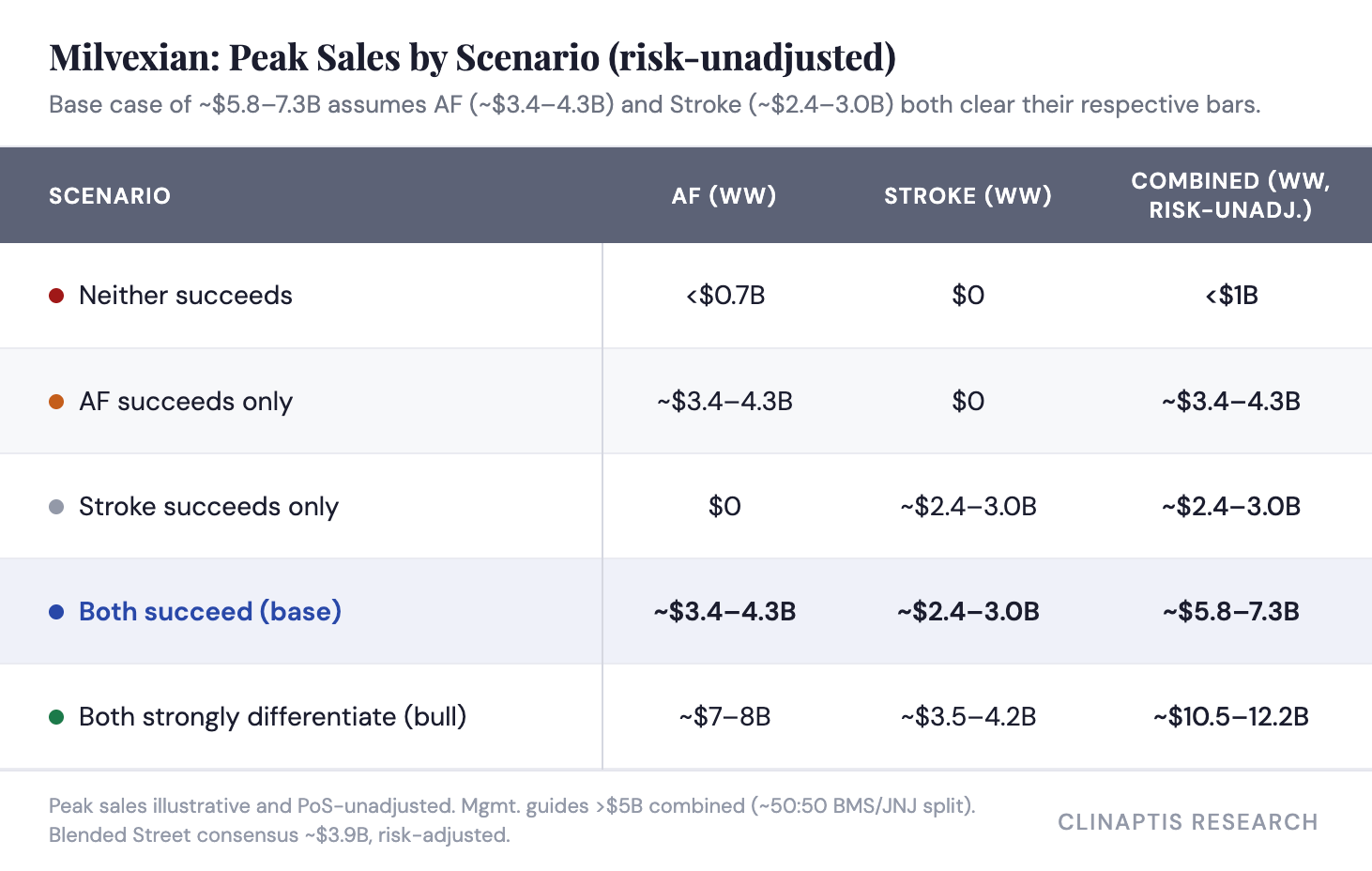

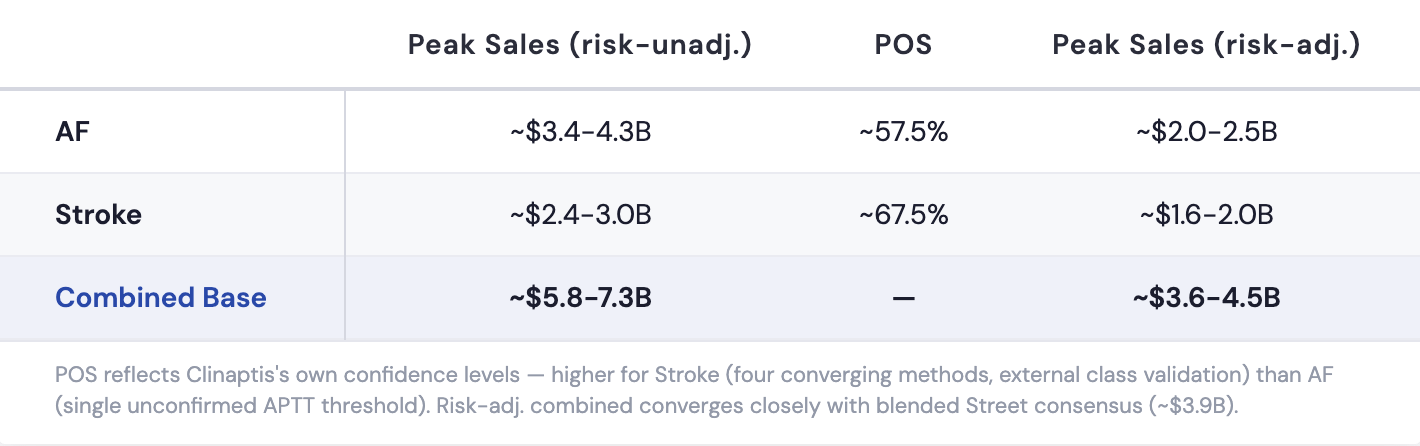

On an illustrative PoS-unadjusted basis, both-indication success supports ~$5.8–7.3B in combined base-case peak sales, with upside to ~$10.5–12.2B if AF and Stroke both strongly differentiate.

These assume pricing broadly consistent with current DOAC economics, ~9 months average treatment duration in AF and ~8-9 months in SSP, ex-US at 30-35% of US sales, and commercially achievable penetration rather than blue-sky displacement of the existing anticoagulant market.

The framework is intentionally modular. AF and Stroke are modeled independently because the evidence base, confidence level, and commercial drivers differ materially between the two indications. Combined valuation is therefore the sum of two largely independent binary outcomes rather than a single peak-sales assumption.

Our risk-adjusted figures converge closely with Street consensus at the base case — the disagreement is about probability, not economics.

Applying our own confidence levels — higher for Stroke (~65-70% POS, reflecting four converging methods and external class validation) than for AF (~55-60% POS, reflecting the single unconfirmed APTT threshold) — to our unadjusted Base case:

Our risk-adjusted Bull case is ~$6.4-7.4B.

We agree with the Street on the dollar economics. We disagree on the odds — and the reason is timing: much of consensus predates OCEANIC-STROKE’s validation of the Stroke thesis.

Bull case. AF: if the hemostasis-sparing property holds at milvexian’s patient-derived exposure (trough APTT 2.50, above the 2.4 base-case threshold for the full dosing interval), the trial delivers simultaneous NI and a clear bleeding advantage — the scenario needed to unlock AF’s upper range. Stroke: the efficacy plateau and OCEANIC-STROKE’s external validation both hold, confirming 25mg BID captures most available benefit in a placebo-controlled design with no incumbent to displace.

Bear case. AF: bleeding differentiation was never modeled at dose selection, and a result that clears NI while landing on “not worse” bleeding is a technical success that doesn’t move prescribing — the PCSK9 failure mode. Stroke: the trial replicates ACS rather than OCEANIC-STROKE, and BMS’s dosing framework credibility takes a hit extending beyond this readout alone.

Bottom Line

Stroke: Our PK/PD framework points toward HR 0.69–0.74 if the indication-specific biology holds (model floor 0.65, independently corroborated at HR ~0.70 via mechanistic simulation). That range is more bullish than post-ACS sentiment reflects. The residual risk is bimodal: four methods converge on Scenario A, and preclinical pharmacology provides a specific mechanism for why ACS failed at the same dose without generalizing to stroke (platelet-activation-dominant vs. amplification-loop-dominant thrombosis). Scenario B (ACS replay, HR 0.95–1.10+) remains live until BMS discloses the ACS exposure-response data — but it is the less-evidenced outcome, not the more-likely one.

AF: The entire prediction pivots on ±0.2 APTT units around an apixaban-equivalence threshold no published dataset has clinically confirmed. Patient-derived trough (2.50, not 2.40) provides a buffer shifting the base case from a coin flip to strong NI — but the bleeding-differentiation question that determines commercial relevance has no mechanistic model at all. This is the larger commercial opportunity (~$3.4–4.3B unadj. vs. Stroke’s ~$2.4–3.0B) riding on the thinner evidence base.

Neither question resolves the other. So, modeling milvexian as a single binary outcome is mispricing the asset regardless of which direction one leans.

Disclaimer

This note is published by Clinaptis for informational and educational purposes only. Nothing herein constitutes investment advice or a recommendation to buy or sell any security. Clinaptis is not a registered investment advisor or licensed financial professional. All data referenced is sourced from publicly available company filings, clinical trial publications, peer-reviewed literature, and regulatory disclosures. Clinaptis may hold positions in securities discussed.