Obesity: Leaders De-risked, Debate Shifting Toward Market Structure

Obesity Is Evolving From a Drug Category Into Metabolic Infrastructure

1) Category De-risked, but Leadership Hierarchy Evolving

Obesity is now firmly de-risked commercially after Wegovy/Ozempic and Zepbound/Mounjaro scaled into massive franchises (~$36B franchise revenues for both Novo’s semaglutide and Lilly’s tirzepatide platforms in 2025), representing the fastest large-scale commercial ramp in pharma history.

However, the market has clearly shifted from “infinite demand + monopoly” toward competition, pricing durability, manufacturing scale, and next-generation differentiation.

Stock performance reflects this transition:

LLY +40% in 2H25 despite modest -8.6% YTD26 pullback as Lilly maintained perceived efficacy and commercial leadership

NVO -26% in 2H25 and still -13.6% YTD26 following REDEFINE-4/CagriSema disappointment (23% WL vs ~25.5% for tirzepatide), oral competition concerns, and broader pipeline scrutiny

RHHBY +26% in 2H25 as Roche/Carmot data validated CT-388 and broader obesity platform relevance.

The transition from a supply-constrained “beta trade” toward a differentiation-led market now looks complete: Wegovy supply normalization removed scarcity premium, pricing pressure is emerging, and investors now demand incremental innovation rather than rewarding category exposure alone.

Over the last 12 months, obesity moved beyond binary efficacy validation into a differentiated “Metabolic Stack” where winners will be defined by titration elegance, lean-mass preservation, manufacturing margins, oral scalability, and platform flexibility in a post-generic world.

2) Expansion Story Intact, but Saturation Debate Now Real

The obesity TAM story remains intact, with >1B obese individuals globally and multiple adjacent indications now pulling GLP-1s deeper into chronic disease management:

CV risk reduction already validated (~14% in obesity without diabetes; SELECT study),

MASH overlap now central & commercially important (label expansion in Aug 2025),

OSA, CKD, hypertension and broader cardiometabolic studies ongoing,

while oral GLP-1s expand access into primary care, lower-BMI populations, and emerging markets.

However, the market is shifting from “peak efficacy” toward durability and persistence:

GI side effects remain meaningful (e.g. nausea >40%, diarrhea 25-30%, vomiting ~25%)

real-world injectable adherence at 12 months remains below ~40% in several datasets,

while investors now debate whether oral GLP-1s materially improve long-term persistence despite chronic GI tolerability burden.

Semaglutide LOEs beginning March 2026 across India, China, and Brazil are beginning to reshape long-term market structure:

India + China alone account for roughly ~25% of the world’s obese adult population

Indian generic semaglutide pricing has already fallen toward ₹450/week ($5) versus branded pricing closer to ~₹6,000/week,

implying real-world pricing compression approaching 80–90% in some emerging-market channels post-generic entry.

Obesity may ultimately evolve more like:

oncology (continuous premium innovation),

or MDD/dyslipidemia (where commoditization foundational therapies coexist with premium next-generation agents).

That distinction may define the next decade of metabolic medicine.

3) Oral GLP-1s Become Distribution and Scalability Innovation

Biggest catalyst of past year arguably was Eli Lilly’s Orforglipron Phase 3 success, validating a small-molecule oral GLP-1 with “injectable-like” efficacy, no food/water restrictions, and materially simpler manufacturing/distribution economics versus injectable peptides.

The oral debate is less about efficacy and more about:

manufacturing scalability,

lower COGS,

freedom from cold-chain logistics,

primary-care penetration,

and emerging-market distribution.

Foundayo launch scripts initially lagged Oral Wegovy (~5.6K week-3 scripts), while Oral Wegovy scaled toward ~134K weekly scripts by week 16 following its January 2026 launch. However, Jefferies still models ~$1.6B 2026 sales and ~$30B peak sales potential for Foundayo, reflecting belief that oral GLP-1s could massively expand the obesity funnel globally.

Commercialization already looks structurally different from traditional pharma:

~45% of Foundayo scripts flowed through LillyDirect,

~35% via telehealth,

and only ~20% through traditional retail,

highlighting how obesity is evolving toward a hybrid consumer-tech / DTC healthcare / subscription medicine model that partially bypasses traditional pharmacy infrastructure.

GPCR remains one of the more interesting oral platform names:

+230% in 2H25 following ACCESS-II data before correcting ~40% YTD26,

while Roche’s $100M CT-996 licensing agreement reinforced the growing strategic value of oral GLP-1 chemistry/IP protection.

Increasingly, the key question is no longer “can oral GLP-1s work?” but:

“Can they get close enough to injectable efficacy while being cheaper, easier, and globally scalable?”

4) The Metabolic Backbone Thesis

GLP-1s are expanding beyond weight loss into broader chronic disease management:

MASH,

cardiometabolic disease,

obstructive sleep apnea (OSA),

CKD,

hypertension,

positioning obesity therapies as foundational metabolic treatments rather than isolated obesity drugs.

The strongest strategic implication is “Indication Encroachment”:

Multi-indication metabolic platforms are pressuring single-indication specialty categories, particularly in MASH where incretin overlap will compete against standalone liver franchises.A March 2026 meta-analysis showing GLP-1s improved fibrosis without worsening MASH (RR ~1.59) materially strengthened the “metabolic backbone” thesis and pressured standalone liver franchises.

MDGL rallied +94% in 2H25 as Rezdiffra, the first approved MASH therapy, scaled to ~$311M quarterly sales by Q1 2026 and exceeded many early commercial expectations (launch trajectory).

However, the long term debate centers on whether standalone MASH therapies ultimately become niche second-line agents layered on top of GLP-1 backbones rather than foundational therapies themselves.

Payer incentives now favor integrated metabolic platforms spanning obesity + CV + liver + renal risk rather than multiple siloed specialty therapies.

Which is why obesity is no longer just a weight-loss category. Obesity now sits closer to foundational metabolic infrastructure than a standalone weight-loss category.

· GLP-1 prescriptions remain heavily concentrated within Commercial plans (~81% of claims), while Medicare access remains tightly restricted despite expanding cardiometabolic indications. Following cardiovascular-risk expansion, Wegovy Medicare Part D approval rates only improved from ~12% to ~20%, while Zepbound’s OSA indication drove approval rates from ~10% to ~28%.

· Reimbursement friction remains substantial beneath the category’s growth narrative. GLP-1 gross-to-net (GTN) discounts already range from ~23–45%, while patient out-of-pocket costs exceeding ~$800/month drove treatment discontinuation to >50% in some datasets (IQVIA).

5) Next-Wave Obesity Competition Intensifies

The obesity pipeline is rapidly moving beyond first-generation GLP-1 monotherapy:

Roche’s CT-388 Phase 2: 22.5% placebo-adjusted WL at 48w, with ~48% achieving ≥20% WL and 26% ≥30% WL, positioning Roche as a credible large-cap obesity player behind Lilly/Novo

Eli Lilly’s Retatrutide remains the upper-end efficacy benchmark (~24.2% WL at 48w in Phase 2)

VKTX stabilized after its prior speculative unwind as investors reassessed the strategic value of its oral and subcutaneous VK2735 (GLP/GIP) following data that compared favorably against earlier tirzepatide benchmarks.

ZEAL.CO / Roche combination strategy further strengthened the amylin narrative after ZUPREME-1 data showed ~10.7% WL with “placebo-like” tolerability, while Roche initiated Petrelintide + CT-388 combo development in Q2 2026.

Market is rewarding:

Durability and tolerability

functional mobility preservation,

and combo flexibility

rather than headline weight-loss alone.

Investors are now distinguishing between:

“high-efficacy obesity assets”

versus “scalable chronic metabolic platforms”

which are not necessarily the same thing.

At the same time, much of the next-wave obesity pipeline already carries significant strategic premium before the long-term durability, scalability, or commercial differentiation are fully proven.

The debate shift:

“Which drug loses the most weight?” → “Which platform remains differentiated once obesity becomes crowded, segmented, and partially commoditized?”

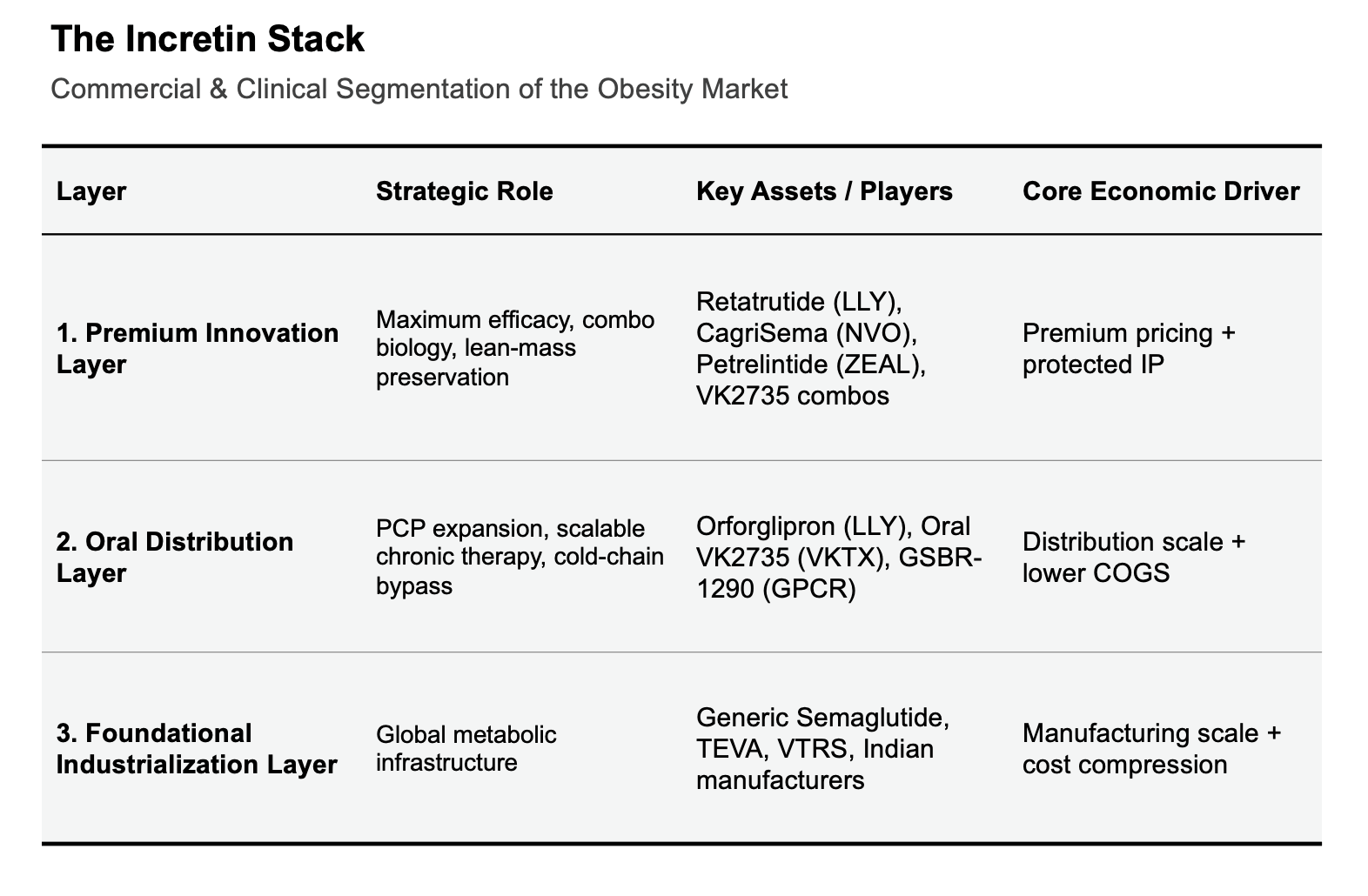

6) Market Structure Bifurcating: Innovation vs Industrialization

The obesity market is splitting into two parallel ecosystems:

Frontier Innovation: LLY, RHHBY, AMGN focused on potency ceilings, oral non-peptides, combinations, and next-generation metabolic architectures

Industrialization Layer: TEVA, VTRS, Dr. Reddy’s Laboratories, Biocon, Divi’s Laboratories focused on peptide manufacturing, fill-finish scale, APIs, CDMOs, and post-LOE metabolic care.

The March 2026 semaglutide LOE in India marked a catalyst event for the industrialization layer:

over 10 manufacturers launched versions within days,

vial-format semaglutide pricing rapidly compressed toward ~$15–25/month,

representing roughly ~90% discounting versus innovator pricing in some channels.

Importantly, while India moved immediately post-LOE, China remains under a more complex administrative stay into late 2026, though local manufacturers are stockpiling API and positioning aggressively for launches.

As efficacy differentiation compresses and semaglutide industrializes post-LOE, investors will focus on who captures manufacturing, supply-chain, and distribution economics beneath the innovation layer.

Stock performance underscores this structural transition:

TEVA (+88% in 2H25) benefited from better appreciation of its CDMO and manufacturing positioning

VTRS (+40% in 2H25) rallied after confirming expected regulatory decisions for complex generic GLP-1 candidates by YE26.

Obesity looks less like a single-drug category and more like semiconductors:

innovators design the architectures,

but manufacturing foundries, peptide yields, supply chains, and distribution infrastructure increasingly determine who captures the long-duration economics.

The next phase looks like a fight over manufacturing scale, distribution architecture, reimbursement persistence, and who ultimately controls the global metabolic supply chain.