Orexin and Narcolepsy

What the first orexin agonist approval in Narcolepsy Type I (NTI) actually validates.

The FDA is about to approve the first targeted and arguably disease-modifying agent in narcolepsy. The more interesting question is what it actually validates.

Takeda’s oveporexton (TAK-861) has a PDUFA date of Sep 30, 2026 — and if two Ph3 studies meeting every primary and secondary endpoint at p<0.001 are the guide, it will become the first orexin receptor agonist ever approved. That matters beyond the catalyst. Excessive daytime sleepiness (EDS) disorders have been managed for decades through mechanisms that compensate rather than correct — stimulants forcing wakefulness through dopamine and norepinephrine, oxybates consolidating nighttime sleep, pitolisant raising histaminergic tone. Each addressed a symptom; none touched the underlying biology. Orexins attempt something categorically different: replacing the missing wakefulness signal itself. NT1 is caused by the autoimmune destruction of up to 90% of the neurons that produce orexin-A — biology established in the late 1990s, a drug 25 years in the making.

With approval now probable, the investor debate is shifting from launch mechanics to a more asymmetric question: does orexin agonism expand the clinical narrative beyond wakefulness normalisation? That distinction will sharpen through 2H26 — the first stress test arrives at SLEEP Baltimore (Jun 14-17), where ALKS 2680’s full NT2 Ph2 data will provide the earliest read on whether orexin amplification works in an orexin-sufficient population. The broader platform debate plays out as ALKS, Centessa/Lilly, and Takeda each present against a widening endpoint universe.

This note is about where the validated signal ends and where the platform bet begins.

I. The Market Jazz Built

Jazz spent two decades building the modern narcolepsy market through prescriber education, label expansion, and franchise defense that absorbed both generic oxybate entry and pitolisant (Wakix) competition without losing the premium tier. The output as of Q1 2026: ~11,075 Xywav NT1 patients, ~8,500 on Wakix, ~6,000 residual Xyrem, and Lumryz (now Alkermes post-Feb 2026 acquisition) implying ~4,500-5,000 patients on $350-370M full-year guidance. Total active premium market: ~22-25K — modest against 160K total US NT1 prevalence, but its composition matters more than its size.

Jazz has presumably treated ~80K NT1 patients over two decades. Against a current active base of 22-25K, that implies a ~20% long-term retention rate — not a drug failure, but a tolerability and access attrition figure. Sodium oxybate carries a black box warning, a restricted REMS program, and twice-nightly dosing; the 20-30% Day 30-45 D/C rate is a compliance ceiling built into the therapy’s physical architecture. The ~55-60K patients who initiated premium therapy and dropped back to PCP-managed generic methylphenidate did not leave because narcolepsy improved. They left because the available therapy was harder to stay on than the disease was to tolerate untreated. At ~$100K annualised net revenue per patient — the Xywav benchmark — that attrition stack represents a $5.5-6bn ‘theoretical revenue pool’ in a population the healthcare system already knows by name. Oveporexton doesn’t need to take share from Xywav. It needs to reactivate the attrition stack — and the prescriber infrastructure to reach that population already exists.

II. Why the Biology Took 25 Years to Drug

The orexin system operates through two receptors: OX2R, which drives sustained wakefulness, and OX1R, linked to autonomic and reward pathways. Activating OX1R non-selectively produces the AE profile that killed early programs — CV fluctuations, hemodynamic instability, anxiety-like activation. Once orexin deficiency was established as a core driver of NT1, the primary uncertainty shifted from biological rationale to druggability: building a molecule with sufficient CNS penetration at OX2R while maintaining selectivity to avoid OX1R-mediated toxicity.

Takeda’s first serious attempt, TAK-994, answered the pharmacology question — and created a new problem. Ph2 efficacy was compelling; the hepatotoxicity that terminated the program in late 2021 was not, later traced to reactive metabolites specific to that scaffold (Shinozawa et al., 2025). Oveporexton, ALKS 2680, and ORX750 use structurally distinct scaffolds with clean hepatic profiles across multi-week exposure. Jazz/Sumitomo’s JZP441 — halted in Ph1 in November 2023 on visual disturbances and CV signals — reinforced the same point from a different angle: the therapeutic window is narrow and molecule-specific. Orexin biology was not failing. Drug design was.

Oveporexton is not introducing regulators to orexin biology for the first time. Three dual orexin receptor antagonists — suvorexant (Belsomra, 2014), lemborexant (Dayvigo, 2019), and daridorexant (Quviviq, 2022) — have given the FDA nearly a decade of experience evaluating orexin pathway modulation in humans. What that history established was the pathway. What it did not establish was the inverse proposition: that activating orexin could safely restore wakefulness. The pathway was validated. The direction was not.

Oveporexton validated the direction. Across two registrational Ph3 studies — FirstLight and RadiantLight, 19 countries — mean MWT improved from ~4-5 min at baseline to 21.8 min (FirstLight) and 24.6 min (RadiantLight) at Wk12, with 63% of patients achieving normative wakefulness (≥20 min) — 4-5× the ~3-5 min improvement historically seen with modafinil. ESS fell from ~17-19 to 6-7, normalizing in ~85% of patients, while cataplexy frequency declined 79-89%. No serious treatment-related AEs were reported across either study. More than 95% of completers entered the ongoing long-term extension — an unusually strong continuation signal in a disease where 20-30% D/C premium oxybate within 30 days.

The pathway was established years ago. Oveporexton demonstrated that it can finally be drugged.

III. NT1 Is the Beachhead, Not the Market

Oveporexton validates one proposition: replacing absent orexin in NT1 restores wakefulness. NT1 is replacement therapy. The neurons are gone. The drug fills the void.

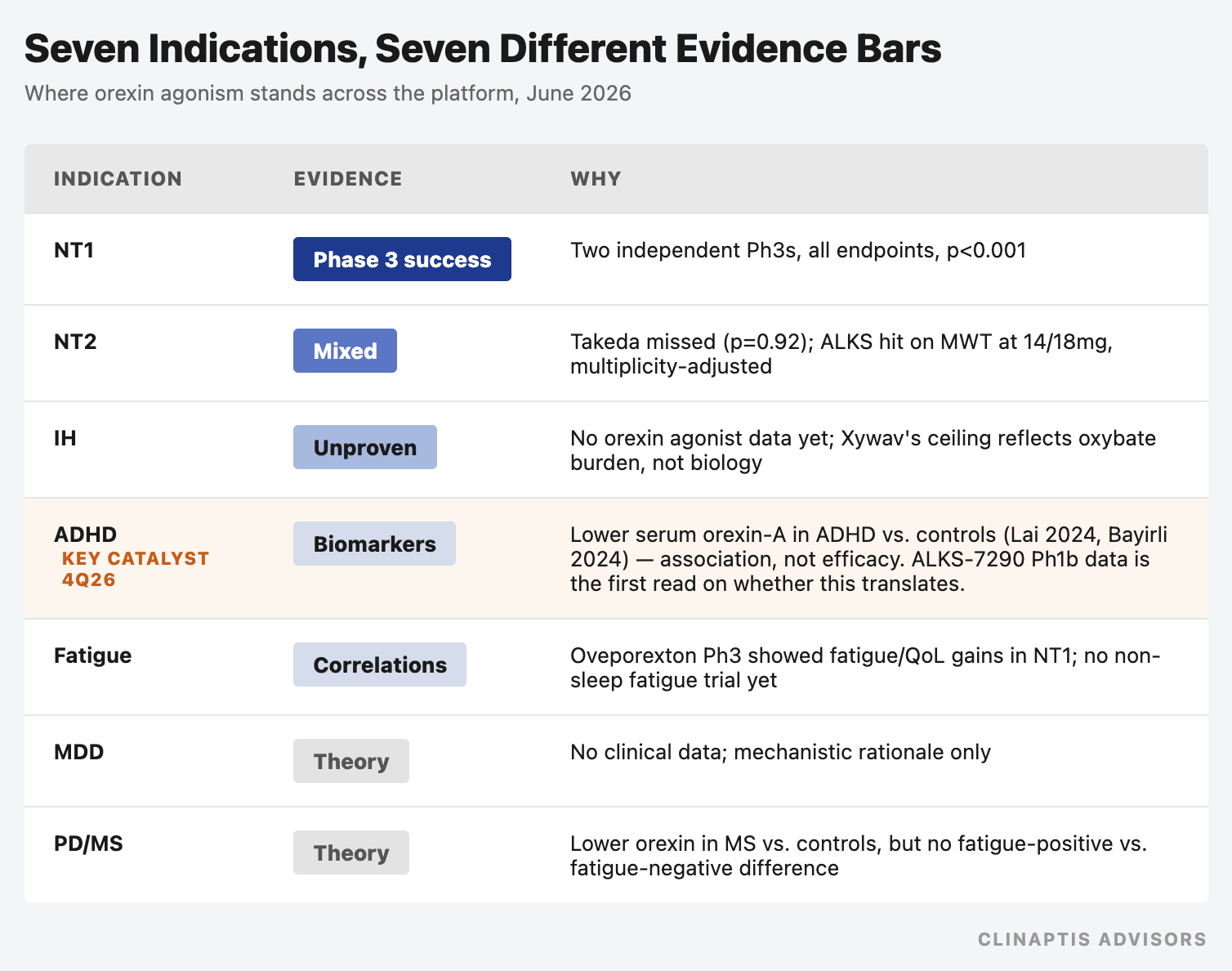

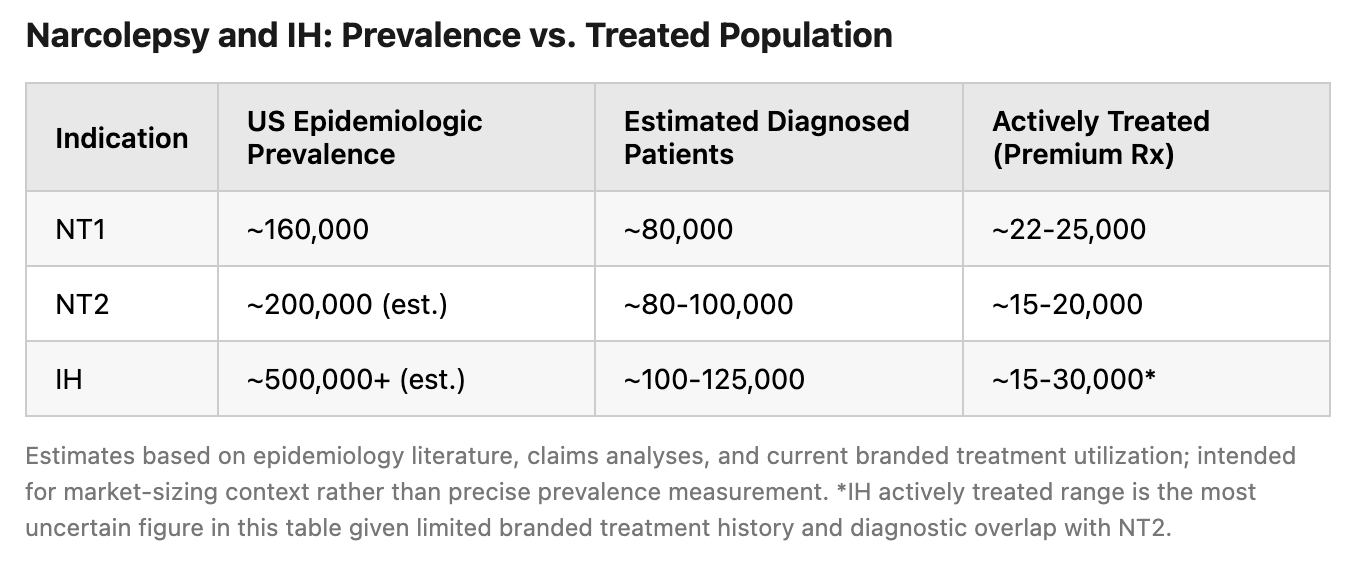

NT2 and IH are structurally different — and the population numbers require precision, since applying penetration rates to the wrong denominator can shift a peak sales model by a factor of five:

The gap between prevalence, diagnosis, and active treatment reflects different bottlenecks. Orexin agonists can address treatment attrition faster than diagnostic under-recognition, making actively managed patients the more useful starting point for framing commercial opportunity than epidemiologic prevalence.

NT2/IH patients are not orexin-deficient — CSF orexin levels are normal. The hypothesis behind ALKS 2680 and ORX750 in these indications is amplification, not replacement: a sufficiently potent OX2R agonist can hyper-activate wake-promoting pathways above normal orexin tone. Early support for the underlying pharmacology came from healthy, sleep-deprived volunteers — Centessa’s Ph1 data (World Sleep 2025) showed ORX750 at ≥2.5mg producing continuous mean MWT latencies >30 min in non-deficient subjects. The more important test, however, is whether this translates to actual NT2/IH patients.

Takeda has already run this experiment in actual patients. TAK-861-2002, an NT2 Ph2 study, did not meet prespecified efficacy criteria — MWT improved +2.4 min vs. placebo at the high dose (95% CI: -3.9 to +8.7, p=0.92), directionally positive but not statistically significant in a 71-patient trial. Takeda subsequently discontinued NT2 participants from the oveporexton LTE and is instead advancing TAK-360, a dual OX1/OX2 agonist, into NT2 and IH — a molecule switch, not merely a pause.

ALKS 2680 — also OX2-selective, the same general mechanistic class as oveporexton — subsequently produced a more encouraging NT2 signal: in Ph1b data presented late 2025, MWT improved 6.7-9.3 min vs. placebo, with the 14mg and 18mg doses reaching significance even after multiplicity adjustment (p=0.0485, p=0.0466). The dose range is the detail worth sitting with. Oveporexton’s own NT1 data shows AE rates roughly doubling between 2mg and 5mg (pollakiuria 13%→33%, insomnia 9%→21%) — and TAK-861-2002 tested only up to 5mg. ALKS 2680’s NT2 study went to 18mg. One receptor, two molecules, two different therapeutic windows — and the simpler explanation doesn’t require invoking OX1 biology or a different mechanism: oveporexton may have been dose-capped before it could reach NT2-relevant exposure, while 2680 wasn’t. Takeda’s own interpretation, via TAK-360, is that NT2/IH require different pharmacology entirely. Both readings remain open. What’s no longer open is the assumption that NT1 approval mechanically de-risks NT2 — Takeda’s own molecule argues the opposite.

The IH benchmark is Xywav. Despite being the only approved therapy since 2021 and Jazz’s established sleep infrastructure, active IH patients numbered only ~5,525 by Q1 2026. The limitation appears practical rather than biological: oxybates work, but the compliance burden constrains adoption. Orexin agonism is the test of what happens when that burden is removed.

The commercial question in NT1 is adoption. The scientific question in NT2/IH is whether amplification works at all — and the first two attempts to answer it disagree.

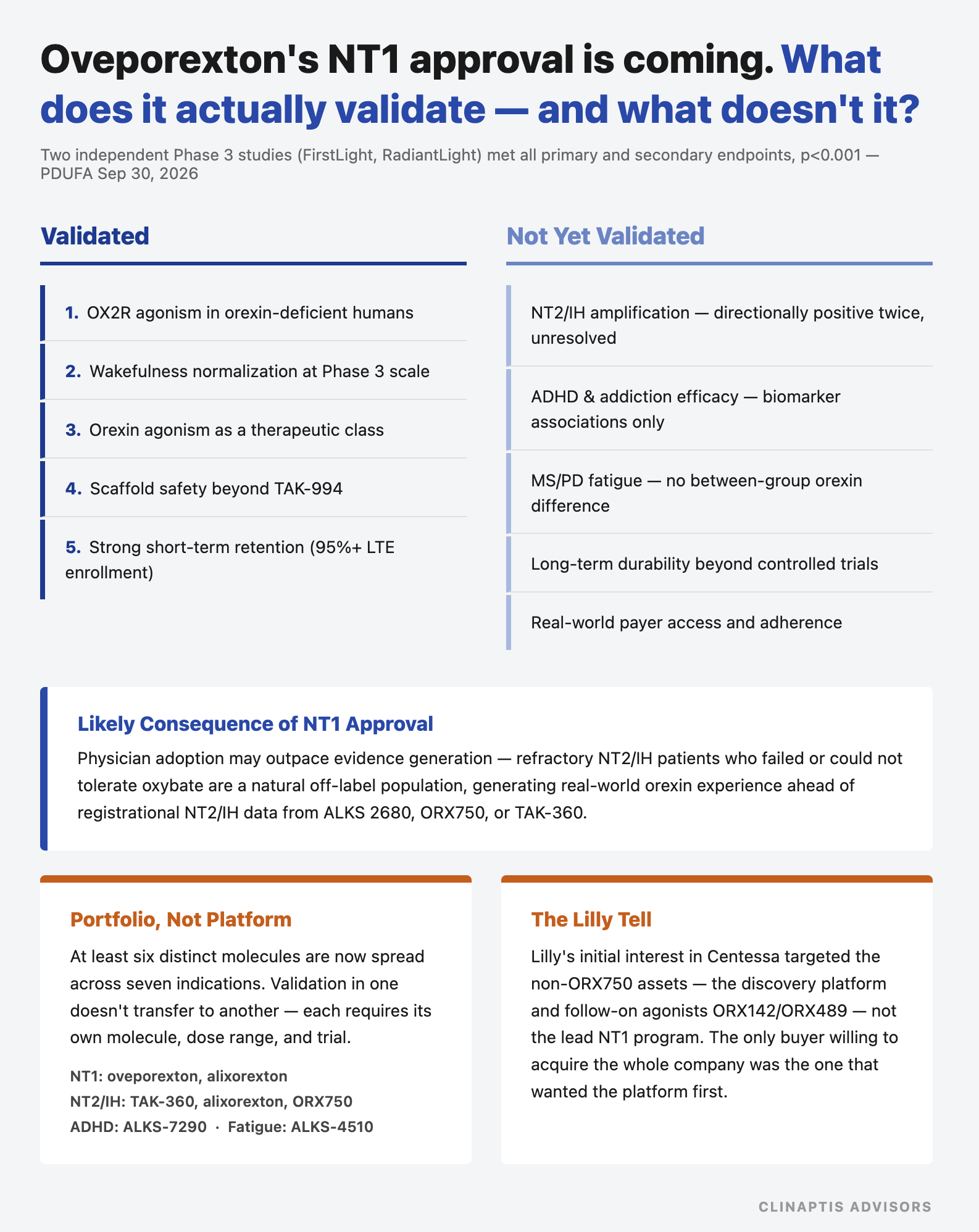

IV. What NT1 Approval Does and Does Not De-Risk

The question that matters most heading into the PDUFA:

De-risked: OX2R agonist mechanism in orexin-deficient humans at Ph3 scale. Hepatic and CV safety (next-gen scaffolds, distinct from TAK-994). Prescriber willingness to adopt once-daily oral therapy in NT1. 95%+ patient retention at 12 weeks.

Not de-risked: Amplification hypothesis in NT2/IH — directionally positive in both attempts so far, but unresolved (Section III). Orexin agonism in ADHD. Orexin agonism in addiction. Orexin agonism in MS/PD fatigue. Each requires independent proof.

ADHD is the most important non-sleep indication — not because it is the most validated, but because positive data here would meaningfully strengthen the bull case for ALKS’s broader orexin platform. Lai et al. (2024, 283-patient pediatric cohort) and Bayirli et al. (2024, adults) both found serum orexin-A levels associated with ADHD status and executive function — human studies, not mouse extrapolation, but still biomarker observations rather than therapeutic evidence. ALKS’s ~$7.5bn market cap has accrued substantially over the past 12 months on the strength of the broader orexin platform narrative; ALKS-7290’s Ph1b ADHD MAD data expected 4Q26 is the first test of whether that narrative extends to ADHD specifically, or stays confined to NT1/NT2/IH.

The addiction signal — higher baseline orexin at smoking cessation correlating with ~30% lower relapse; rising orexin with meth abstinence length — is correlational only. The MS/PD fatigue data shows orexin levels lower in MS patients vs. controls, but fatigue-positive and fatigue-negative MS patients show no meaningful difference. Biomarker abnormality is not therapeutic target validation — the template for how several broader platform arguments could unravel.

A subtle assumption embedded in many orexin valuation frameworks is that validation transfers across indications — that NT1 success de-risks NT2, which de-risks IH, which de-risks ADHD and fatigue, in sequence. The industry’s own development choices argue otherwise. Takeda’s response to an ambiguous NT2 result was not to push oveporexton harder, but to advance a structurally distinct molecule, TAK-360. Alkermes is pursuing ADHD and fatigue through separate assets — ALKS-7290 and ALKS-4510 — alongside alixorexton’s NT1/NT2/IH program, on a working assumption that these were purpose-built rather than late substitutions. Each indication’s evidence currently rests on its own molecule, dose range, and trial — not a shared platform read-through.

Lilly’s acquisition of Centessa adds an unexpected wrinkle. SEC filings show Lilly’s interest in Nov 2025 was initially directed at Centessa’s non-ORX750 assets — the follow-on OX2R agonists ORX142/ORX489 and the broader discovery platform — not the lead NT1/NT2/IH program. Centessa declined to sell those assets separately, citing its strategy as a focused orexin neuroscience company. Other potential acquirers, meanwhile, were reportedly interested in ORX750 alone or wanted more Ph2 data first. The only buyer willing to acquire the entire company was the buyer that had initially expressed interest in the non-ORX750 assets — Lilly’s resolution was to buy all of Centessa, ORX750 included, with CVR terms broadened to cover products containing either ORX750 or ORX142.

Lilly’s initial interest was in Centessa’s non-ORX750 assets. The rest of the market appeared to be evaluating a narcolepsy drug; Lilly was evaluating an orexin platform.

NT1 is de-risked. NT2/IH is partially de-risked. ADHD — currently the largest single component of platform optionality — is barely de-risked at all. The first phase proved replacing a missing signal restores function. The second phase tests whether orexin deficiency is a disease driver, a biomarker, or a bystander across broader CNS. The answer to the first does not predict the answer to the second.

V. The Competitive Clock

Here is the tension the orderly competitive summaries miss: Takeda wins the mechanism validation race on/before Sep 30, 2026, and enters commercial launch with an important caveat. Takeda is not a sleep medicine novice — Rozerem (ramelteon) has been on the US market since 2005, and existing specialist relationships exist. But Rozerem’s commercial trajectory is instructive: projected at $700M+ peak global sales, it peaked at ~$350M. Takeda has never commercialised a narcolepsy therapy, never navigated the oxybate-era prescriber hierarchy, and enters a market where Alkermes, Jazz, and Harmony have been actively detailing for years. The specialist relationships from an insomnia drug and the narcolepsy treatment network are not the same commercial asset.

Takeda’s position: two clean Ph3 NT1 studies, Priority Review, BTD, and a product profile — once-daily oral, no REMS, no black box — that removes the primary adherence barriers of the oxybate era. Building from zero: a narcolepsy sales force, payer access agreements, and patient identification infrastructure. The warehoused cohort — 55-60K patients on PCP-managed generic methylphenidate — is not visible to a specialist sales force. Reaching them requires disease awareness infrastructure that extends into primary care. The product can win on merit. The question is execution speed. One structural caveat independent of commercial readiness: FDA approval triggers a mandatory DEA scheduling review — orexin agonists are expected to land at Schedule IV — adding ~3 months before commercial dispensing begins. Launch economics in 2026 will be limited regardless of PDUFA outcome.

Alkermes enters Ph3 with BTD for NT1 and a Ph2 dataset — Vibrance-1, 92 patients, six weeks, three dose arms — directly competitive with Takeda’s efficacy benchmark. At 6 mg and 8 mg, 75–80% of patients achieved normative wakefulness on MWT; majority of 8 mg patients exceeded 30 min; ESS normalised across all doses. Cataplexy data was messier — only 6 mg reached statistical significance on a noisy patient-reported endpoint. Vibrance-1 showed PROMIS-Fatigue normalising by Wk2 (placebo-adjusted improvements of -8.7 to -12.9 points) and BC-CCI cognitive complaint scores improving at p<0.0001. Alkermes is pitching alixorexton as a broader disease burden agent, not merely a wakefulness drug. The complication for that thesis is that Takeda’s Ph3 package already demonstrates exactly that: PVT normalising attention in 73% of patients vs. 28% placebo; NSS-CT symptom burden dropping 18-21 points vs. 4 on placebo; SF-36 MCS improving +6.8-10.1 points placebo-adjusted; EQ-5D VAS improving +14.7-20.2 points — all pre-specified, all replicated across two Ph3 studies. The ALKS differentiation argument has therefore narrowed to a specific question: can alixorexton demonstrate incremental fatigue benefit beyond the broad functional restoration oveporexton has already shown? PROMIS-Fatigue and SF-36 MCS measure adjacent but distinct constructs — fatigue-specific vs. broader mental QoL — and that gap is where Alkermes is planting its flag. Whether it holds in Ph3 is unresolved. What is no longer arguable is that Takeda ignored these domains.

The commercial adjacency argument is harder to dismiss. The Avadel acquisition (Feb 2026) added Lumryz — $72M Q1 2026, $350–370M full-year guidance, ~4,500–5,000 active patients — to a portfolio that now includes active payer contracts in narcolepsy, a functioning REMS infrastructure, and medical affairs teams already calling on every high-volume sleep specialist in the country. The Lumryz prescriber base is a warm call list for ALKS 2680. The BRILLIANCE-NT1 Ph3 protocol (ClinicalTrials.gov, June 2026) anchors inclusion on ICSD-3-TR confirmation via PSG/MSLT or CSF hypocretin-1 — deliberately engineering around the 30–50% MSLT reclassification noise. Takeda launches first into a market Alkermes is already operating in. The patient cycling map that Takeda needs to build, Alkermes already has.

Lilly/Centessa is the capital certainty play. ORX750 has the cleanest Ph1 safety read in the class — no hepatotoxicity, no CV signal, no visual disturbances. Lilly paid $6.3bn upfront for an asset in adaptive Ph2a — since expanded to 248 patients from 96 at deal close, a capital commitment beyond the acquisition price itself. That figure is the market’s most precise revealed preference for what Lilly believes the NT2/IH amplification hypothesis could be worth. Whether sleep medicine benefits from Lilly’s GLP-1-scale infrastructure is debatable for NT1 alone — a ~22–25K patient market Jazz managed with a targeted specialty force. For the NT2/IH expansion, where the challenge is identifying and converting a large, diagnostically fluid, stimulant-managed population never actively targeted by premium therapy, the answer is probably yes.

Eisai’s E2086 has demonstrated proof-of-mechanism, while Merck (MK-6552) and Vertex (VX-433) have entered early clinical development. Their immediate competitive relevance is limited; their strategic significance is that orexin has become a mechanism large-cap CNS players now view as worth pursuing.

Harmony may ultimately benefit from orexin class validation, but it also inherits the burden of comparison — and that bar is now published: 63% MWT normalization, ~85% ESS normalization, 79-89% cataplexy reduction across two independent Ph3 studies. By the time BP1.15205 reaches meaningful efficacy testing, Takeda and likely Alkermes will have years of prescribing data embedded. The question for future entrants is no longer whether orexin works — it’s whether their asset can meaningfully improve on what’s already been shown.

The first phase of orexin development was proving that replacing a missing wakefulness signal could restore function. That question gets answered on Sep 30, 2026. The second phase — testing whether orexin deficiency is a disease driver, a biomarker, or a bystander across broader CNS disorders — will take the rest of the decade to resolve. Investors pricing the full platform today are running well ahead of the data.

The mistake investors risk making is treating validation of orexin replacement as validation of orexin expansion. The former appears increasingly likely. The latter remains largely unproven.

Disclaimer: Clinaptis Advisors publishes independent institutional research. This note is for informational purposes only and does not constitute investment advice. All data sourced from public filings, conference presentations, and peer-reviewed literature. Key sources: Shinozawa et al., Toxicological Sciences (2025); Lai et al., Psychoneuroendocrinology (2024); Bayirli et al., PMC (2024); Takeda FirstLight/RadiantLight Ph3 topline press release (July 2025); Takeda FDA NDA acceptance press release (February 2026); Jazz Pharmaceuticals Q1 2026 earnings; Alkermes Q1 2026 earnings.