Retatrutide’s 28%: The PCSK9 Mistake

Why Superior Efficacy Doesn't Always Win the Market

Eli Lilly’s retatrutide just delivered 28% weight loss in Ph 3 — approaching bariatric surgery outcomes and setting a new efficacy ceiling for the obesity class. Social media celebrated. LLY stock held its gains. The narrative wrote itself: the obesity race has a new leader.

We’ve seen this movie before. In 2015, Amgen’s Repatha and Regeneron’s Praluent (PCSK9s) delivered 60% LDL reduction — a genuinely spectacular cardiovascular efficacy number that dwarfed anything generic statins could achieve. The commercial result: near-zero adoption for four years, a 60% price cut, and one of the most painful launches in modern pharma history. Superior efficacy at a price point payers won’t cover, and PCPs won’t fight for is commercially worthless — regardless of how impressive the clinical data looks on a KM curve. The obesity market may be about to make the exact same mistake. This is a commercial architecture note, not a molecule ranking. The question isn’t which drug wins — it’s how the obesity market structure is changing around them.

Section 1 — The Bifurcation

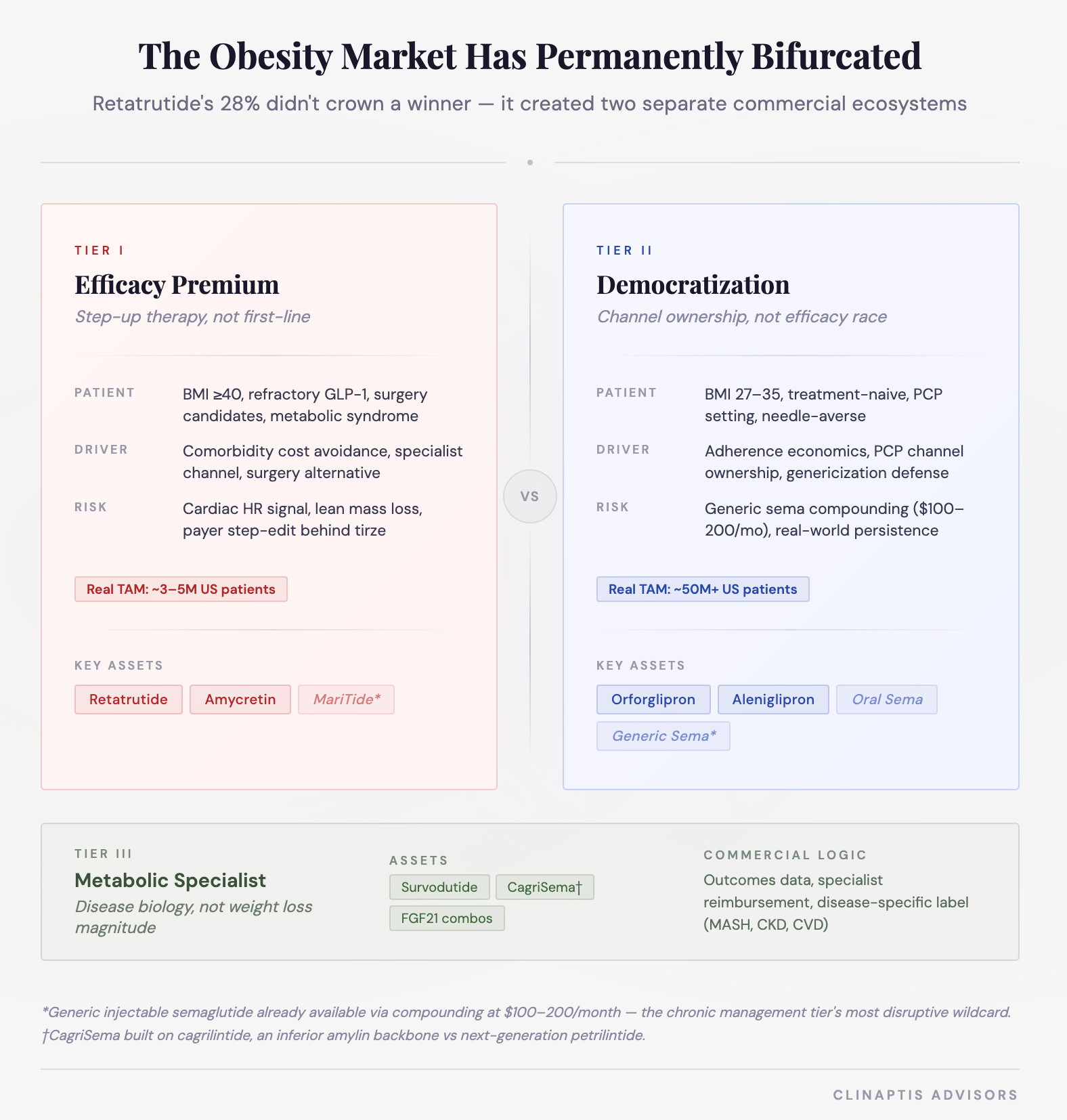

Retatrutide didn’t just raise the efficacy ceiling. It permanently split the obesity market into two distinct commercial ecosystems that require completely different investment frameworks — and most investors are still modeling it as one.

Retatrutide and orforglipron will rarely appear on the same prescription pad. They serve different patients, different physicians, different commercial channels, and different payer dynamics. Modeling them as head-to-head competition misses the structural point entirely.

Where Does Retatrutide Actually Belong?

The clinical trial population answers the commercial question better than Street’s launch forecasts. Retatrutide’s Ph3 enrolled patients with mean BMI approximately 37-40 — well above the moderate obesity population that orforglipron and oral sema are targeting. The trial was designed around severe obesity with metabolic comorbidities — not the 50M Americans with BMI 27-32 sitting in primary care waiting rooms.

This points to three specific patient entry scenarios where retatrutide makes clinical and commercial sense:

High BMI + metabolic syndrome. BMI >37-40 with concurrent T2D, hypertension, dyslipidemia, or cardiovascular risk. Comorbidity burden is high enough that incremental efficacy genuinely changes outcomes — and payer justification is strongest where comorbidity cost avoidance is demonstrable.

Prior GLP-1/GIP non-responders or partial responders. Approximately 10–15% of patients on semaglutide achieve <10% weight loss — a meaningful non-responder population. Escalating to triple-mechanism agonism represents a legitimate clinical step-up rather than a first-line choice. This is retatrutide's clearest commercial entry point.

Bariatric surgery candidates. BMI >40 patients who qualify for surgery but prefer or cannot tolerate surgical management. The 28% weight loss number earns its place here without qualification — approaching surgical outcomes pharmacologically is genuinely practice-changing.

What this means commercially: Retatrutide may initially commercialize as a high-acuity escalation agent rather than a broad first-line therapy — a commercial reality that defines its peak sales ceiling, though outcomes data and pricing evolution could expand that aperture over time. The addressable population that fits all three criteria simultaneously is ~3-5M Americans — meaningful, but a fraction of the 100M+ obesity-eligible population the market is sometimes implicitly pricing.

This patient profile is not an accident — it’s exactly who the Phase 3 was designed around. The trial population is the commercial roadmap.

Section 2 — Mechanism, Tolerability, and the Real-World Efficacy Gap

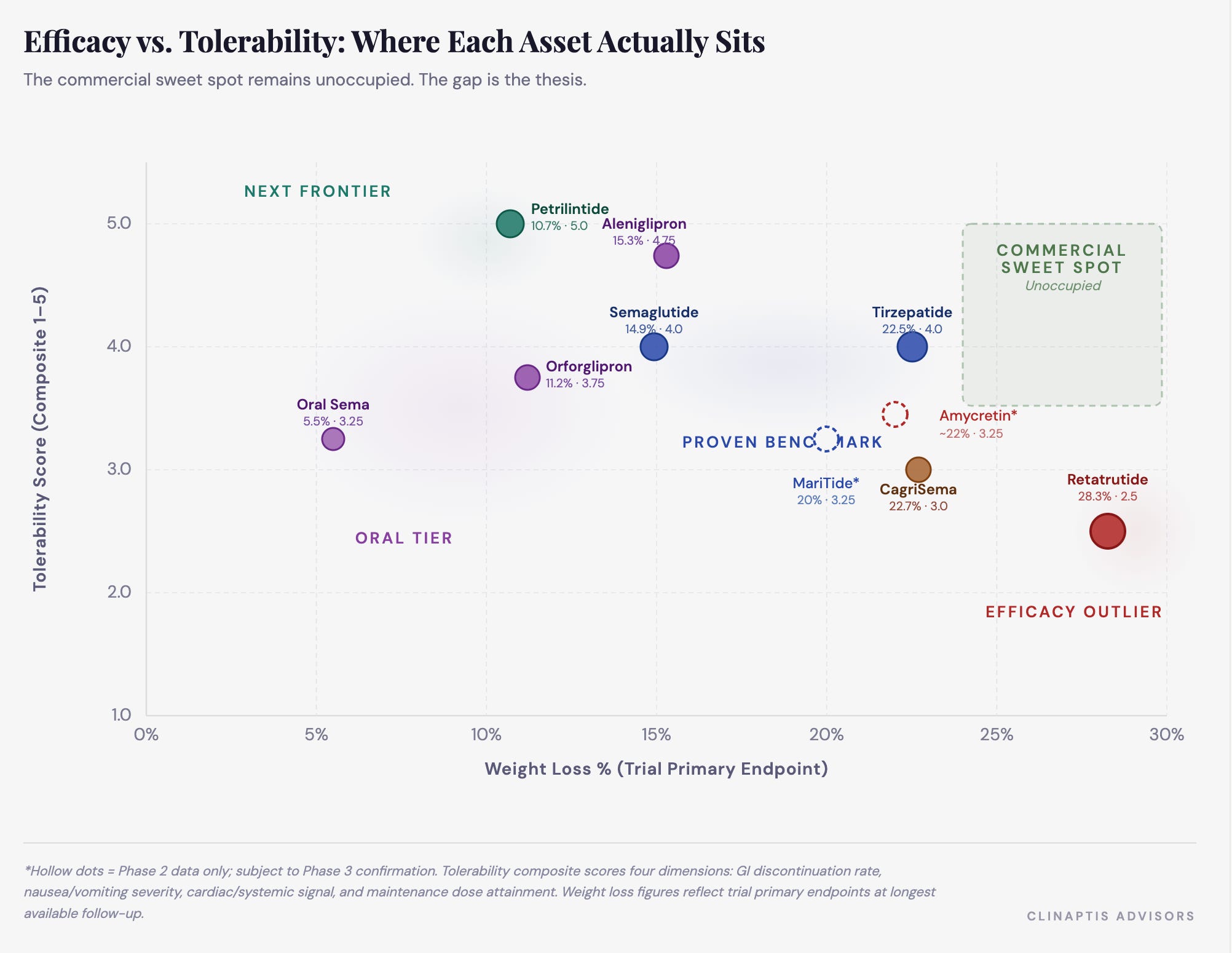

Why Triple Agonism? The Architecture Behind 28%

Retatrutide represents Lilly’s bet that obesity pharmacotherapy has moved beyond appetite suppression toward systemic metabolic reprogramming — and that understanding the architecture explains both the efficacy ceiling it reached and the tolerability ceiling it may have hit simultaneously.

Three design choices define it:

Glucagon escapes the satiety ceiling. GLP-1 and GIP suppress appetite effectively — but metabolic adaptation limits how far pure satiety signaling can go. Glucagon adds lipolysis, hepatic fat clearance, and energy expenditure as parallel levers. That’s the mechanistic argument for why 28% is achievable where 22% was the prior ceiling.

Receptor balance was deliberately engineered — strongest at GIP, intermediate at GLP-1, weakest at glucagon — to harness glucagon’s benefits while limiting its tolerability burden. The extensive dose-escalation schemes across Phase 1 and 2 weren’t inefficiency. They were Lilly asking whether triple agonism at scale remains commercially viable — a question the real-world launch will now answer.

The development program was built beyond obesity. Liver fat reduction, diabetic kidney disease, cardiovascular outcomes, sleep apnea, osteoarthritis — deliberate platform positioning. Retatrutide’s peak sales ceiling may depend less on obesity label breadth and more on whether a cardiovascular outcomes trial justifies premium pricing to payers who currently see 28% as impressive but not obviously reimbursable above tirzepatide’s 22%.

The debate is not whether retatrutide works. It does. The debate is whether “metabolic reprogramming” at this tolerability cost and price point reaches enough patients to justify the commercial expectations embedded in LLY’s current valuation — or whether we’re watching the PCSK9 mistake in slow motion.

The Mechanism Landscape — Where Each Approach Stands

Not all mechanisms are equal and most aren’t ready:

GLP-1 — Satiety, gastric emptying, insulin secretion. Fully validated. Now commoditizing.

GIP — Counterintuitively improves GLP-1 tolerability rather than worsening it. Tirzepatide’s key insight. Validated commercially.

Glucagon — Energy expenditure, thermogenesis, hepatic fat clearance. Adds efficacy and cardiac and GI burden simultaneously. Jury still out on the commercial tolerability ceiling.

FGF21 — Hepatic fat reduction, metabolic regulation. Its home is MASH and fibrosis, not primary care.

Amylin — Parallel receptor system, not additive to GLP-1 on tolerability. CNS-mediated satiety. Lean mass preservation signal. Only MOA that potentially solves the efficacy/tolerability tension rather than worsening it.

Adherence at month 12 beats peak weight loss at week 72 in any chronic disease market. The D/C data makes this concrete: retatrutide’s discontinuation rate reaches 11.3% at the highest efficacy dose vs 4.1% at the lowest and 4.9% for placebo. The cardiovascular signal compounds it — mean heart rate increased +3.6 bpm at 4mg, +5.6 bpm at 8mg, and +6.7 bpm at 12mg (95% CI: 4.6–8.8 bpm). An upper CI of +8.8 bpm in a population where atrial fibrillation prevalence already runs 3–5x the general population is not necessarily prohibitive — but glucagon-mediated efficacy amplification may carry a chronic cardiovascular cost that becomes commercially relevant at scale.

The commercial trade-off in one number: retatrutide delivers 5.5% more weight loss than tirzepatide at the cost of 4.3% more discontinuation. That ratio is the commercial conversation.

MariTide (AMGN) — A Different Bet

MariTide combines GLP-1 agonism with GIPR antagonism in a monthly injectable — producing ~20% weight loss at 52 weeks with one genuinely interesting signal: patients maintained weight loss for up to 150 days post-dose. Phase 3 will determine if that durability holds at scale. If it does, monthly dosing plus off-drug persistence becomes a credible commercial answer to the adherence problem retatrutide just made worse.

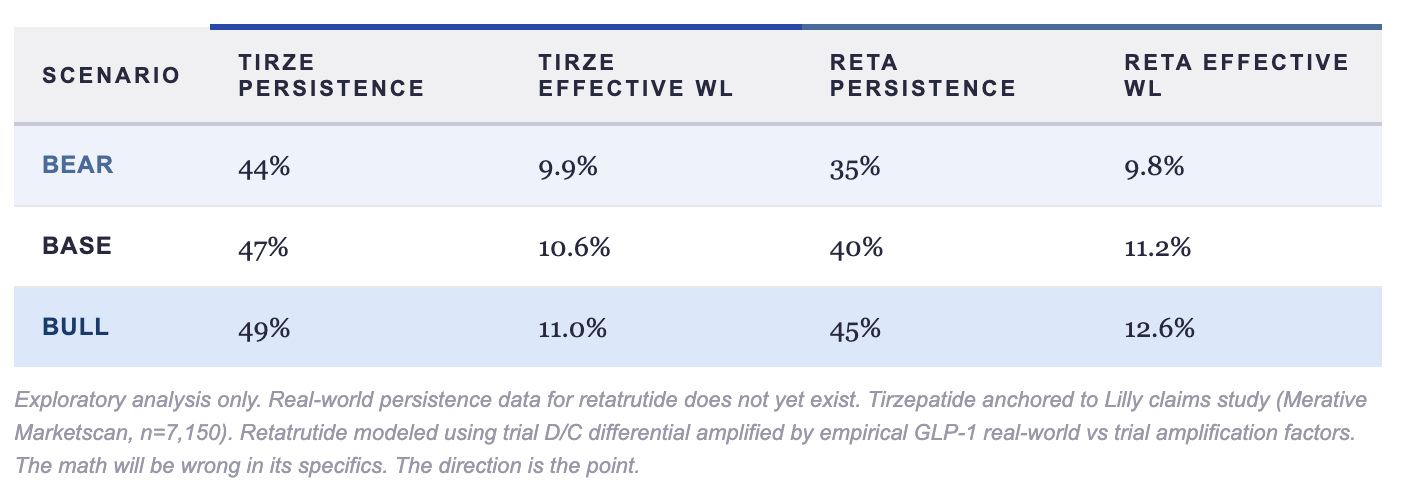

The Real-World Gap — An Exploratory Framework

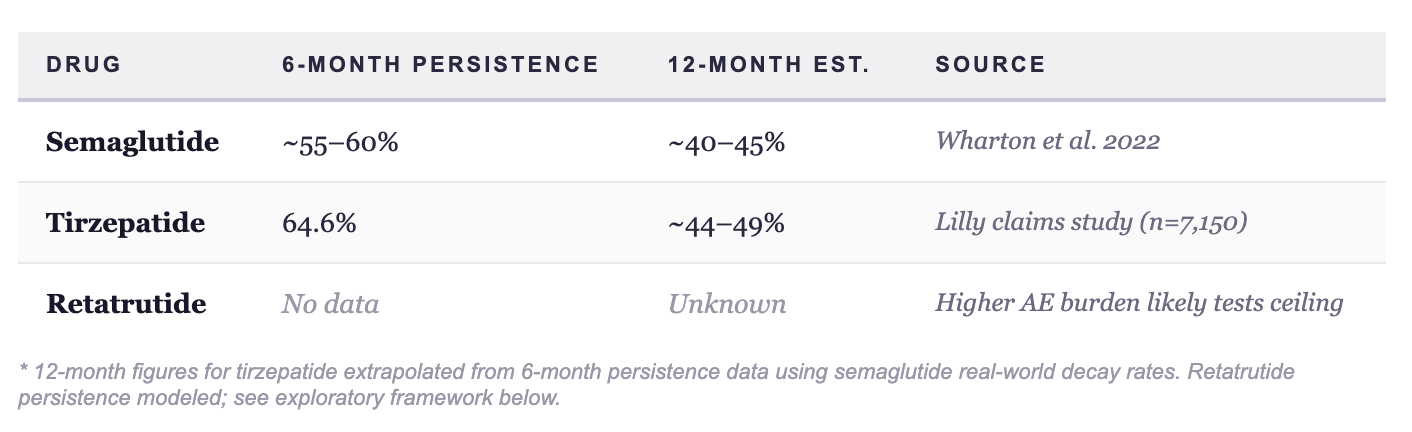

Explicitly exploratory. Tirzepatide anchored to a published Lilly claims study (Merative Marketscan, n=7,150). Retatrutide modeled using the trial D/C differential. The math will be wrong in its specifics. The direction is the point.

Tirzepatide’s 64.6% six-month persistence extrapolates to 44-49% at 12 months applying semaglutide real-world decay rates. Retatrutide’s higher trial D/C rate — amplified by the 3.5-4x real-world vs trial gap established across the GLP-1 class — produces a 12-month persistence range of 35-45%.

Retatrutide’s 5.5% trial efficacy advantage disappears in bear and base scenarios — and amounts to 1.6% points in the bull case, which requires assuming real-world tolerability materially better than the trial AE profile suggests. The real-world obesity battle is fought on adherence economics. The gap narrows. In two of three scenarios — it disappears.

Three important caveats. First, trial D/C rates capture only one driver of real-world attrition — access barriers, affordability, titration fatigue, and simple goal achievement matter as much or more in obesity. Second, the amplification factor may understate retatrutide’s persistence: higher efficacy creates behavioral reinforcement. A patient losing 28% tolerates more nausea than one losing 20%. The feedback loop of visible body changes, comorbidity reversal, and social reinforcement may flatten retatrutide’s persistence curve in ways this model doesn’t capture. Third, the effective WL calculation treats discontinuation as zero efficacy thereafter — which overstates the penalty, since patients retain meaningful weight loss for months after stopping. The real unresolved question isn’t whether the gap narrows. It’s whether retatrutide’s ultra-high efficacy compresses time-to-target enough that some patients discontinue intentionally — and still derive durable metabolic benefit. If that hypothesis holds, traditional chronic-medication persistence models may not apply to this asset class at all.

Full TRIUMPH dataset reads at ADA. The persistence curve and cardiovascular signal at longer follow-up will be the numbers that matter — and will determine whether this framework needs revision or reinforcement.

Section 3: The Democratization Tier — Oral GLP-1s and the Access Imperative

The oral GLP-1 story didn’t start with orforglipron. It started with a graveyard.

Pfizer’s danuglipron and lotiglipron — both discontinued due to liver toxicity. Rybelsus — not a true small molecule, hamstrung by poor bioavailability and a T2D-only label. The class carried genuine trauma into 2026. Every new entrant had to answer one question before efficacy even mattered: is this safe enough to not embarrass us?

Orforglipron answered yes. And then delivered. Approved in April ‘26 as Foundayo — it becomes LLY's primary care anchor.

Orforglipron (LLY) — Good Enough Is the Point

ATTAIN-1 Ph3: 11.2% absolute WL at 72 weeks, placebo-adjusted 9.0%. Missingness in active arms of 14-16% — better than placebo’s 23.9%, a quietly encouraging persistence signal. The drug works. It is not tirzepatide. It was never meant to be.

The commercial thesis is not efficacy. It is three things:

Channel ownership. A daily pill requires no cold chain, no injection training, no specialist referral. The prescriber base expands from ~15,000 obesity-adjacent physicians to every PCP in America. That distribution shift is worth more commercially than an extra 3% weight loss.

Genericization defense. Semaglutide biosimilars arrive 2031-2032. Compounding versions exist today at $100-200/month vs $1,000+ branded. Every week without established oral GLP-1 prescriber habit and formulary position is a week NVO’s generic injectable erodes the chronic management tier. Orforglipron’s launch isn’t about 2026 revenue. It’s about 2032 defensibility.

TAM expansion. The patients who take orforglipron are not patients who were about to start tirzepatide. They are the 30-40M Americans who wanted pharmacological obesity treatment and couldn’t or wouldn’t inject weekly. New patients. New revenue. Not cannibalization.

LLY isn’t launching orforglipron to win the efficacy race — they’re launching it to own the primary care channel before generic semaglutide arrives and makes the entire injectable market a commodity. That’s a very different and much smarter strategic bet than it looks.

GPCR/Aleniglipron — The Better Molecule Playing The Long Game

Aleniglipron is doing something strategically underappreciated: building the best oral GLP-1 molecule while letting orforglipron commercially derisk the market it plans to enter.

The efficacy case is legitimately strong:

ACCESS Phase 2a (120mg): 11.3% placebo-adjusted WL at 36 weeks

ACCESS II (240mg): 15.3% placebo-adjusted at 36 weeks — no plateau observed

No-plateau at 36-44 weeks typically signals further upside at 52 weeks. Injectable-like efficacy from an oral small molecule is not a phrase the market expected to use seriously in 2026.

The tolerability rescue is the program-defining moment: Early data showed 10.4% discontinuation — problematic for a chronic drug. GPCR’s fix: ultra-slow 2.5mg titration initiation. Result: zero AE-related discontinuations with the slow-start protocol. The broader obesity class keeps relearning the same lesson — titration strategy matters almost as much as molecule potency.

The safety profile directly addresses class trauma: No DILI, no persistent LFT elevation, no QTc signal. Given danuglipron and lotiglipron’s history, this isn’t boilerplate. It’s GPCR surgically removing the historical objection before it gets raised.

The strategic positioning is deliberately non-confrontational. GPCR isn’t trying to beat orforglipron in a head-to-head. By the time aleniglipron reaches market, orforglipron will have trained PCPs, negotiated formulary positions, and demonstrated oral GLP-1 commercial viability. GPCR inherits that infrastructure and competes with a better molecule. That’s not a second-mover disadvantage — it’s a deliberate fast-follower strategy in a market too large for one winner. The manufacturing advantage compounds this: oral small-molecule GLP-1s need no peptide synthesis, no cold chain, no autoinjectors — structural scalability that injectable franchises cannot replicate.

The hidden bull case: if aleniglipron truly solves chronic tolerability at 15%+ placebo-adjusted efficacy, oral convenience plus injectable-comparable efficacy becomes commercially explosive.

The most consequential amylin story of 2026 isn’t happening in oral formulations — it’s happening in the injectable combination space, where NVO’s cagrisema is about to face a reckoning from a molecule it was never designed to compete with.

The Amylin Debate: NVO Built the Wrong Molecule

CagriSema’s 22.7% WL in REDEFINE-1 looked like NVO’s answer to tirzepatide. It wasn’t. It was NVO’s answer to their own anxiety about losing ground — built on a molecule already being superseded while they were celebrating the press release.

The combination optionality question is where the thesis crystallizes. CagriSema is psychologically and commercially locked to one combination. Petrilintide + CT-388 (Roche’s GLP-1/GIPR asset) is the genuinely dangerous combination — potentially achieving 18-22% WL with materially better tolerability than any aggressive GLP-1/GIP or glucagon combination in development. Not because it beats retatrutide on peak efficacy. Because it may beat it on persistence, refill behavior, PCP adoption, and real-world durability — the metrics that determine lifetime commercial economics in a chronic disease market.

The obesity market is entering its second-order optimization era. First era: maximize weight loss, chase waterfall charts. Second era: persistence, tolerability architecture, combination flexibility, lean mass preservation. Petrilintide was engineered for Era 2. Cagrilintide still carries Era 1 DNA.

NVO built the right thesis — amylin combinations are the next commercial frontier — with the wrong molecule. Roche paid to fix that mistake. The market hasn’t fully priced the implications yet.

Conclusion: Retatrutide may ultimately become the most effective obesity drug ever developed. But the next phase of this market may not be decided by peak efficacy at all. The winners will be determined by persistence architecture, channel ownership, manufacturing scalability, and the ability to survive contact with real patients and real payers at global scale. The PCSK9 analogy isn’t a prediction. It’s a warning that the obesity market has heard before — and may be about to ignore again.

The next mechanism frontier — amylin done right — deserves its own note.

The obesity market just gave us its most impressive efficacy number. The next 18 months will tell us whether impressive efficacy and commercial success are the same thing — or whether we’re about to watch the PCSK9 mistake happen again, this time with 100 million patients in the balance.