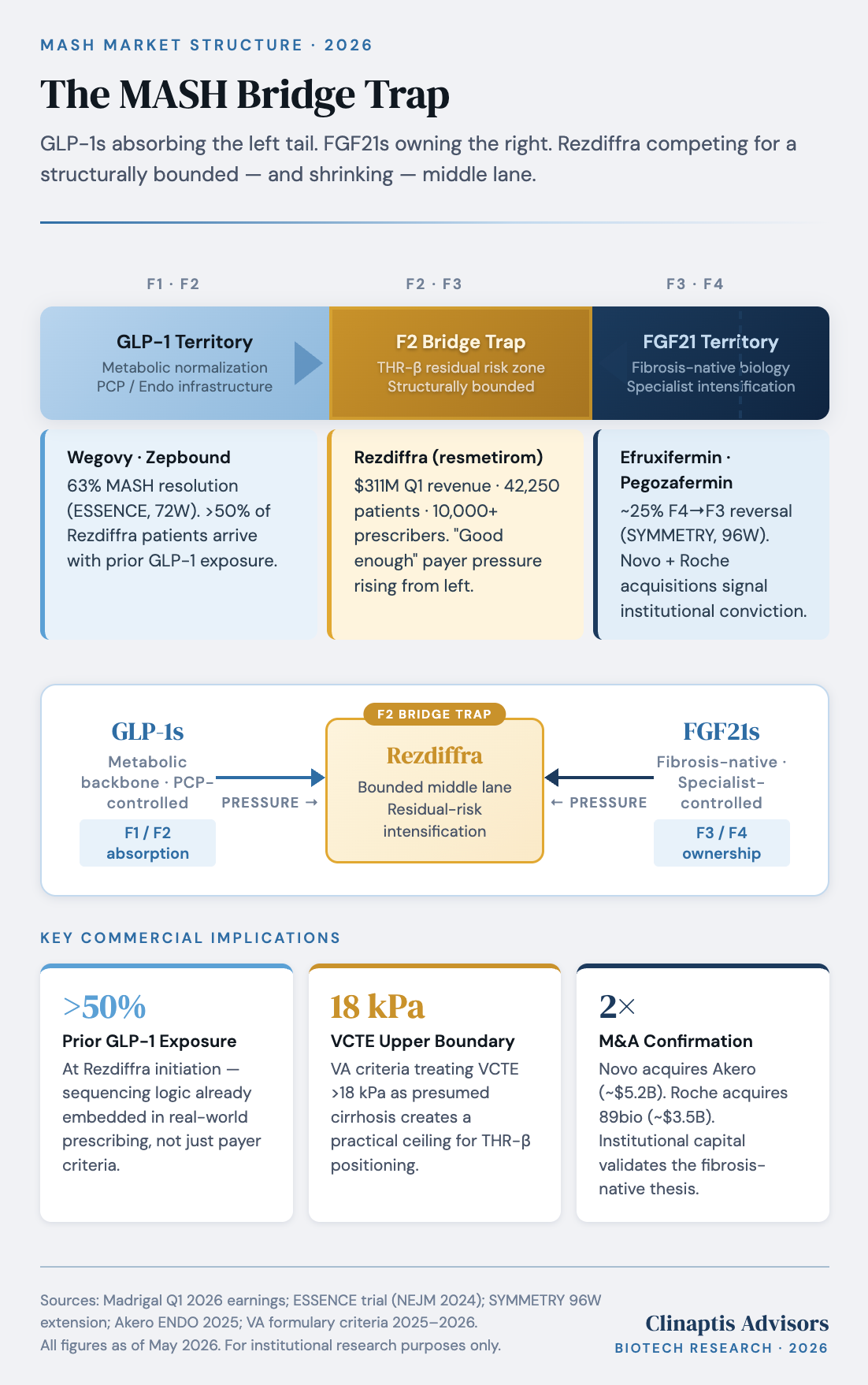

The MASH Bridge Trap

Why Madrigal's Rezdiffra Market Is Smaller Than the Model

GLP-1s Didn’t Just Enter the MASH Market. They Restructured It.

Between 2021 and 2023, every major pharma was racing to stake out MASH territory before anyone else got approved. First mover locks up the hepatologists, controls the patient funnel, owns the category. Plant your flag, defend your ground. The field was still debating whether 23% fibrosis improvement — Intercept’s best number from REGENERATE, the trial FDA ultimately rejected anyway — was enough to build a market around. Nobody modeled the ground moving. It moved.

Wegovy Didn’t Join the MASH Market. It Reclassified It.

Wegovy’s MASH approval in August 2025 was not a new entrant competing for patient share. It was a reclassification. ESSENCE posted 63% MASH resolution and 37% fibrosis improvement at 72 weeks — not by targeting the liver, but by fixing the metabolic substrate driving it. GLP-1s don’t treat MASH. They treat the condition that causes it.

The approval didn’t create the behavioral shift — it formalized one already three years in the making. Physicians had been watching hepatic fat improve on GLP-1s since 2021. The mechanism required no clinical trial to intuit. What August 2025 changed wasn’t prescribing. It was institutional infrastructure. Payers now have a labeled prior therapy to sequence against Rezdiffra — and they are using it.

The prescribing data confirms the split is already happening at ground level. Two quarters post-approval, Madrigal’s own disclosure confirmed more than 50% of active Rezdiffra patients had prior GLP-1 exposure. That’s not eight months of label-driven behavior change. That’s three years of clinical pattern recognition showing up in the access data. Meanwhile the prescriber base tells its own story — 10,000+ physicians, majority gastroenterology volume, and a nascent endocrinology channel Madrigal only began targeting in Q4 2025. Endocrinologists are at the earliest stage of a ramp gastroenterology took two and a half years to complete. They also manage the patients with the highest GLP-1 background rates in the system. That tension doesn’t resolve in Madrigal’s favor. Triangulated GLP-1 penetration across the broader diagnosed F2/F3 pool sits at approximately 38-42% — and the trajectory, as Zepbound pursues its own MASH indication and oral GLP-1s reduce prescribing friction further, is what the penetration models still haven’t priced.

What that trajectory created has a name. Call it the Bridge Trap.

The Bridge Trap: Rezdiffra’s Market Is Smaller Than the Model

The launch numbers are real. $321M in Q4 2025. 42,250 active patients. Best NBRx week in launch history — occurring after Wegovy’s MASH approval, not before it. Rezdiffra is executing. That is not the argument.

The argument is structural — and it starts with what Rezdiffra is already functioning as in practice: a second intervention, not a first. On the other end, Novo and Roche have placed $8.7B behind FGF21 biology — the mechanism with the strongest fibrosis-specific data in the field right now (efruxifermin: 39% fibrosis improvement in compensated cirrhosis at 96 weeks) and the clearest separation from THR-β at advanced disease stages. Rezdiffra sits between infrastructure scale it cannot match on the left and fibrosis-native differentiation it cannot replicate on the right.

That is the Bridge Trap. The bridge itself — F2/F3 patients with residual liver dysfunction despite GLP-1 optimization — is real. But its boundaries are being drawn by institutions Rezdiffra doesn’t control. On the left, VA criteria explicitly require GLP-1 optimization before Rezdiffra authorization; an estimated 40-70% of commercial plans are moving in the same direction. On the right, approximately 14-17% of the diagnosed F2/F3 pool — roughly 65,000-78,000 of the 460,000 addressable patients — exceed the 18 kPa VCTE threshold, placing them outside the THR-β window entirely. The bridge is not disappearing. It is shrinking from both ends simultaneously.

The strongest counterargument deserves a direct answer. Management cites expansion of the specialist-managed F2/F3 pool from approximately 315,000 to 460,000 patients as evidence the diagnosis funnel is growing faster than GLP-1s can absorb it. The skeptical read: those 145,000 patients were not hiding. They were obese, diabetic, and already inside healthcare systems that lacked both a therapy and an economic incentive to formally diagnose them. What changed was classification and referral infrastructure, not disease prevalence. Diagnosis growth expands the funnel. It does not automatically expand the bridge.

Why Novo Bought Akero: $8.7B Said What Management Won’t

Novo’s ~$5.2B acquisition of Akero was not a bullish bet on liver disease. Novo already owned the metabolic backbone. The deal acknowledged something harder — that GLP-1-driven metabolic repair may not fully resolve advanced fibrosis biology, and that the residual unmet need at the severe end belongs to a different mechanism entirely. Unlike THR-β, FGF21 retains activity deeper into the fibrosis continuum — where stellate activation and matrix remodeling operate independently of metabolic inputs.

FGF21 earned that capital allocation. The answer was never the efficacy headline — it was what happened after it. Efruxifermin’s SYMMETRY data showed deepening fibrosis response over 96 weeks, late converters emerging, and signal directionally preserved in patients already on background GLP-1 therapy. That last point matters: FGF21 and GLP-1 appear additive, not redundant. The combination effect is present, not absent. Roche reached the same conclusion from a different angle — paying ~$3.5B for pegozafermin, which hit both FDA-approvable histological endpoints in ENLIVEN with ~3.5x fibrosis improvement over placebo alongside broad cardiometabolic improvement. Neither transaction was acquiring broad metabolic MASH volume. Both were explicitly focused on residual fibrosis burden after metabolic optimization.

The capital allocation map now reads plainly. Novo owns the metabolic backbone and the fibrosis escalation layer. Roche owns the metabolic-heavy fibrosis segment. Lilly owns the top of the funnel. No major company with real MASH exposure is building toward monotherapy dominance. $8.7B concentrated at the severe end of the fibrosis spectrum is not a coincidence. It is a thesis — and it is the right wall of the Bridge Trap becoming permanent.

What the Market Is Missing

Given that map, the right question is no longer which therapy wins MASH. It is which mechanisms remain indispensable after metabolic optimization already occurs. Madrigal’s pipeline answers that more honestly than their communications do. The oral GLP-1, the PNPLA3 siRNA, the DGAT-2 inhibitor — none of these are TAM expansion plays. Combination optionality is being priced as additive to the Rezdiffra opportunity. The more precise read is compensatory — capital deployed to manage the consequences of a structurally eroding standalone position, not reverse them. The company is following the patient funnel upstream into territory GLP-1 manufacturers already own.

Rezdiffra will keep growing. FGF21s will become major franchises. None of that is the argument. The argument is that the economic center of gravity has permanently shifted toward residual-risk management — the patients metabolic optimization alone cannot resolve. Durable value accrues there. Not in defending broad monotherapy share against GLP-1 infrastructure that controls the funnel, owns the patient relationship, and is now backed by $8.7B of acquisition capital at the fibrosis-intensive end. The map most investors are using is a picture of a market that no longer exists.

Every major player has already repriced the thesis in their capital allocation. Novo paid $5.2B. Roche paid $3.5B. The sell-side consensus on MDGL hasn’t moved. The land-grab thesis is dead. The map most investors are using is a picture of a market that no longer exists. The price tag on that picture is next.

The Math the Consensus Hasn’t Done

MDGL trades at ~$11B+ on $1.13B trailing revenue. ~9.7x sales, pre-profitability, consensus-long, with sell-side peak Rezdiffra sales modeled at ~$7.1B by 2035. That number is not a forecast. It is a wish.

The $7.1B requires 30-35% penetration of the addressable MASH market on standalone monotherapy. Run the haircut. Start with 460,000 diagnosed F2/F3 patients. Remove the 14-17% above the VCTE ceiling — already outside the THR-β window. Remove the growing share achieving adequate metabolic response on GLP-1 backbone before specialist intervention occurs — a denominator expanding as the 38-42% background GLP-1 rate deepens. What remains is the Bridge Trap population. Real, bounded, and structurally smaller than the model assumes. A 30% penetration of a narrowing middle lane is not the same calculation as thirty percent penetration of a standalone hepatology market. The NPV difference is not marginal. It is the entire bull case.

One assumption the consensus embeds deserves a direct answer: endocrinology as additive TAM. It isn’t. Every endocrinologist Madrigal converts manages patients with the highest GLP-1 background rates in the system and faces structurally higher authorization friction — not lower. The consensus is modeling the endocrinology ramp as if the channel behaves like hepatology did in 2024. It won’t.

Then there is 2027. MAESTRO F4C reads next year. F4C probably works. The opportunity is probably real — ~245,000 patients, no approved therapy, genuine urgency. The street is pricing it as a straightforward doubling of TAM. Here is what that misses: a positive readout doesn’t validate penetration assumptions. It forces them into the open for the first time. How many F4C patients are already on optimized GLP-1 therapy? How many sit above the VCTE threshold — FGF21 candidates, not THR-β candidates? The 2027 readout is not a binary catalyst. It is a forced reckoning with penetration math that current valuation has never had to confront — even in the scenario where Madrigal wins cleanly.

Madrigal is well-run. Rezdiffra is genuinely important. None of that is the issue. The issue is $12B priced on a market structure that no longer exists, defended by a consensus that has never run the haircut this note just did. 2027 is when that becomes unavoidable. The sell-side hasn’t buried the land-grab thesis yet. The math already has.

Disclaimer

This note is published by Clinaptis for informational and educational purposes only. Nothing herein constitutes investment advice or a recommendation to buy or sell any security. Clinaptis is not a registered investment advisor or licensed financial professional.

All data and market figures referenced are sourced from publicly available information including company filings, earnings transcripts, clinical trial publications, and regulatory disclosures. Where figures are triangulated or estimated, this is noted explicitly in the text.

References to market valuation and consensus estimates are analytical tools used to illustrate structural arguments — not calls to action on any specific security. Directional commentary reflects the author’s interpretation of public information, not a recommendation to establish any investment position.

Readers should conduct their own independent research and consult a licensed financial advisor before making any investment decision.

Clinaptis publishes independent market structure commentary on pharmaceutical and biotech categories. All views are the author’s own.