The Rise of Mini-Pharma: Why Commercial Concentration Is Replacing Platform Breadth

Concentration, commercial proof, and the rise of biotech’s new operating model.

1. The Market Quietly Changed What It Rewards

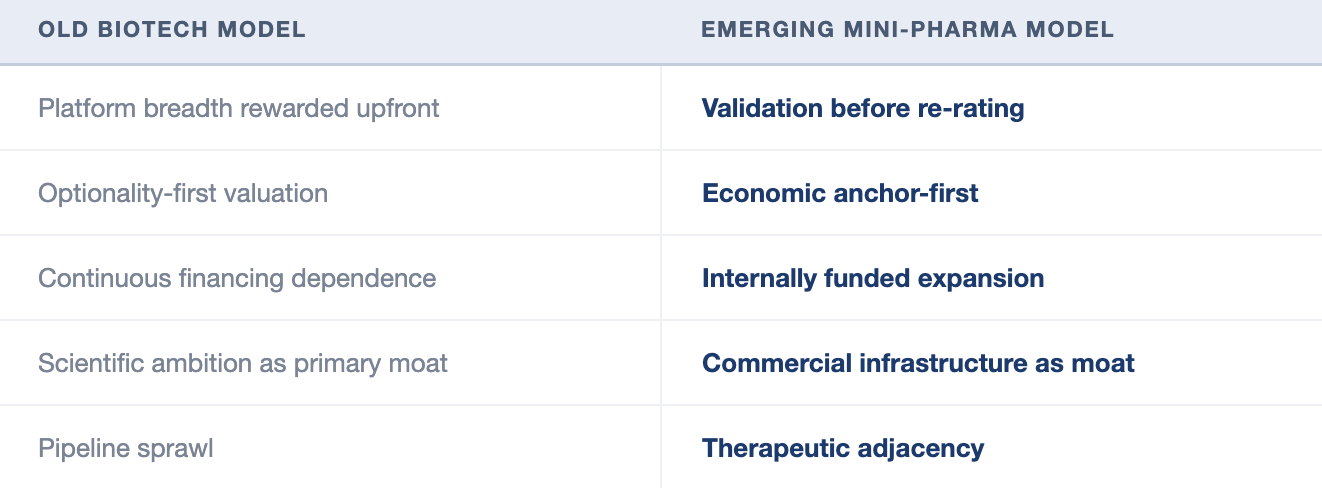

From Platform Maximalism to Operational Concentration

Between 2018 and 2021, the dominant valuation framework rewarded scientific ambition over commercial execution. The XBI peaked above $180 in early 2021, carrying an entire cohort of platform-stage companies valued on pipeline optionality, modality novelty, and TAM expansion narratives rather than observable commercial output. The implicit contract was straightforward: pursue the largest possible scientific surface area, and the market will assign credit for the universe of drugs you might eventually build.

Pre-revenue companies routinely carried market capitalizations of $2B–$5B on preclinical data packages alone. Nektar briefly touched $15B on an IL-2 cytokine platform. Allogene peaked at ~$4.7B before a single patient had been durably cured. The gene-editing basket — EDIT, NTLA, BEAM — collectively represented north of $22B built almost entirely on scientific optionality.

The cost of being wrong was low when dilution was cheap and equity markets were perpetually open.

Post-2021 ended that contract abruptly. Rates rose, the financing window narrowed, and the market began demanding proof rather than possibility. The XBI fell more than 60% from peak to trough. The rest is consequence.

The reset did more than destroy speculative valuations. It revealed which businesses could fund growth without capital markets.

The Forced Experiment

What followed was less a correction than an involuntary stress test. When capital became expensive, two very different sets of businesses became visible simultaneously. The casualties were not random — they represented two distinct failure modes that should not be conflated:

precision-oncology enthusiasm

Nektar Therapeutics

Cytokine / IL-2

~- 87%

~$15B

Speculative IO optionality

Platform

without durable product

economics

Allogene Therapeutics

Allogeneic Cell

~- 91%

~$4.7B

Manufacturing complexity +

Therapy

durability skepticism

Gene Editing Basket

Genome Editing

-42% to

~$22B

Valuation timing, not scientific

EDIT . NTLA . BEAM

-95%*

combined

validity

* Gene editing range: EDIT -95%, NTLA -83%, BEAM -42% on market-cap basis, Dec 2020 to Jun 2026. BEAM's narrower market-cap

decline reflects share count roughly doubling since 2021 - a 2021 holder of 1% of BEAM now owns ~0.49% of the business. Returns reflect

price performance only; ownership dilution compounds the loss.")

IOVA is a different failure mode — not financing or durability risk, but throughput. Amtagvi scaled toward $350–370M FY26 guided revenue on genuine commercial reception, but iCTC turnaround only reached ~32 days in 2026, years post-launch. Commercial proof alone didn’t re-rate the stock; the infrastructure had to catch up to it.

IONS and PTCT run on non-dilutive, royalty-heavy financing — on paper, internally funded. Neither re-rated like NBIX or KRYS. The reason: neither owns the specialist relationship — IONS licenses out its ASO franchise to Biogen and AstraZeneca, PTCT’s salesforce sits on capped ultra-rare assets plus Sarepta royalty pass-through. Financing source isn’t the variable. Owned infrastructure is.

$40B in Pre-Commercial Optionality, Repriced. At peak, these four categories collectively represented well north of $40B built substantially on pre-commercial optionality. The gene-editing row deserves particular care: the science remains credible and the programs continue. What the market repriced was when that science deserved premium valuation — not whether it deserved it at all. The wide range inside that basket — EDIT down ~95%, BEAM down only ~42% on a market-cap basis — isn’t inconsistency in the data. The more instructive lens is ownership retention. Between FY20 and 2026, BEAM, NTLA, and EDIT increased shares outstanding by roughly 56% to 128% while their market capitalizations declined 62% to 95% from peak.

Valuation compression was the primary destroyer — but financing dependence compounded it by transferring future ownership to the investors who funded the intervening years. A holder of 1% of BEAM, NTLA, or EDIT at the start of the platform cycle now owns approximately 0.49%, 0.44%, and 0.64% of those businesses respectively. The stock went down and the stake got diluted simultaneously. That is what continuous external financing dependence actually costs — not just in the reset, but in any eventual recovery.

CRSP is instructive: Casgevy generated only ~$116M in FY2025 despite Vertex’s full rare disease infrastructure — approved, resourced, and still commercially constrained by one-time dosing economics. uniQure’s Hemgenix makes the same point from a different angle: approved in 2022, licensed to CSL Behring rather than commercialized directly, with QURE collecting milestones while CSL owns the hematologist relationship.

Meanwhile, the businesses that had built concentrated commercial infrastructure compounded quietly. Neurocrine grew from ~$1.1B in 2020 revenue to ~$2.8B in 2025, funding its pipeline internally. Corcept scaled from ~$270M to ~$760M at 95%+ gross margins with zero dilutive financing and never more than ~150 commercial representatives. Krystal went from pre-revenue to $389M in annual sales at 93%–95% gross margins within three years of launch — generating positive net income and ~$1B in cash without a single dilutive raise after commercialization.

The divergence was not random. The survivors shared concentrated franchises, specialist prescriber ecosystems, and R&D funded from operations rather than capital markets — running R&D at 20%–35% of revenue while the casualties ran at 300%–500%+.

The regime shift can be stated plainly: the market stopped paying premium multiples for the possibility of breadth and began paying for the proof of concentration — with ultra-rare Ph2 data the standing exception, where regulatory probability of success substitutes for commercial proof. That single observation has significant implications for which businesses the next decade of biotech rewards — and which it quietly leaves behind.

Platforms Didn’t Die. The Valuation Framework Did.

This is worth stating explicitly because it’s the objection most readers form before finishing Section 1. CRSP’s Casgevy is a genuine scientific achievement. MRNA may yet build a durable mRNA franchise beyond COVID. RXRX’s EC-4881 is the first sign that AI-discovered assets can reach registrational trials. The science didn’t stop working. What changed was when it deserved premium valuation — not whether it did.

The market’s message since 2021 has been precise: optionality is real but it should be priced after clinical and commercial validation, not before it. A platform that hasn’t demonstrated reimbursable, repeatable revenue doesn’t get a $5B market cap on the promise that it might. It gets one after it proves it can. That’s not anti-science. It’s a repricing of the timeline at which science converts into shareholder value. The casualties above weren’t punished for being wrong. They were punished for being early and expensive simultaneously.

NBIX

+65%

100

BEAM -58%

NTLA -71%

0

NKTR -76%

2021

2022

2023

2024

2025

2026

ALLO -92%

EDIT -96%

Source: Company price data, Clinaptis Advisors. Indexed to Dec 31 2020 = 100. Platform basket: ALLO, BEAM, EDIT, NKTR, NTLA. Concentrated compounders: COGT,

CORT, KRYS, NBIX. Returns reflect price appreciation only, not total shareholder return inclusive of any distributions.

CLINAPTIS ADVISORS")

2. The Rise of Mini-Pharma

Focused Specialist Businesses Are Emerging As the New Winning Model

Out of the post-2021 reset, a new archetype is consolidating. These businesses are neither single-asset biotech stories nor sprawling platform organizations. They operate as concentrated specialty-commercial ecosystems with unusually scalable economics — and the pattern is now quantitatively observable in a way that is difficult to dismiss as narrative.

The numbers tell the story directly:

H

EES

EMPLOYEE

FORCE

REP

MARGIN

ECOSYSTEM

NBIX

3,102

~22%

2,300

$1.35M

600 **

$5.2M

98%

Neurology

KRYS

417

~34%

314

$1.33M

40

$10.4M

93%

Rare Derm

CORT

769

~13%

552

$1.39M

~150

$5.1M

98%

Endocrine / Onc.

Platform

Basket*

~65

Volatile

~298

~$218K

Minimal

N/A

~80%

Broad / Fragmented

* Platform basket: ALLO, EDIT, NTLA, BEAM, NKTR - pre-commercial optionality names. Excludes commercial-stage specialists (VRTX, REGN,

ALNY) which are not the comparison being made. Employee counts: LinkedIn, June 2026.

** NBIX sales force per 2024 annual report (~600 reps, four teams). Excludes ~30% expansion completed end of Q1 2026.")

The resulting economics increasingly resemble specialty software businesses inside biotech — gross margins consistently above 90%, repeat prescribing behavior, and internally funded pipeline expansion with minimal dependence on external capital. Revenue per employee clusters tightly at $1.3M–$1.4M across NBIX, KRYS, and CORT — three companies of very different scale, age, and indication — against ~$218K for the platform basket. That convergence is harder to dismiss as one company’s idiosyncrasy than a single standout number would be.

- NBIX, KRYS, CORT vs. the platform basket average

$1.35M

$1.33M

$1.39M

$218K

NBIX

KRYS

CORT

Basket

Neurology

Rare Derm

Endocrine/Onc.

ALLO.EDIT.NTLA.BEAM-NKTR

Three companies of very different scale, age, and indication converge inside a $60K band - and sit

roughly 6x above the platform basket on the same metric. That convergence is harder to wave off as one

company's idiosyncrasy than a single standout number would be.

Revenue: TTM as of Q1 2026 close. Employees: current LinkedIn headcount, not 2021-peak. Platform basket figure is aggregate (sum revenue

+ sum employees) across ALLO, EDIT, NTLA, BEAM, NKTR. Source: company filings, LinkedIn, Clinaptis triangulation.

CLINAPTIS ADVISORS")

The framework remains observational rather than statistically proven. However, the consistency of operating characteristics across Neurocrine, Krystal, Corcept, Blueprint and increasingly Cogent suggests the pattern may be more than coincidence. The common denominator is not modality, therapeutic area, or company age. It is the emergence of concentrated specialist ecosystems paired with increasingly self-funded expansion.

One objection deserves a direct answer: NBIX, KRYS, and CORT simply had better drugs. Under that reading, drug quality drives commercial success, which drives stock performance — concentration is incidental. The framework doesn’t dispute that drug quality is necessary. The claim is narrower: concentration determines how much of a good drug’s value actually reaches shareholders. IONS has genuinely important ASO science; it licenses the economics to Biogen and AstraZeneca. PTCT has real assets in DMD; the commercial relationship is Sarepta’s, not PTCT’s. The drug quality was present in both cases. The monetization infrastructure wasn’t. That is the distinction the framework is actually making.

One central question remains open — addressed directly in Section 5: whether the infrastructure that monetizes a first product genuinely transfers to a second, or quietly requires a rebuild each time.

None of this is happening in a shrinking corner of the market, which is worth stating with the actual numbers rather than a rounded estimate. Specialty drugs already account for 51.7% of total US prescription spending as of 2024 — the absolute majority, up from 32% in 2012 — and the concentration is starkest precisely where Mini-Pharma economics live: in Medicare Part D, specialty drugs are just 6.2% of prescriptions but 71.1% of spend. The businesses this note describes aren’t fighting for share of a niche. They sit on top of where the spend already is, and that share has been moving in one direction for over a decade.

If the market is now rewarding concentrated commercial infrastructure over scientific optionality, the most direct test is capital allocation — not what investors say they want, but what acquirers actually paid for.

Interlude — External Validation: Sanofi’s Acquisition of Blueprint Medicines

Sanofi’s $9.1B acquisition of Blueprint Medicines (June 2025, ~27% premium to spot, ~34% to 30-day VWAP) may be the strongest transaction yet consistent with the Mini-Pharma framework.

Sanofi didn’t frame the deal around kinase-platform breadth. Instead cited established presence among allergists, dermatologists, and immunologists, alongside Ayvakit’s commercial positioning in systemic mastocytosis (SM): $479M in 2024 revenue, more than doubling from $204M in 2023, plus $149M in Q1 2025 alone (+61% y/y) — inside a specialist category most platform-era biotech would have considered subscale. Sanofi paid ~19x trailing revenue, a multiple hard to justify on optionality but straightforward against ~85% gross margins, an ~80-rep salesforce, and ~$3.6M revenue per rep — economics that map almost exactly onto the Mini-Pharma operating profile from Section 2.

Not every narrow-indication deal validates the framework. Nestlé paid $2.6B for Aimmune in 2020 on Palforzia’s peanut-allergy approval; in-office dosing killed adoption, and Nestlé wrote it down within three years. CCXI ($3.7B, Amgen, 2022) and RETA ($7.3B, Biogen, 2023) are the better comparators — narrow indications where specialist economics held up. The difference: administration burden and prescriber density, not rarity alone.

Strategic value is accruing after commercial durability is demonstrated, not at the point of scientific optionality. The COGT thesis — same KIT biology, same mast cell physician overlap, dual NDAs now under FDA review — sits directly downstream of this transaction.

The Mini-Pharma framework now has external commercial validation. What it does not yet have is a fully resolved answer to its most important structural question.

3. Platforms Didn’t Die — The Valuation Timing Changed

“Show Me the Product”

The companies now re-rating most durably didn’t wait for the market to reward them — they built the commercial proof that made the re-rating inevitable.

The New Pattern: Validation First, Optionality Second

The companies now re-rating most durably built one economic anchor first, then earned platform credit afterward. NBIX’s Ingrezza became the commercial engine before CNS pipeline optionality received valuation. KRYS’s VYJUVEK demonstrated reimbursement scaling and operational consistency before the HSV-1 platform earned credibility. Pipeline optionality in both cases was funded by internally generated cash, not equity dilution.

COGT is an emerging candidate building toward the same structure — concentrated KIT biology across GIST, NonAdvSM, and AdvSM, same specialist populations, still pre-revenue. CORT’s relacorilant entry into ovarian oncology is the more aggressive test: same cortisol biology, a different physician base entirely, and the most direct live experiment yet on how far therapeutic concentration can stretch before it requires a rebuild.

Sarepta (SRPT) is the contrast case worth sitting with before Dyne’s. SRPT built DMD gene-therapy commercial infrastructure first — Elevidys reached the market years ahead of any competing exon-skipping or gene-therapy franchise in the indication. The credibility-compounding thesis hasn’t been clean: a REMS requirement and a black-box safety signal followed launch, and the market has discounted the franchise accordingly. Infrastructure-first is not sufficient on its own if execution erodes the trust that infrastructure is supposed to compound.

Dyne illustrates the same evolution without — so far — the scar tissue. FORCE was initially valued for breadth; investor attention has since converged around z-rostudirsen as the commercial anchor in DMD, with adjacent neuromuscular and additional exon-target expansion gaining value as validation accumulated. The platform didn’t disappear — it became credible after a franchise emerged.

CRNX is an open question, not a verdict. PALSONIFY approved Sep 2025; Q1 2026 revenue reached $10.3M (up from $5.4M in Q4), 263 prescribers, ~70% reimbursed — early, not obviously weak. The fairer critique is the multi-year stock performance through a tougher endocrine indication: acromegaly’s addressable population and prescriber density are a fraction of TD’s. Whether concentrated endocrinology economics scale the way NBIX’s did remains live.

Regulatory and Operational Compounding

Credibility itself compounds. FDA alignment, manufacturing consistency, and reimbursement execution on one program lower the market’s discount rate on the next — KRYS’s platform designation, DYN’s repeated FDA alignment aren’t regulatory checkboxes, they’re accumulating operational trust pre-commercial platforms can’t replicate. It’s visible across NBIX, KRYS, COGT, and CORT, and may be the most durable structural advantage in the model.

The market is not punishing science. It is repricing when science deserves capital.

Obesity is the obvious exception. LLY and NVO don’t fit this framework — and that’s not a flaw, it’s a scope condition. When the addressable population is large enough to justify manufacturing and distribution scale, raw market size becomes the binding constraint rather than specialist commercial infrastructure. Mini-Pharma economics are a function of specialist density. The framework applies where commercial infrastructure is the bottleneck. Obesity inverted that constraint.

4. The Second Product Problem

The Mini-Pharma framework rests on a single load-bearing assumption: that commercial infrastructure transfers across products rather than requiring a rebuild with each new launch. Everything else in the framework — the SG&A leverage, the regulatory compounding, the lower discount rate — depends on that assumption being true. It is still unproven.

The key unresolved question is not whether focused specialist franchises can scale — Neurocrine’s ~$2.8B revenue base, Krystal’s 34% y/y growth and ~$955M cash exiting FY25, and Corcept’s raised 2026 guidance of $950M–$1.05B already demonstrate that they can. The open question is whether a second product benefits from existing infrastructure or requires rebuilding the commercial organization from scratch — and with it, the operating leverage that defines the model.

Two historical cases frame the downside.

Alexion (ALXN) built durable specialist-ecosystem economics around complement biology — Soliris and Ultomiris owned the nephrology and hematology relationship as completely as NBIX owns movement-disorder psychiatry today. The second product never came: diversification stalled, and AstraZeneca acquired the outcome in 2021. BioMarin (BMRN) is a related but distinct version — Roctavian’s gene therapy in hemophilia A never leveraged BioMarin’s enzyme-replacement relationships (different physicians, different administration model, different payer conversation), and a $2.9M list price met enough resistance that BioMarin has since scaled back investment behind it. Infrastructure transfers when the next product shares the physician relationship and administration model — not automatically because it shares a parent company.

Two live cases are testing this now.

Neurocrine’s Crenessity launch is the cleaner test. The product entered through an existing rare disease team within a field organization of approximately 600 representatives, subsequently expanded ~30% by end of Q1 2026. NBIX’s SG&A ran ~$1.0B in FY25 against $2.8B revenue — a ratio that should compress if Crenessity leverages rather than duplicates that footprint.

CORT’s relacorilant entry into ovarian cancer is the more aggressive test — gynecologic oncologists, not endocrinologists, different reimbursement workflows entirely. CORT enters from strength (~$515M cash, 2026 guidance $950M–$1.05B, approval ~3 months early), but whether the existing ~150-rep infrastructure transfers or requires a parallel build remains open. Early NCCN preferred-regimen inclusion is the right first signal; prescriber breadth beyond the initial oncology core is the real one.

The next two to three years — specifically NBIX’s SG&A ratio through the Crenessity ramp and CORT’s oncology prescriber build — will say which interpretation is correct.

5. Why This Matters To Investors

The six advantages compounding inside NBIX, KRYS, and CORT — and beginning to take shape in COGT as an emerging candidate — are structural to the operating model, not artifacts of the financing cycle that exposed them — which is what should change how investors underwrite biotech going forward, not just how they explain the last four years.

Lower financing risk. R&D at 20%–35% of revenue versus 300%–500%+ means survival doesn’t depend on equity markets staying open. The 2022–2024 reset already tested this once: it determined which companies still existed to have a multiple by 2025. The next drawdown re-tests the same divide.

Greater SG&A leverage. Still unsettled — it’s the live test running through Crenessity and relacorilant (Section 5). If a second product leverages the existing sales force rather than requiring a parallel build, SG&A as a share of revenue compresses with scale in a way platform diversification never does.

Regulatory compounding. FDA alignment, manufacturing consistency, and reimbursement execution on one program transfer credibility to the next — KRYS’s platform designation, COGT’s RTOR and dual Breakthrough designations, DYN’s repeated FDA alignment. Each subsequent program inherits materially lower execution-timeline risk.

Strategic acquisition attractiveness. Sanofi paid ~19x trailing revenue for Blueprint’s KIT-biology franchise — hard to justify on optionality alone, straightforward against a de-risked, functioning specialist ecosystem. CCXI ($3.7B) and RETA ($7.3B) cleared the same logic. Acquirers pay for retired execution risk, not promising science — an embedded takeout floor platform-stage names lack.

Higher forecastability. Repeat prescribing against 90%+ gross margins produces a narrower distribution of outcomes than a platform-stage pipeline tied to binary readouts — and the current XBI tape rewards exactly that: shorter, more legible distances to monetization, independent of the underlying growth rate.

Lower discount rates on future cash flows. The synthesis of the prior five: lower financing, execution, and regulatory risk all compress the discount rate applied to future revenue. A dollar of NBIX or KRYS revenue should carry a lower terminal-value discount than an equivalent dollar of platform-stage revenue — not better biology, just a shorter, cleaner path to it. That’s the actual mechanism behind the multiple gap this note opened with.

None of this is guaranteed. It depends on the answer Section 4 is still waiting on — whether the second product leverages existing infrastructure or rebuilds it from scratch. The market is already pricing the first interpretation. The next 18–24 months of Crenessity and relacorilant data will say whether it’s right.

Disclaimer

This note is published by Clinaptis for informational and educational purposes only. Nothing herein constitutes investment advice or a recommendation to buy or sell any security. Clinaptis is not a registered investment advisor or licensed financial professional.

All data and market figures referenced are sourced from publicly available information including company filings, earnings transcripts, clinical trial publications, and regulatory disclosures. Where figures are triangulated or estimated, this is noted explicitly in the text.

References to market valuation and consensus estimates are analytical tools used to illustrate structural arguments — not calls to action on any specific security. Readers should conduct their own independent research and consult a licensed financial advisor before making any investment decision.

Clinaptis publishes independent market structure commentary on pharmaceutical and biotech categories. All views are the author’s own.