When 45% Isn't Enough: Rethinking Disease Modification in IgAN

Reviewing Vera's Atacicept & Why the Next IgAN Winners Will Be Decided by Residual Disease Burden.

The first generation of IgAN investing was about who could reduce proteinuria. The second generation will be about who leaves the least disease behind.

~45% placebo-adjusted UPCR reduction is now table stakes. Five approved therapies spanning four mechanisms have all cleared it. The market’s analytical error is treating that hurdle as a differentiator when it has become a floor. What actually determines long-term competitive positioning — and eGFR slope preservation over a decade — is not how much proteinuria a drug removes, but how much it leaves behind. Absolute residual UPCR, not relative reduction, is the variable that maps to kidney survival. We built our analysis around that distinction.

We test that hypothesis through three complementary frameworks:

Framework 1 | Biology to Outcomes: Quantitative modelling linking residual UPCR to long-term eGFR preservation across modern IgAN trials, exposing why two drugs with similar proteinuria reductions can produce meaningfully different kidney outcomes.

Framework 2 | Residual Disease Burden: Evaluating atacicept through the variable that actually maps to long-term kidney preservation: absolute residual UPCR after treatment, not headline reduction percentage.

Framework 3 | Mechanistic Possibility: Whether immune-class agents can outperform the hemodynamic eGFR benchmark at similar residual UPCR — and what Tarpeyo’s outlier status implies for atacicept’s Q3 readout.

Each framework arrives at the same place: approval is priced. Commercial leadership is priced. Those are not the same bet.

1. The Category That Changed Overnight

IgAN progresses insidiously, mostly in patients in their 20s and 30s, often without symptoms until eGFR has already declined enough to matter. The pathophysiology is well-characterized: a 4-hit cascade in which galactose-deficient IgA1 triggers autoantibody formation, immune complex deposition in the renal mesangium, and progressive glomerular inflammation. Roughly 30% of patients reach kidney failure within ten years. For two decades, the clinical response was RAAS inhibition — generic, modestly effective, and borrowed from the broader CKD toolkit rather than designed for IgAN’s specific biology.

The FDA’s 2021 acceptance of proteinuria reduction as a reasonably likely surrogate endpoint was the unlock — and it generated genuine therapeutic diversity almost immediately, spanning the B-cell axis, complement cascade, and endothelin/RAAS signaling simultaneously.

What followed was a first-generation land grab. Novartis spent $3.2B on Chinook in August 2023 — acquiring atrasentan and zigakibart while already holding iptacopan — making three mechanistically distinct IgAN bets from a single balance sheet. Asahi Kasei paid ~$1.1B for Calliditas a year later. $4.6B of strategic capital in 18 months didn’t validate the category; it signaled that multiple strategics believed the category was large enough to support parallel winners. That assumption is now being stress-tested.

Tarpeyo was the first approved and the first commercial warning sign. Budesonide’s positioning — targeting the active, hematuria-positive phase rather than chronic maintenance — makes it incidence-driven rather than prevalence-driven. More importantly, its steroid mechanism generates compliance headwinds that have contributed to meaningful real-world churn. Tarpeyo’s commercial trajectory quietly established the template for what IgAN patients actually need: a chronically tolerable, mechanism-specific therapy that durably suppresses the upstream B-cell drivers of disease rather than managing downstream inflammation episodically.

That is precisely what dual B-cell pathway inhibition promises — and why atacicept became the most discussed IgAN asset before a single Ph3 kidney outcome has been reported.

Atacicept enters this market as the most mechanistically upstream asset in the approved class. Dual APRIL/BAFF blockade targets the B-cell survival signals that initiate Gd-IgA1 production — further upstream than endothelin/RAAS pressure reduction, and broader than the APRIL-only inhibition already approved in sibeprenlimab. IgAN’s contained, IgA-dominant pathology may be the indication where the mechanism-to-disease match is tightest. The ORIGIN 3 Ph3 data is clean. The unresolved question — the one this note is built around — is whether that biological coherence translates into the eGFR slope preservation that Filspari demonstrated on label and that the market now uses as the commercial benchmark for every IgAN asset that follows.

Filspari (sparsentan, Travere) is the more instructive commercial proof-of-concept. Despite a REMS program and liver injury warnings at launch, Travere executed well: ~40% proteinuria reduction vs. irbesartan, a statistically significant 1.1 mL/min/yr eGFR improvement at 110 weeks — the first kidney-function preservation claim on any IgAN label — and $320M+ in FY25 revenue, almost entirely from IgAN. FSGS approval only arrived in April 2026 after four years of regulatory friction, partly because endothelin blockade’s acute hemodynamic effect creates an early eGFR spike that makes curve separation slower to confirm. The lesson is not that any IgAN drug with a clean label succeeds — it is that a differentiated, label-supported eGFR claim succeeds. That bar is now set.

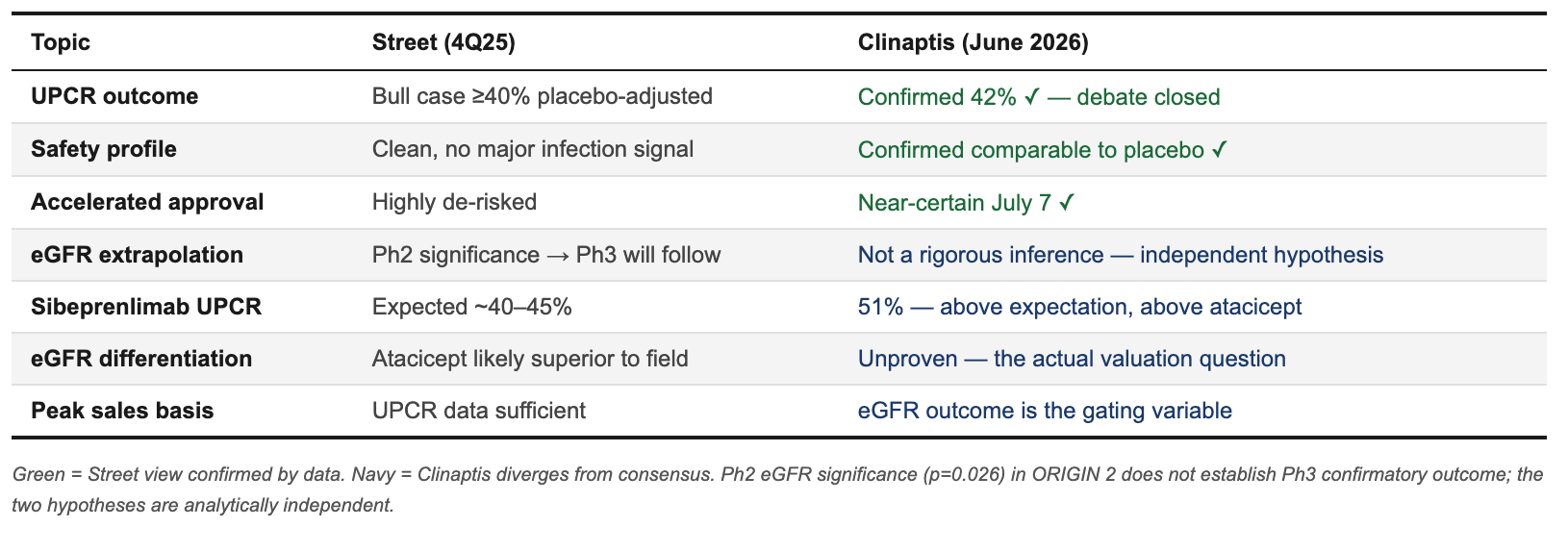

The question entering July 7 is not whether atacicept works. ORIGIN 3 is clean: 42% placebo-adjusted UPCR reduction (p<0.0001), Gd-IgA1 down 68%, hematuria resolved in 81% of baseline-positive patients, safety profile comparable to placebo. Accelerated approval on July 7 is close to a non-event as a binary. The tail risk the market is not pricing is a delay: The live precedent is Filspari in FSGS — a 3-month extension in January 2026 specifically to review eGFR curve separation. An analogous request ahead of July 7 is not the base case, but it is not zero-probability either, and it would reprice VERA back toward the $30s without warning.

VERA peaked at $55 in December 2025 and has not been back since. The subsequent decline through the $40s and into the low-$30s by May and June 2026 was the market slowly reasserting the question the NEJM paper didn’t answer: what does the eGFR look like at two years. The recent bounce to $40+ into the July 7 PDUFA likely reflects a mix of pre-catalyst positioning and short covering rather than a fundamental re-rating. The stock is not cheap on the base case — at $42, the market is implying closer to Scenario A than Scenario B — and approval itself resolves nothing about the variable that actually matters.

The stock is no longer pricing binary PDUFA risk. It is pricing a successful eGFR outcome — a more specific bet, and one the data has not yet supported.

2. The Mechanism Argument — And Why It Doesn’t Fully Resolve

The B-cell axis is the right place to intervene in IgAN. The disease is driven by dysregulated plasma cells producing galactose-deficient IgA1, which forms immune complexes depositing in the renal mesangium and triggering progressive glomerulonephritis. Two cytokines govern the sustaining B-cell signals: BAFF, which supports general B-cell maturation broadly across immunoglobulin classes, and APRIL, which signals through TACI and BCMA to promote long-lived plasma cell survival — the population directly responsible for persistent Gd-IgA1 production. Atacicept binds both simultaneously via a soluble TACI-Fc fusion protein, disrupting both the initiation and perpetuation of the Gd-IgA1 cascade.

APRIL > BAFF. The available evidence tilts toward APRIL carrying the primary load. Anti-APRIL neutralization reduces Gd-IgA1 synthesis at the plasma cell level; anti-BAFF suppresses B-cell survival broadly without IgAN-specific selectivity. Preclinical data support the hierarchy. And the clinical record outside IgAN adds a caution: in multiple sclerosis, atacicept worsened disease activity in a Ph2 trial, attributed to depletion of regulatory B-cell populations that BAFF supports. Dual blockade does not universally mean dual benefit. Sibeprenlimab — APRIL-only — received accelerated approval three months before atacicept’s PDUFA with a numerically stronger proteinuria headline: 51% vs. 42% placebo-adjusted UPCR reduction. If APRIL does the primary mechanistic work, the incremental BAFF arm is biological plausibility priced as clinical certainty.

The one signal that partially supports differentiation is hematuria resolution. The 81% resolution rate in ORIGIN 3 among baseline-positive patients is not noise — the 2025 KDIGO guidelines now formalize hematuria as a disease activity staging tool, separating immunologically active patients where B-cell targeting has maximum leverage from those in the sclerotic phase where CKD management dominates. It is atacicept’s cleanest patient-selection argument, without a directly disclosed parallel in VOYXACT’s Ph3 data. Whether it translates into prescribing differentiation is an unanswered commercial question.

What the mechanism argument cannot resolve is the eGFR question. Whether disrupting both BAFF and APRIL produces a kidney function trajectory meaningfully better than APRIL alone — or than the endothelin/RAAS dual blockade Filspari already demonstrated on label — requires two-year slope data. Three frameworks follow.

3. The eGFR Translation: Three Frameworks, One Uncomfortable Picture

Proteinuria is the surrogate that got these drugs approved. eGFR is the outcome that determines whether they stay approved — and whether the commercial story holds.

The FDA’s 2021 surrogate acceptance was a pragmatic regulatory move, not a clinical equivalence statement. The Filspari FSGS case made the stakes explicit: when Travere sought full approval for sparsentan in FSGS, the FDA issued a 3-month delay — January to April 2026 — specifically to review eGFR curve separation before granting traditional approval. That is the template for what VERA faces in Q3. Accelerated approval on July 7 is close to certain on the UPCR data. What happens to the stock between July and Q3 eGFR readout is a different question.

Full approval requires demonstrated eGFR preservation; payers and nephrologists ultimately care about kidney function, not a surrogate. In a field with four approved agents converging on similar proteinuria responses, eGFR slope is the only variable that creates durable market separation.

A KOL data point sharpens the competitive framing. Jonathan Barratt — a primary PROTECT investigator and one of the most cited IgAN clinical voices — has suggested that a 15–20% absolute UPCR difference between agents would be required for clinically meaningful separation. The gap between atacicept (42% vs. placebo) and sibeprenlimab (51% vs. placebo) is 9 percentage points, below that threshold. This is not a disqualifying observation: the two trials are not head-to-head and patient populations differ. Below the Barratt threshold, the UPCR debate settles nothing. eGFR slope is where the differentiation case will be made or lost.

Framework 1 — Biology to Outcomes

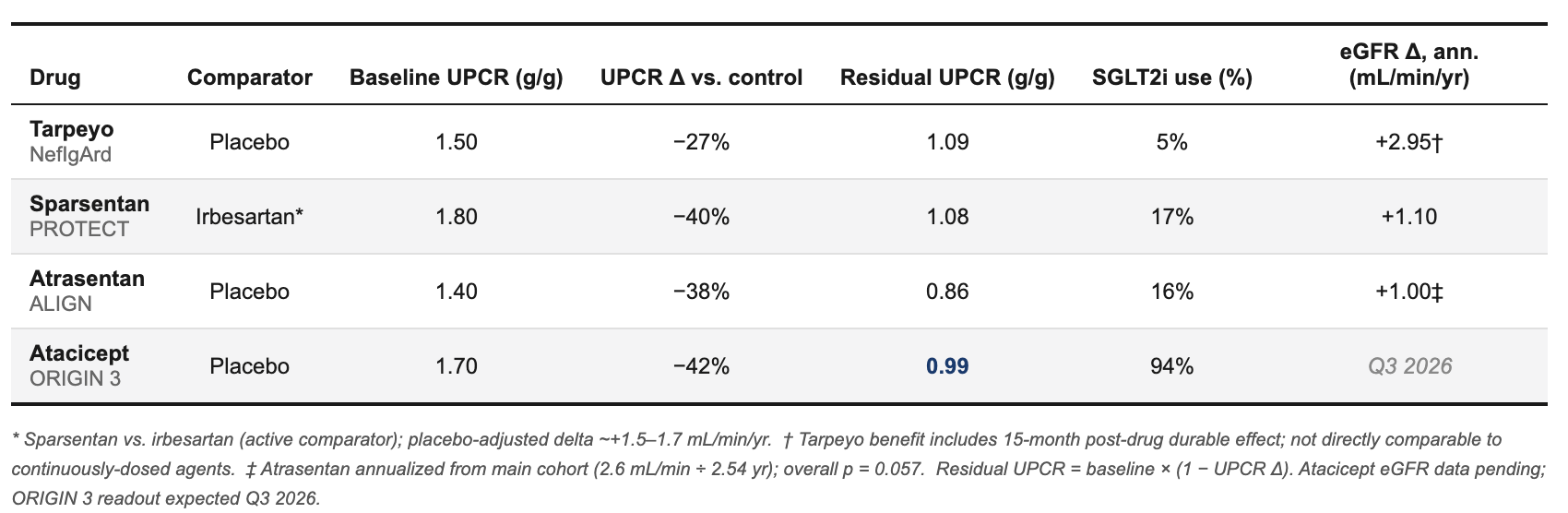

The published IgAN evidence includes three Ph3 trials with both proteinuria and eGFR slope data from placebo- or active-controlled studies over ≥2 years.

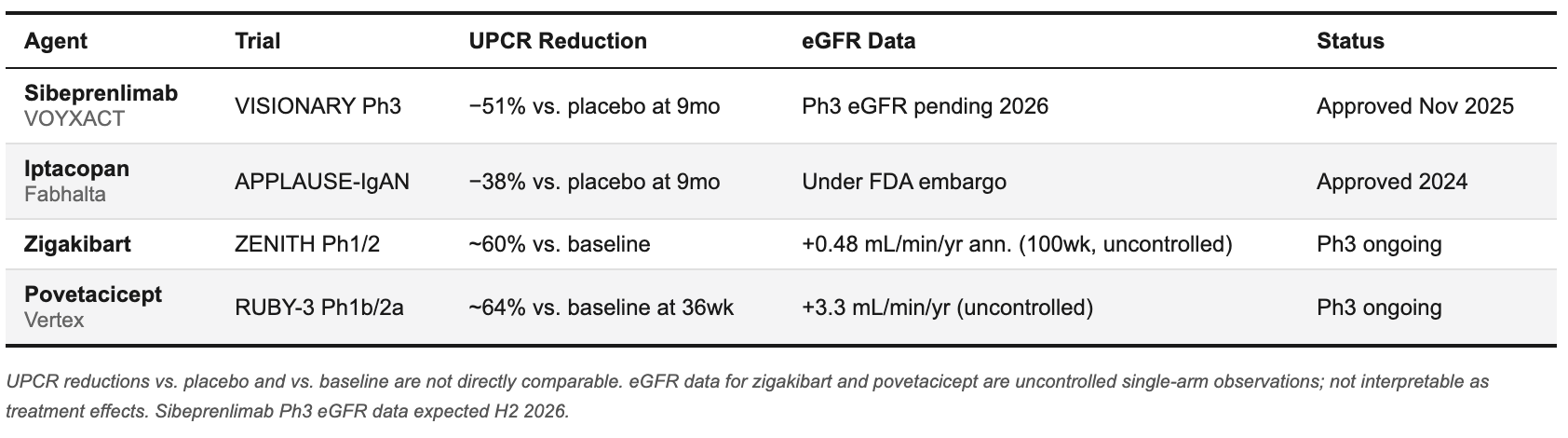

For context, earlier-stage and uncontrolled data from other category participants:

These are context, not anchors — eGFR data are either embargoed, uncontrolled, or too early-stage for placebo-controlled slope comparisons.

The SGLT2i column deserves close attention. Across the three historical anchors, background SGLT2i penetration ranged from 5% to 17%. In ORIGIN 3 it is 94% — a categorically different trial environment, and the largest source of uncertainty in translating historical eGFR benchmarks to ORIGIN 3. SGLT2i independently reduces proteinuria by ~20–30% and slows eGFR decline by ~1–2 mL/min/yr. Both the atacicept and placebo arms carry that benefit — meaning the incremental gap between drug and placebo is competing against a better-protected placebo arm than any prior IgAN trial has faced. The directional analog: atrasentan’s SGLT2i subgroup (n=64, exploratory) showed 3.0 mL/min/yr vs. 1.0 mL/min/yr in the main cohort. Small sample, but it quantifies the direction of the effect.

Cross-trial benchmark range for ORIGIN 3: +1.0–1.4 mL/min/yr — anchored to sparsentan and atrasentan at similar baseline UPCR, adjusted for SGLT2i compression of the placebo arm. Not a point prediction. The empirical zone where the data place the base case before mechanism or subgroup factors are applied.

The FDA’s own registry-based translation model — which predicted 6.4 mL/min/1.73m² total eGFR separation from a 30% proteinuria difference in the PROTECT filing — overestimated sparsentan’s realized benefit by approximately 3×. The point-in-time surrogate systematically overstates long-term kidney protection. That is not a Clinaptis-specific concern. It is documented in the agency’s own statistical review.

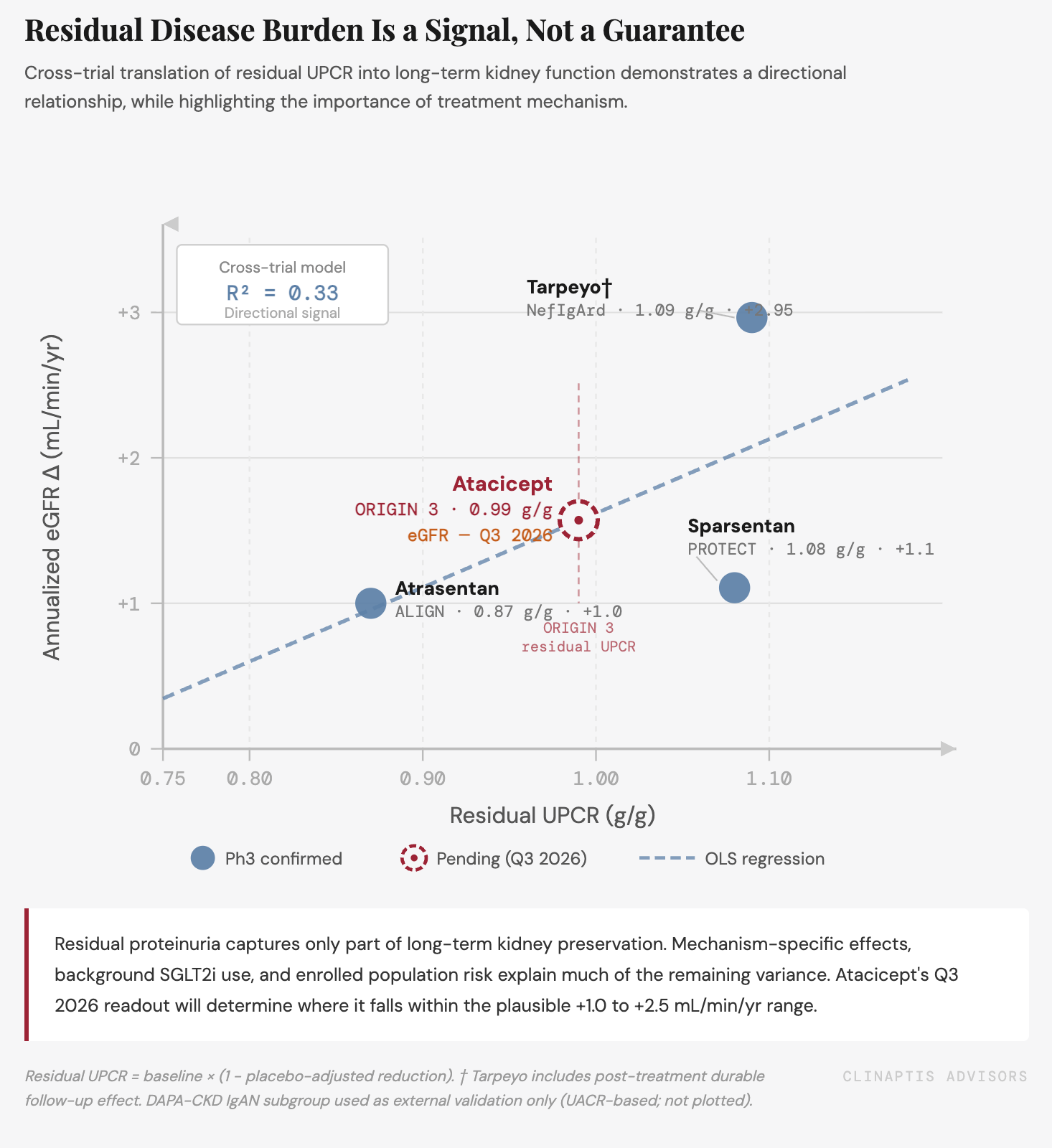

Framework 2 — Residual Disease Burden

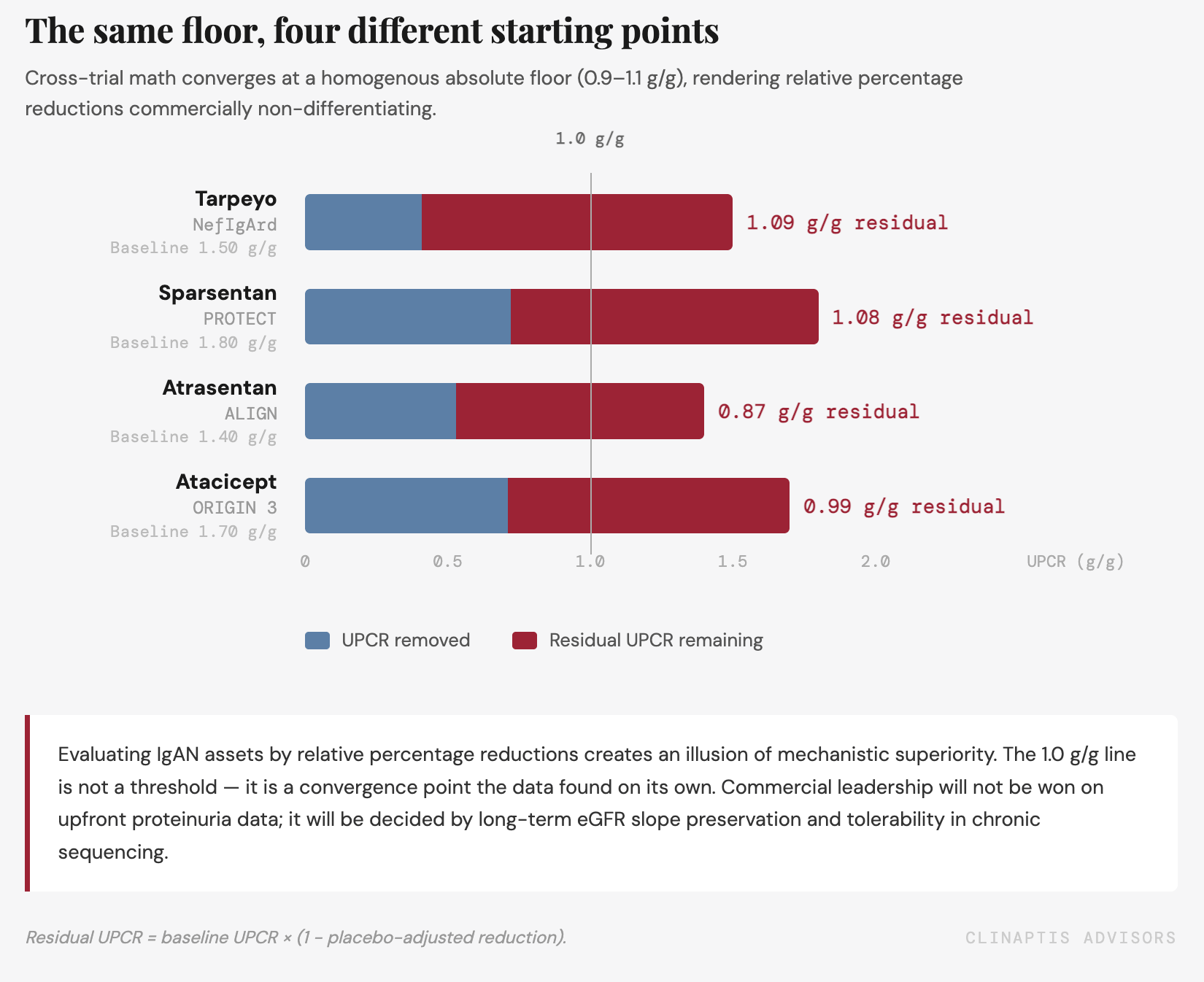

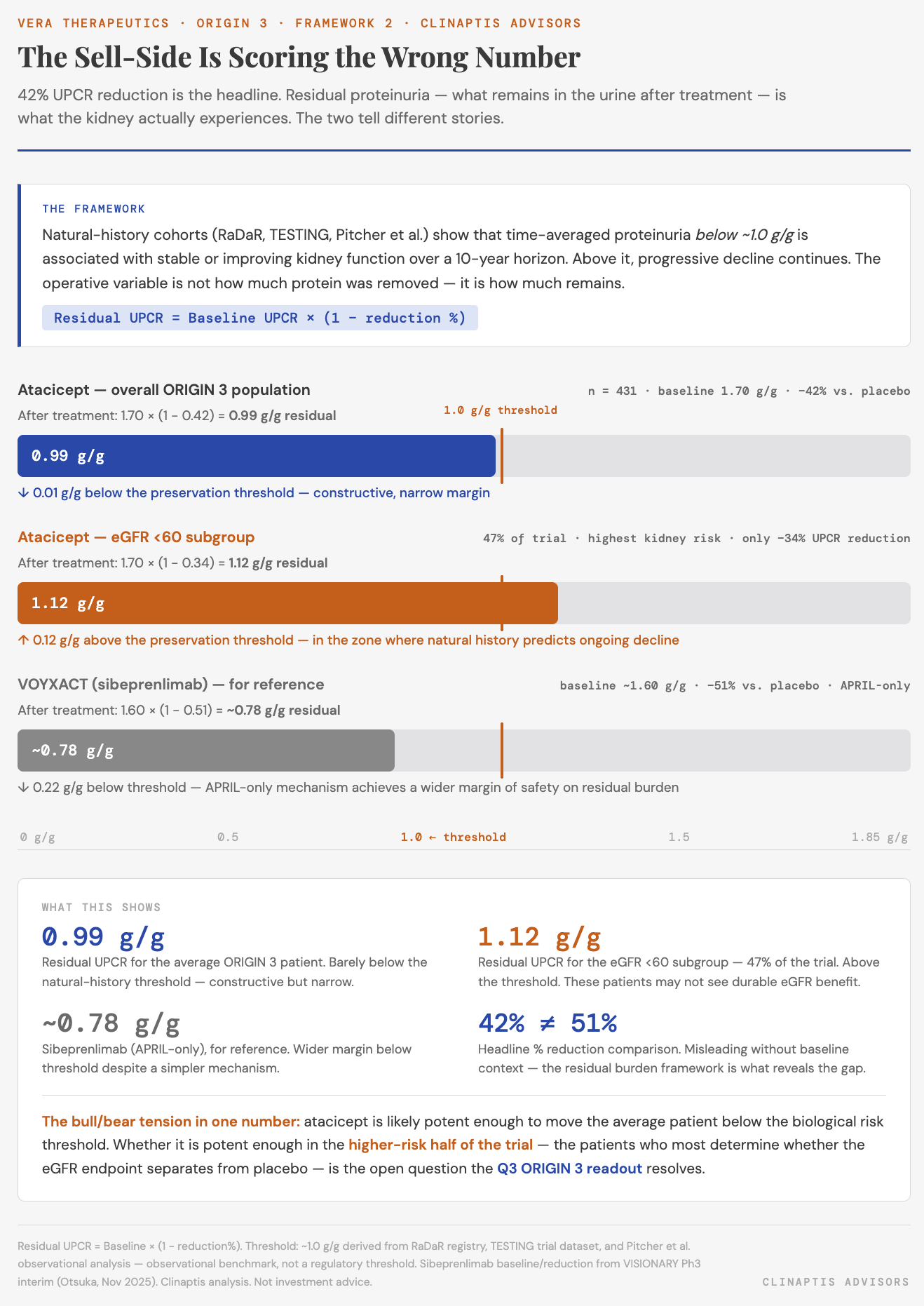

Rather than comparing headline proteinuria reductions across trials, we ask a different question: is kidney preservation proportional to the residual disease burden after treatment? This framing is underused in the IgAN investment literature — and it changes what the ORIGIN 3 data actually shows. What the kidney experiences is not the percentage reduction in the press release — it is the absolute proteinuria that remains after treatment. Residual UPCR is how natural-history cohorts stratify long-term kidney risk: the RaDaR registry, the TESTING trial dataset, and the Pitcher et al. observational analysis consistently show that time-averaged UPCR below ~1.0 g/g is associated with stable or improving eGFR over a 10-year horizon — above it, progressive decline continues at a rate that compounds over decades in a disease that mostly strikes patients in their 20s and 30s. That ~1.0 g/g level is the natural-history inflection point this framework uses as its reference.

On this measure, atacicept’s 42% reduction from a 1.70 g/g baseline leaves residual UPCR at ~0.99 g/g — one hundredth of a gram below the inflection point. Constructive, but the margin of safety is narrow and the distribution of response within that average matters enormously.

The eGFR <60 subgroup is where the framework focuses uncomfortably. Patients with baseline eGFR below 60 mL/min/1.73m² — 47% of ORIGIN 3 — showed only ~34% UPCR reduction vs. placebo against ~45% in the eGFR ≥60 cohort. Residual UPCR in that subgroup: ~1.12 g/g, above the inflection point. These are the patients most dependent on eGFR protection, landing in the zone where observational data predicts continued decline regardless of treatment. That the high-risk half of the trial shows attenuated proteinuria response is not a rounding error in the ORIGIN 3 eGFR prediction.

The severe proteinuria subgroup adds a second cut of the same concern. Among ORIGIN 3 patients with baseline UPCR ≥2.0 g/g — the highest-risk stratum, where progression to ESKD is fastest — percentage reductions look strong but residual burden remains elevated. A patient starting at 2.5 g/g achieving 42% reduction carries ~1.45 g/g residual, well above the natural-history inflection point. The residual UPCR framework is most damning precisely where the disease is most severe: the two subgroups that most need kidney protection are the two subgroups landing furthest above the reference level.

Framework 3 — Mechanistic Possibility

The residual UPCR framework is built on hemodynamic data — and that is a structural limitation. Sparsentan and atrasentan reduce intraglomerular pressure, mechanically lowering proteinuria and preserving filtration surface area. Tarpeyo works differently: gut mucosal immunomodulation resets Gd-IgA1 production upstream, with a post-treatment effect that may partly reflect both immune reset and withdrawal design. That partially explains why Tarpeyo plots as an outlier — nearly identical residual UPCR to sparsentan (~1.08–1.09 g/g), 2.7× the annualized eGFR benefit. Mechanism class explains what residual UPCR alone cannot; the cross-trial R² is 0.34, not 0.95, for exactly this reason.

Atacicept belongs to the immune mechanism class alongside Tarpeyo, not the hemodynamic class. If dual APRIL/BAFF blockade produces genuine disease modification — reducing mesangial immune complex deposition, attenuating complement activation, resetting the inflammatory cascade at the tubular level — then the empirical benchmark of +1.0–1.4 mL/min/yr may be a floor rather than a ceiling. The 68% Gd-IgA1 reduction and 81% hematuria resolution in ORIGIN 3 are directionally consistent with upstream disease modification.

The mechanism argument cannot be quantified from available data — but it reframes what the Q3 readout actually tests. Proteinuria is unlikely to translate linearly into kidney protection across mechanism classes. Hemodynamic therapies establish one empirical benchmark;

upstream immune therapies may preserve kidney function beyond what proteinuria reduction alone would predict. The ORIGIN 3 eGFR readout therefore tests not only whether atacicept works, but whether dual APRIL/BAFF blockade demonstrates biological leverage beyond conventional proteinuria lowering. That is a more interesting question than the Street is asking — and a more consequential one for how the IgAN category gets valued from here.

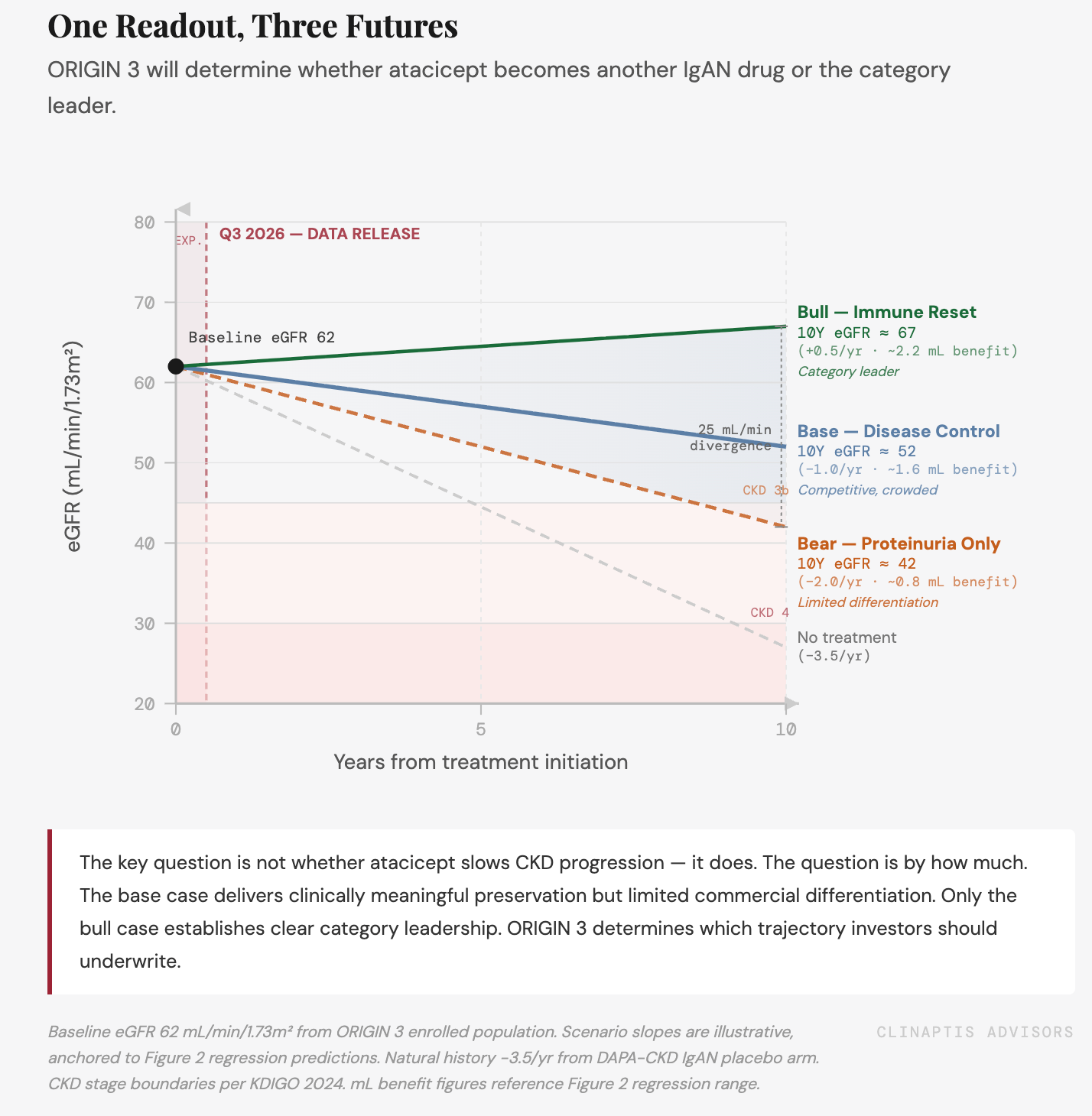

What the three frameworks converge on: The empirical benchmark puts the base case at +1.0–1.4 mL/min/yr, compressed by an unprecedentedly well-protected placebo arm. The natural history framework shows the average patient barely below the preservation threshold, with the high-risk subgroup above it. The mechanism framework is the only pathway to the bull case — and it requires a hypothesis confirmed by Q3 data, not evidence already in hand.

A forward note: The framework above uses endpoint proteinuria — the week-36 snapshot — as the key variable. Natural-history cohorts use time-averaged proteinuria across the full observation window. Time-Integrated Residual Proteinuria (TIRP) — cumulative kidney burden across the full 2-year ORIGIN 3 curve, weighted by duration — is a more biologically faithful variable than any single timepoint. We will test it when the full dataset lands in Q3.

Key Questions for Q3 2026

① Does ORIGIN 3 eGFR Δ reach ≥1.8 mL/min/yr vs. placebo?

Below +1.4, the commercial case compresses materially and a disease-modification label claim is out of reach.

② Does the eGFR <60 subgroup separate from placebo?

47% of the trial sits at residual UPCR ~1.12 g/g — above the natural-history preservation threshold. If this cohort doesn’t separate, the overall endpoint may not either.

③ Does immune biology outperform the hemodynamic benchmark?

Tarpeyo — same residual UPCR as sparsentan — delivered 2.7× the eGFR benefit. Atacicept plotting above the hemodynamic regression line validates the APRIL/BAFF premium. Plotting on it doesn’t.

④ Does VOYXACT report comparable eGFR concurrently?

If sibeprenlimab matches or exceeds atacicept’s eGFR outcome, the incremental BAFF contribution is effectively disproven in a clinical setting.

Three analytical frameworks, one commercial implication: the eGFR readout in Q3 is not a catalyst that confirms an already-de-risked story. It is the event that determines whether the commercial thesis is structurally sound or built on a proteinuria surrogate that the market has temporarily chosen to treat as equivalent to clinical benefit. The market sizing below assumes that distinction matters — because payers, nephrologists, and treatment guidelines will eventually make it matter, regardless of what the July 7 label says.

Where the Street Was — and Where the Debate Has Moved

The proteinuria debate is effectively over. The eGFR debate is just beginning. The note being written today is fundamentally different from the one the Street was writing six months ago — and being explicit about that evolution is part of the analytical value.

The Street’s prior error was conflating proteinuria success with eGFR probability. Phase 2 showed statistically significant eGFR at 36 weeks in an underpowered n=116 trial — not a rigorous basis for predicting Phase 3 eGFR in a 431-patient, 94%-SGLT2i-background, 2-year confirmatory study against a better-protected placebo arm than any prior IgAN trial has faced. Our framework separates the two explicitly: the proteinuria story is proven; the eGFR story requires Q3.

4. Market Structure: What’s Actually Being Treated Today

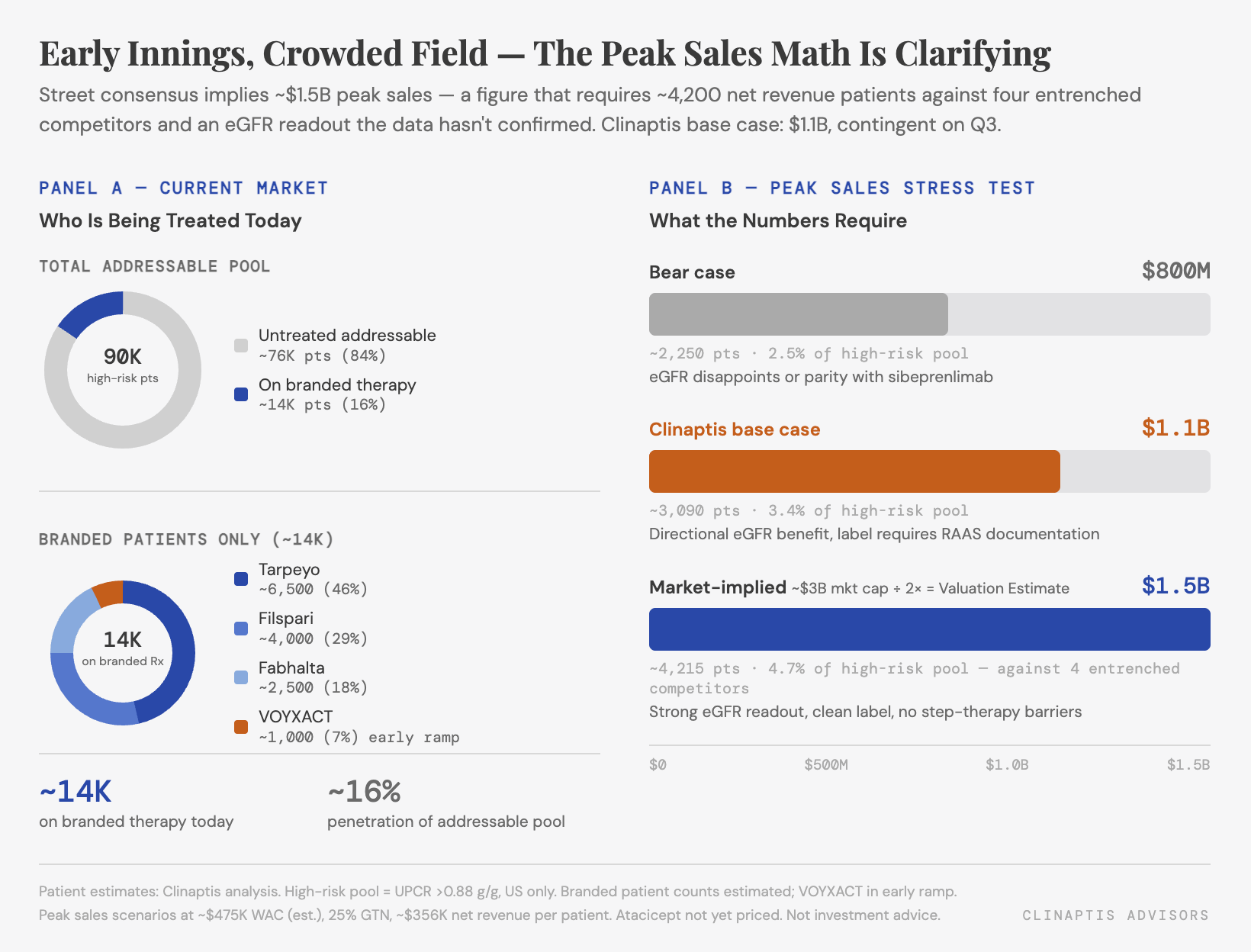

The market is real, early, and already competitive. The US IgAN patient pool of ~160K total stratifies to ~90K high-risk patients (UPCR >0.88 g/g) — the Ph3-eligible population. Of those, roughly 14,000 are estimated to be on branded therapy today across the four approved agents, implying ~15–16% penetration of the addressable pool. That’s early innings by any chronic-disease standard.

But this market is not empty — it is being built by agents that arrived before atacicept. Tarpeyo, Filspari, and Fabhalta have established real-world prescribing patterns, managed-care contracts, and step-therapy protocols. Sibeprenlimab arrived three months ahead with a larger sponsor and a stronger proteinuria headline. VERA launches fifth into a category where the treatment algorithm is actively hardening.

The peak sales math is clarifying. At ~$475K annual WAC and 25% GTN discount, net revenue per patient is ~$356K. VERA’s current ~$3B market cap, at a 2x peak-sales multiple implicit at this stage of development, implies ~$1.5B in worldwide peak sales — a multiple that already discounts outer-year cash flows. Reaching $1.5B requires roughly 4,500 net revenue patients, ~5% of the high-risk pool, against four entrenched competitors. The Clinaptis base case of $1.1B requires ~3,100 patients — achievable with a differentiated eGFR outcome, difficult without one. Without clearly superior eGFR data, step-therapy behind VOYXACT compresses the commercial ceiling toward $800M–$1B.

The prescribing decision for nephrologists is not obvious. IgAN lacks a routine clinical biomarker that identifies which patients need APRIL-only vs. dual APRIL/BAFF blockade. A high-volume nephrologist managing a 35-year-old with UPCR 1.8 g/g, hematuria, eGFR 58, already on max RAAS therapy and SGLT2i, has three incoming B-cell modulator options — sibeprenlimab (approved, monthly SC), atacicept (weekly SC, if approved), and eventually povetacicept (Vertex, Ph3 ongoing). Without a compelling eGFR story separating atacicept from sibeprenlimab, the decision defaults to formulary access, dosing convenience, and real-world experience depth. Atacicept enters that conversation without an advantage on any of the three.

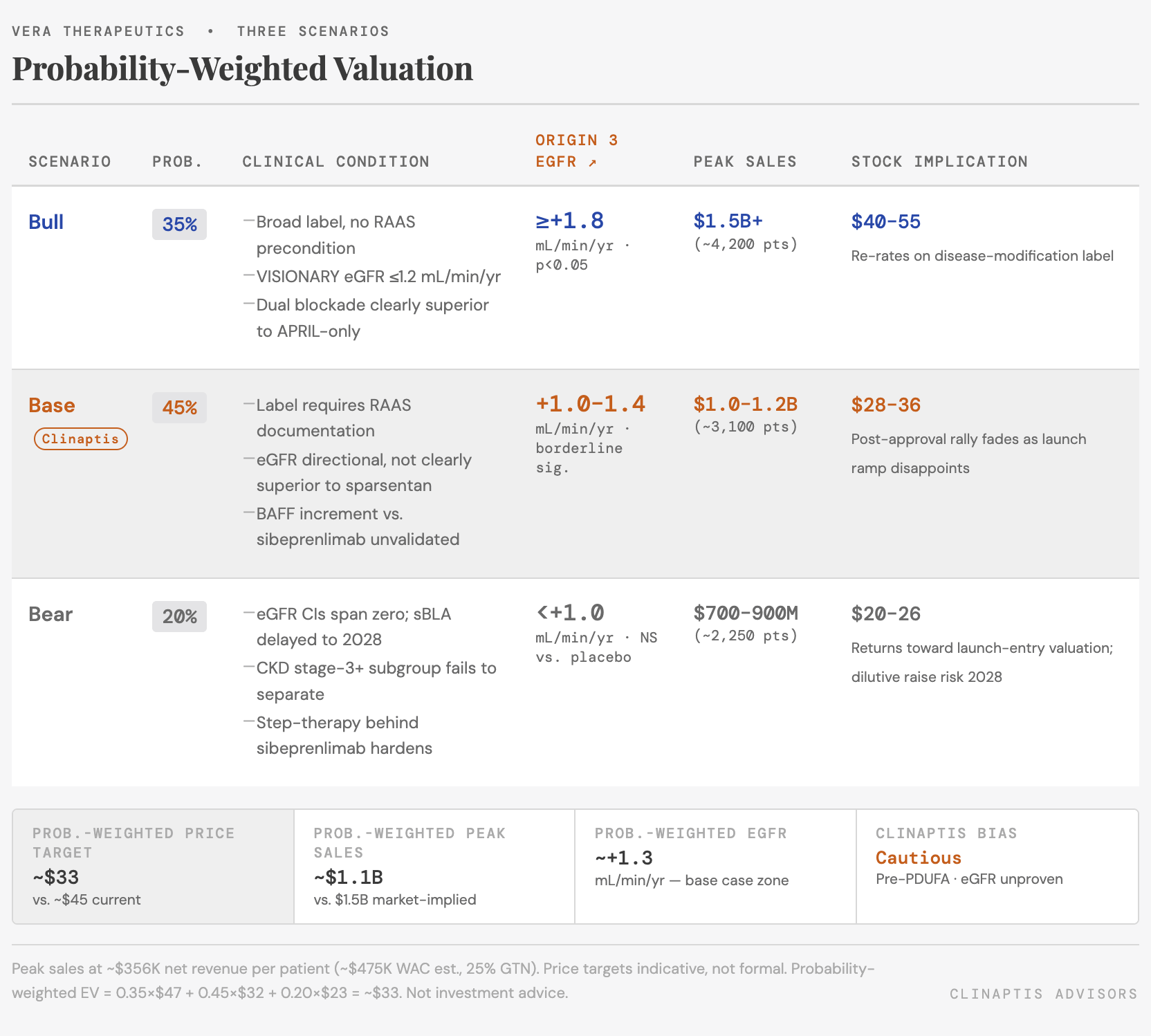

5. Three Scenarios

The Street is constructive to bullish. Accelerated approval probability is priced near 1.0, the Q3 eGFR readout is framed as an upside catalyst, and peak sales estimates cluster around $1.5B+. The market is anchored on the UPCR headline and discounting three things simultaneously: eGFR uncertainty, label qualification risk, and competitive dynamics that have shifted materially since sibeprenlimab’s November 2025 approval.

The probability mass sits in Scenario B for one reason: the eGFR data doesn’t exist yet. Street consensus is effectively pricing Scenario A at close to 1.0 — clean label, strong eGFR, disease-modification framing. That requires the Q3 ORIGIN 3 readout to show Δ≥1.8 mL/min/yr in a trial where the placebo arm carries 94% SGLT2i background, where the eGFR <60 subgroup showed only 34% UPCR reduction, and where the mechanism premium over an already-approved APRIL-only agent remains unquantified in any head-to-head setting.

The bear case is not a collapse — it is the specialist-drug adoption pattern that nephrology knows well. High-volume nephrologists managing IgAN patients are already writing Filspari and VOYXACT; atacicept enters without real-world data, without a published eGFR label claim, and at a price point that is currently unknown — positioning above sibeprenlimab’s WAC without a clearly superior eGFR outcome creates a payer conversation VERA’s launch team will need to win repeatedly, account by account. Step-therapy hardening behind an established agent is how rare-kidney commercial ramps disappoint without the drug ever failing clinically. The eGFR readout in Q3 is the variable that separates all three paths.

6. Bottom Line

The PDUFA is not the event. Accelerated approval arrives July 7 — the UPCR data is NEJM-quality, the surrogate precedent in IgAN is well-established across four prior approvals, and there is no safety signal that would support a CRL. The real analytical questions are what the label says and what the Q3 eGFR readout delivers. Expect a short-term post-approval rally; expect the stock to reprice as attention shifts to launch trajectory numbers and the eGFR readout timeline.

What changes our view to Bullish:

ORIGIN 3 demonstrates eGFR preservation ≥1.8 mL/min/1.73m²/year versus placebo (p<0.05), supporting disease modification beyond proteinuria reduction.

Regulatory label reinforces commercial differentiation, including favorable kidney-function language and no clinically meaningful safety restrictions or monitoring burden that would limit physician adoption.

VISIONARY Phase 3 eGFR data (expected concurrently) reports ≤1.2 mL/min/1.73m²/year, establishing clear differentiation of dual BAFF/APRIL blockade over APRIL-only inhibition.

Any one of these would move our view from cautious to neutral. All three would support a meaningful re-rating.

What confirms the Bear case:

ORIGIN 3 eGFR benefit <1.4 mL/min/1.73m²/year, implying limited kidney-function differentiation despite robust proteinuria reduction and little evidence of a meaningful biological premium.

Treatment sequencing may favor hemodynamic agents first — positioning atacicept as a later-line option for patients with persistent disease activity despite optimized supportive care. If that pattern hardens in formulary protocols, the addressable first-call patient population narrows materially.

VISIONARY reports eGFR preservation at parity or better, eliminating the proposed BAFF premium and weakening the differentiation thesis for dual BAFF/APRIL blockade versus APRIL-only inhibition.

What to watch after July 7:

Label indication wording, not the approval headline

eGFR language from Phase 2b in the initial label — positive signal if present

Managed-care contracting and VOYXACT step-therapy positioning

ORIGIN 3 eGFR topline in Q3

Monthly SC formulation disclosure

Zigakibart ZENITH Ph3 readout

Drawdown cadence on the $500M term loan

Bias ahead of PDUFA: Cautious. The mechanism is promising, the proteinuria data is real, the market opportunity is genuine — and the commercial case is softer than the consensus has priced.

Clinaptis Advisors | This note is for informational and educational purposes only and does not constitute investment advice. All data sourced from publicly available company filings, clinical trial publications, regulatory disclosures, and earnings transcripts. Where figures are triangulated or estimated, this is noted explicitly in the text.