XBI 2026: What the Tape Is Rewarding vs. Punishing

Why 2026 Became a Market for Visibility, Reinforcement, and Shorter Timelines

Capital didn’t leave biotech in 2026. It rotated aggressively within it.

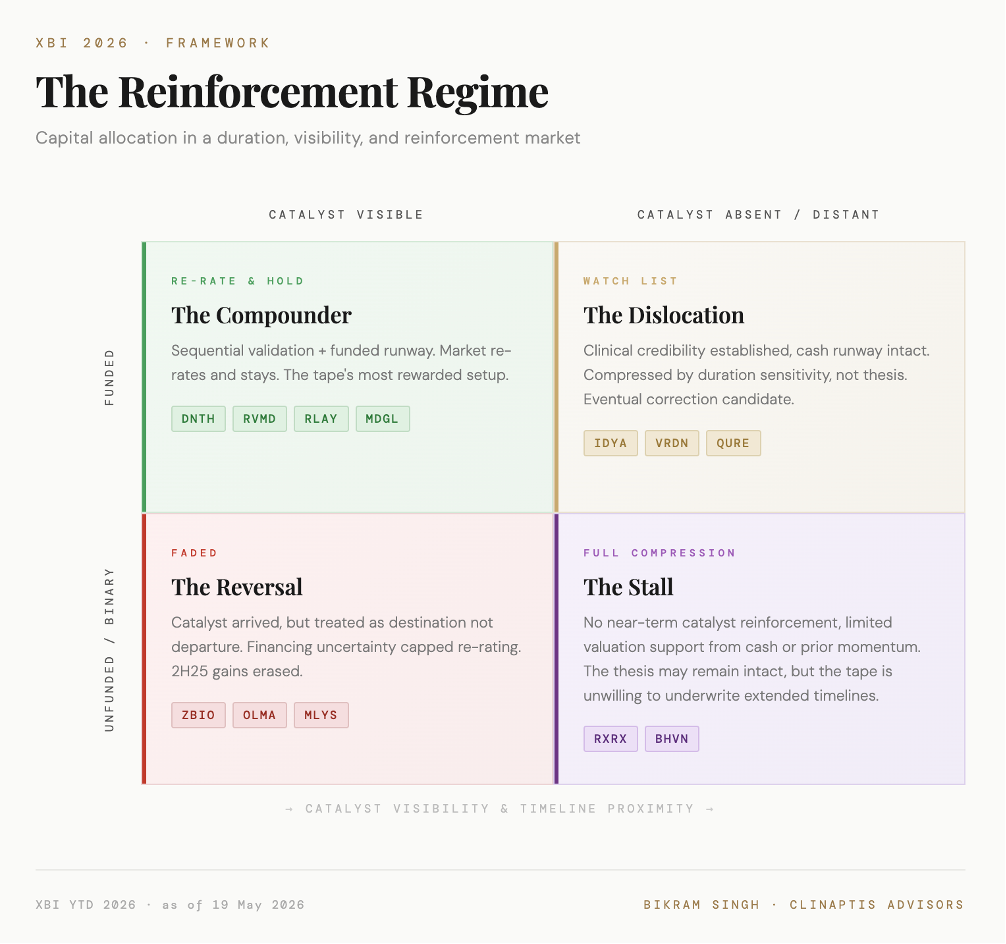

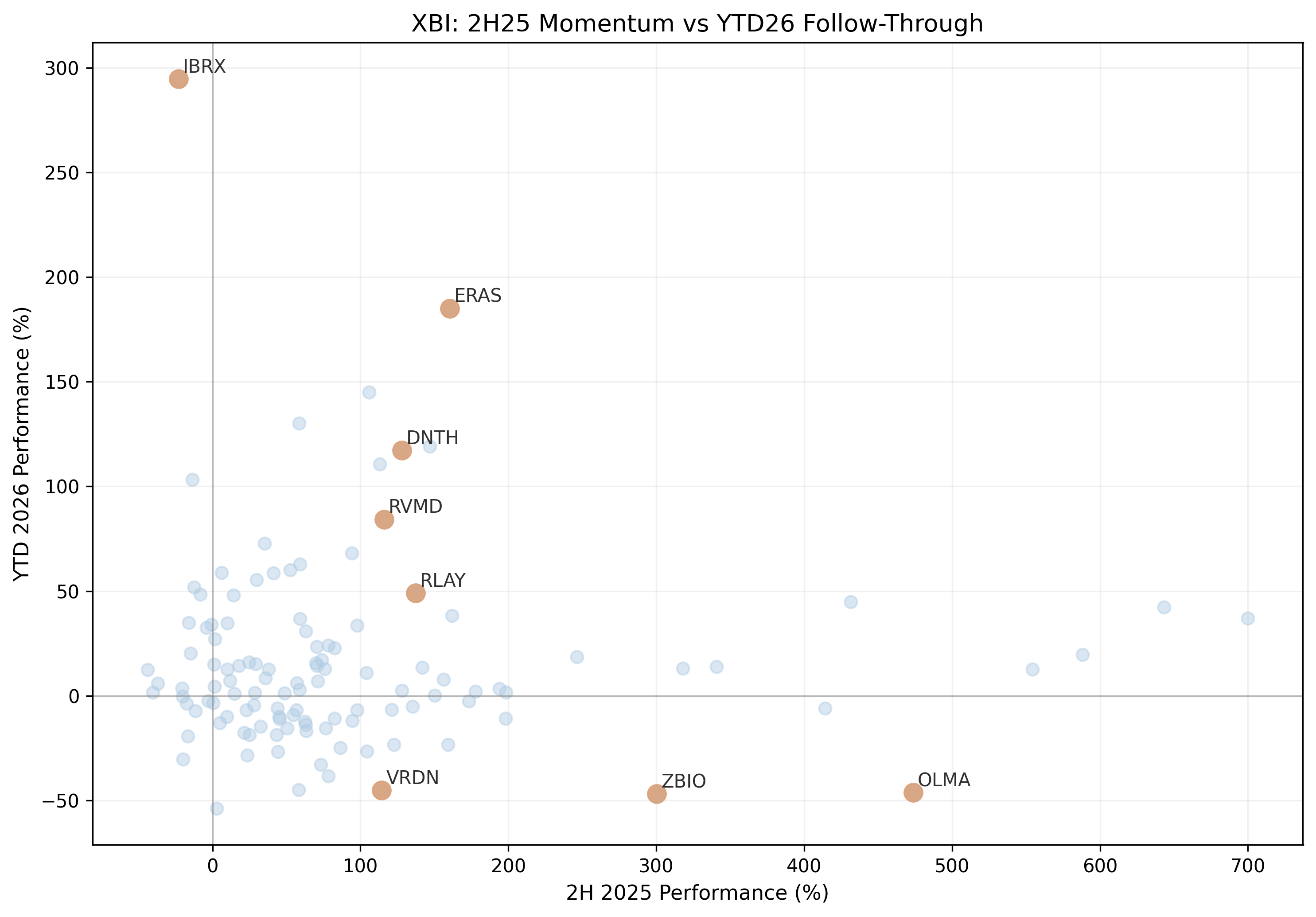

The broader XBI cohort is roughly flat (median +2% YTD) - a more constructive headline than most expect. But beneath that, dispersion has been extreme: downside clustered near -50% to -60%, upside extending toward +185–295%. The top cohort — IBRX (+295%), ERAS (+185%), SYRE (+145%), TNGX (+130%), DNTH (+117%), ANAB (+111%) — shares one feature: a shortening, visible path to asset monetization or clinical inflection. IBRX shifted from launch potential to early revenue scaling. ERAS de-risked its pan-RAS oncology platform. DNTH secured a fully funded Phase 3 path in autoimmune. Convexity and positive surprise — not stability — are driving returns.

This is not a macro story, though the backdrop hasn’t helped. Rising geopolitical tensions, higher energy prices, and renewed Fed uncertainty have amplified duration sensitivity — and XBI, heavily weighted toward pre-commercial SMID-cap names, absorbs that disproportionately.

But the deeper story is internal to biotech. The 2026 tape is a duration, visibility, and reinforcement market. What follows is a breakdown of what that means — and which names it’s rewarding and punishing.

1. The Market Is Rewarding Shorter Timelines

Many of the weakest YTD 2026 performers materially outperformed in 2H25 before sharply reversing. VRDN (+114% → -56%), ZBIO (+300% → -44%), OLMA (+473% → -43%), MLYS (+159% → -25%), VERA (+122% → -26%), ARQT (+104% → -20%), QURE (+70% → -14%), and PTCT (+56% → -15%) all delivered +50–300%+ returns in 2H25 followed by meaningful YTD declines.

The common thread was not clinical failure, but transition from discrete valuation unlocks into longer-duration execution cycles. 2H25 momentum was driven by pivotal or proof-of-concept data (MLYS, QURE), positioning into major readouts (OLMA), commercial acceleration narratives (ARQT, PTCT), and thematic inflows into high-interest categories like FcRn and IgA nephropathy (VRDN, VERA).

Once those catalysts passed, the market focused on what remained between current positioning and durable commercial realization: additional P3 timelines, launch execution, competitive pressure, indication expansion. Timing gaps and in-line progression are now treated as duration risk, not neutral outcomes.

An important distinction: most of what reads as 2026 weakness is 2H25 normalization. The majority of the worst YTD performers were up 50–470% in the prior six months — the 2026 decline is digestion, not deterioration. The names where genuine new weakness is occurring — RXRX, down in both periods; ADMA, barely recovered before breaking further — are a smaller and more concerning cohort.

2. Commercial Infrastructure Did Not Prevent Multiple Compression

Revenue, institutional ownership, and commercial franchises did not act as the floors many expected. Alnylam (-28%), Insmed (-38%), BioMarin (-13%), BridgeBio (-16%), and Madrigal (-12%) all declined materially — none for lack of operational execution.

The logic is consistent across names: where upside revision has stalled, multiples compress regardless of business quality. ALNY grew revenue; the problem was that growth no longer surprised. INSM’s -38% decline is the starkest in this cohort — a name with a genuinely strong commercial franchise in pulmonary arterial hypertension, punished not for execution failure but for running into an elevated expectations set built during a 78% 2H25 rally. BBIO and BMRN face the same dynamic: strong franchises, forward estimates no longer moving in a direction that justifies premium positioning.

MDGL is the cleanest illustration. Rezdiffra generated $311M in Q1 2026 net revenue with 42,000+ active patients — a strong launch by any historical benchmark. The stock still fell ~12% YTD as peak MASH positioning normalized and embedded M&A assumptions partially unwound.

Commercial scale extends survivability. In 2026, it does not sustain premium multiples without continued forward revision.

3. Platform Value Now Requires Clinical Credibility

The 2026 tape has drawn a sharper distinction within platform-oriented biotech — not between platforms and non-platforms, but between companies generating meaningful clinical evidence in defined patient populations and those still asking investors to underwrite the discovery engine itself. Platform breadth without demonstrated efficacy in commercially relevant indications is receiving limited valuation credit.

The divergence is legible across three names:

RVMD (+84% YTD): Daraxonrasib’s AACR 2026 data answered the question the tape cares about most: is this a one-asset story or the beginning of a scalable oncology franchise? Combination data in frontline RAS-mutant PDAC (n=40) delivered 58% ORR, 84% 6-month PFS, and 90% 6-month OS; monotherapy showed 47% ORR and 92% disease control. Three simultaneous Phase 3 programs across PDAC and NSCLC shifted underwriting from “RAS platform optionality” toward a registrational oncology franchise with expanding commercial scope.

RXRX (-30% YTD): EC-4881 FDA pathway discussions represent one of the first meaningful signs that Recursion’s AI discovery engine can generate registrational assets. Until that transition becomes repeatable and not singular, the market is assigning limited value to platform breadth alone.

The RVMD/RXRX contrast is the section’s core point: the distinction is no longer scientific ambition or platform sophistication, but proximity to durable commercial and regulatory outcomes.

IDYA (-17% YTD) represents a third and different case — a name where clinical credibility is arguably already established. OptimUM-02 data in uveal melanoma (HR 0.42; median PFS 6.9 vs 3.1 months) advanced darovasertib toward NDA submission in H2 2026, backed by ~$973M cash runway into 2030. The compression looks more like duration sensitivity and pre-ASCO positioning than thesis deterioration — with sequential catalysts still ahead, this is the kind of dislocation the current tape eventually corrects.

4. Momentum Requires Reinforcement

The 2H25-into-2026 split between follow-through and reversal names is among the most instructive patterns in the current tape.

Three names sustained meaningful gains: RVMD (+116% → +84%), RLAY (+137% → +49%), DNTH (+128% → +117%). Three gave back nearly all of it: ZBIO (+300% → -47%), OLMA (+474% → -43%), VRDN (+114% → -56%).

The divergence was not primarily clinical. VRDN hit endpoints. ZBIO’s INDIGO data substantially de-risked obexelimab. OLMA’s OPERA-01 readout remains intact, pushed to Fall 2026. The difference was whether the original catalyst was an opening act or the main event.

The follow-through cohort kept adding chapters. DNTH extended Ph2 gMG data into positive interim Ph3 CIDP results, then executed a $719M upsized offering in May 2026 — bringing total cash to ~$1.2B and removing the funding overhang that has punished peers in similar windows. RVMD, already discussed for platform credibility, expanded from a single-asset oncology trade into a multi-program RAS franchise as combination strategies and registrational pathways matured. RLAY layered in vascular anomaly data that extended platform credibility beyond a single indication.

The reversal cohort, by contrast, experienced the original catalyst as the destination. OLMA transitioned into a longer execution cycle as OPERA-01 timelines extended and competitive SERD pressure built. VRDN hit endpoints but generalist capital rotated out as focus shifted toward commercial differentiation and launch complexity. ZBIO’s positive data was followed by financing uncertainty that capped re-rating durability.

Single-event repricing is no longer durable. The tape is pricing continuation, not arrival.

5. Cash No Longer Provides a Valuation Floor

Balance sheet strength offered little downside protection in the 2026 unwind.

VRDN is the starkest example. Viridian entered Q1 with $762M in cash against a current EV of ~$1.08B — implying the entire clinical pipeline, including its thyroid eye disease (TED) franchise competing against an established Horizon/Amgen standard of care, is valued at under $320M. In prior cycles, trading near cash-equivalent EV reliably attracted value buyers. In 2026, it hasn’t — the market is demanding de-risked data, not balance sheet optionality.

OLMA held $500M+ and still fell 46% YTD. The culprit wasn’t company-specific — class-wide SERD readthrough pressure hit the entire category, and no amount of runway insulated it from sentiment. QURE presents a different flavor of the same problem: $600M+ in cash, sitting ~70% below prior highs as investors discount the long runway to commercialization in gene therapy, where timeline risk and post-setback scepticism remain unresolved.

The shift: the buffer between cash value and implied pipeline value has narrowed materially. A strong balance sheet extends runway and limits downside — it no longer anchors a premium without near-term catalysts to justify it.

Liquidity is necessary. In 2026, it is not sufficient.

6. Obesity and MASH Remain a Privileged Capital Pool

Against a backdrop of generalized duration compression, obesity and MASH have remained relatively insulated. MDGL (-12% YTD) and VKTX (-15% YTD) declined modestly — both following substantial 2H25 appreciation, with MDGL having gained ~94% — while the broader bottom-40 XBI cohort fell ~19% median.

The 2H25 strength had a clear catalyst. Novo’s ~$5.2B acquisition of Akero and Roche’s ~$3.5B acquisition of 89bio — both FGF-21 programs targeting advanced fibrosis — embedded an M&A premium across MASH names through year-end and into the JPM Conference. That optionality has partially unwound in 2026, but not fully: the strategic logic that drove both deals hasn’t changed.

The resilience in 2026 reflects structure, not sentiment. Large commercial addressable markets with visible near-term monetization pathways are precisely what the current tape is willing to pay for. MDGL’s Rezdiffra generated $311M in Q1 2026 net revenue with 42,000+ active patients, commercially validating MASH as a scalable category even as peak positioning normalized. VKTX retains late-stage positioning across both indications with strategic optionality that generalist capital has not fully abandoned.

Neither name is immune to the broader compression — MDGL’s decline reflects real normalization and partial unwinding of those embedded M&A assumptions. But the category continues to attract longer-duration capital that has largely exited pre-commercial platform biotech. In a tape compressing almost everything, that relative insulation is itself a signal worth noting.

Bottom Line

The 2026 XBI tape is not a sector call. It is a duration, visibility, and reinforcement market — median dispersion between top and bottom cohorts exceeds 100% points YTD. The prior playbook — buy quality platforms, trust the balance sheet, let commercial franchises compound — has not worked.

Selective re-risking is warranted. Several prior momentum names with intact clinical theses are pricing outcomes well below what the data supports. The tape remains unforgiving, but for names where the next catalyst is visible and funded, the current entry may look better in hindsight than it feels today.